Summary

- The FOMC downshifted its pace of policy tightening, lifting the fed funds rate by 25 bps to a range of 4.50-4.75%, at the conclusion of its last meeting on February 1. Since then, the ground under the Fed has shifted enormously.

- The economic data have been decisively strong since the FOMC last met. Nonfarm payrolls rose by a combined 815K in January and February, and the inflation data remained uncomfortably high over the same period. Furthermore, upward revisions to the hiring and inflation data covering the end of last year suggest that the strength cannot be fully chocked up to an unusually warm first two months of the year. Rather, it appears monetary policy tightening to date has had a less potent effect on dampening demand growth and inflation than many observers would have thought previously.

- In isolation, the recent economic data are supportive of further tightening at the March 22 FOMC meeting. However, recent developments in the financial system have clouded the outlook to a considerable degree. Financial conditions tightened abruptly following the failures of Silicon Valley Bank (SVB) and Signature Bank on March 10 and 12, respectively. Financial markets have been highly volatile but clearly have reduced the amount of anticipated policy tightening by the Federal Reserve.

- Further hiking the fed funds rate would be a crystal-clear signal of the FOMC’s commitment to reducing inflation while also displaying confidence in the measures put in place to stem recent financial market stress.

- However, the dust is still settling from the nation’s second and third largest bank failures in history. We look for the FOMC to briefly pause its tightening efforts to ensure the situation is under control. In our view, the last thing the FOMC wants is more financial instability that threatens the banking system and forestalls any additional rate hikes down the road. But, neither a hike nor a pause would surprise us.

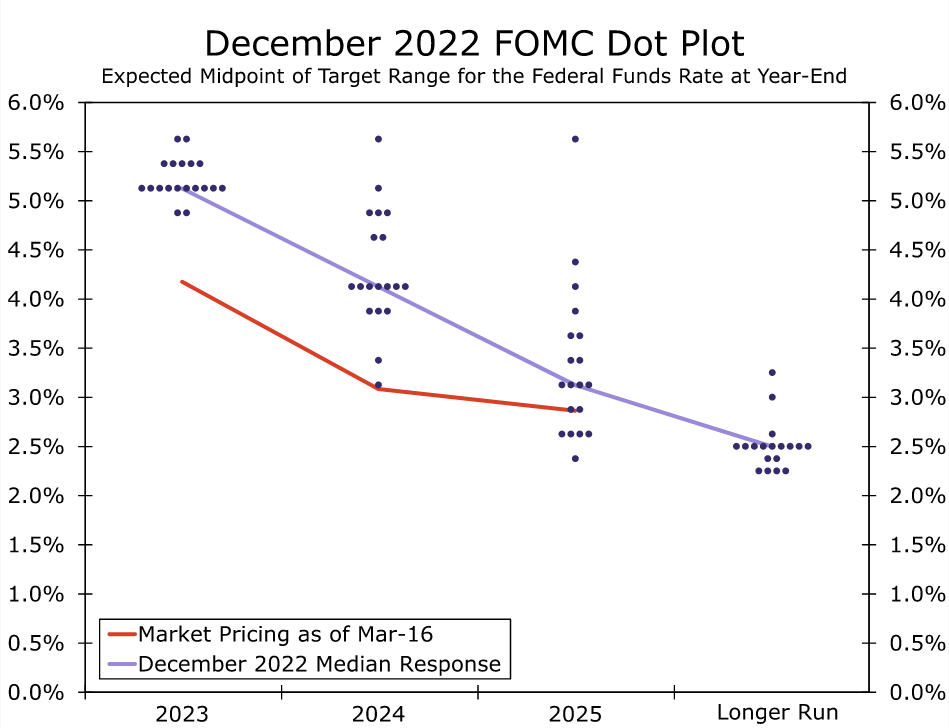

- If, as we anticipate, the FOMC opts to hold the fed funds rate at 4.50-4.75% at next week’s meeting, it could use the “dot plot” to clearly signal that the tightening cycle is unlikely to be over just yet. Between the economic data’s recent strength and the presumption that efforts to stem stress in the financial system will be effective, we expect the median dot for 2023 to move up 25 bps to a range of 5.25-5.50%.

- With some FOMC members likely to believe that rates will also need to be held above neutral for longer, we expect the median estimate for the fed funds rate at the end of 2024 to move up 25 bps from its December range of 4.00-4.25%.

What a Difference A Week Makes

The most recent FOMC inter-meeting period has been quite the roller coaster ride. Since the FOMC concluded its past meeting on February 1, data have suggested that the economy has significantly more positive momentum than previously believed. The resilience of the labor market and inflation in particular raised the prospect of the Committee re-accelerating the pace of rate hikes. With Chair Powell appearing open to such a move, the odds of a 50 bps move seemed a bit better-than-not in the days leading up to the blackout period. As recently as March 8, markets were priced for roughly a 70% change of a 50 bps rate hike.

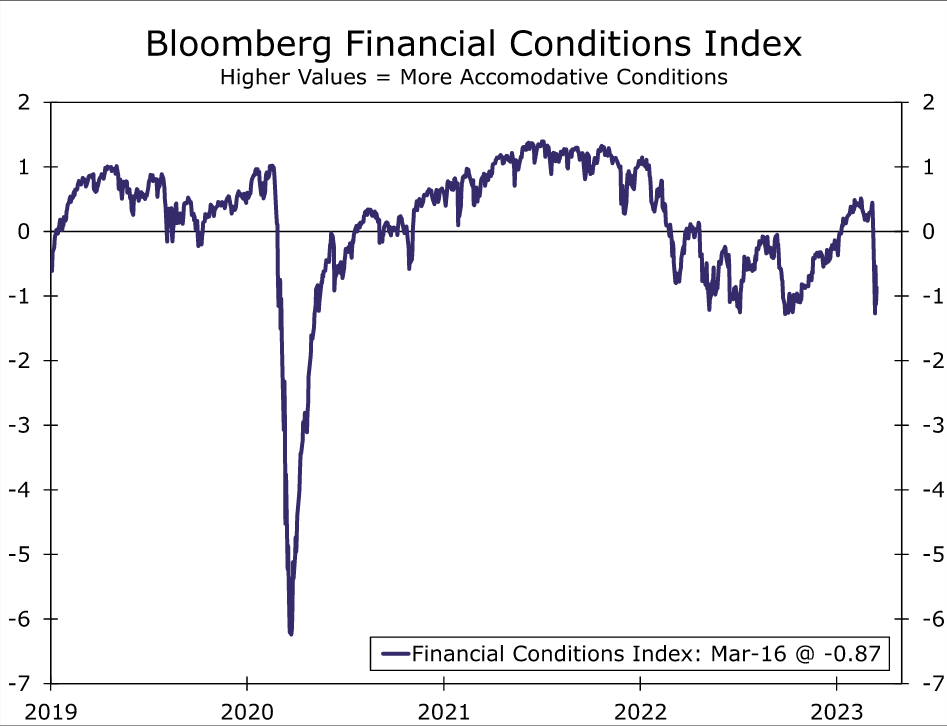

How quickly the world can change. Financial conditions tightened abruptly following the failures of Silicon Valley Bank (SVB) and Signature Bank on March 10 and 12, respectively (Figure 1). Policymakers responded swiftly to stem concerns that other financial institutions may find themselves in a similar position. On Sunday, March 12, the Federal Reserve announced a new lending facility—the Bank Term Funding Program—which allows eligible depository institutions to borrow against Treasury securities, mortgage-backed-securities and certain other securities at par. In addition, the Fed, FDIC and Treasury Department issued a joint statement on March 12 that included an assurance that even depositors with balances above the $250,000 FDIC insured threshold would be made whole.

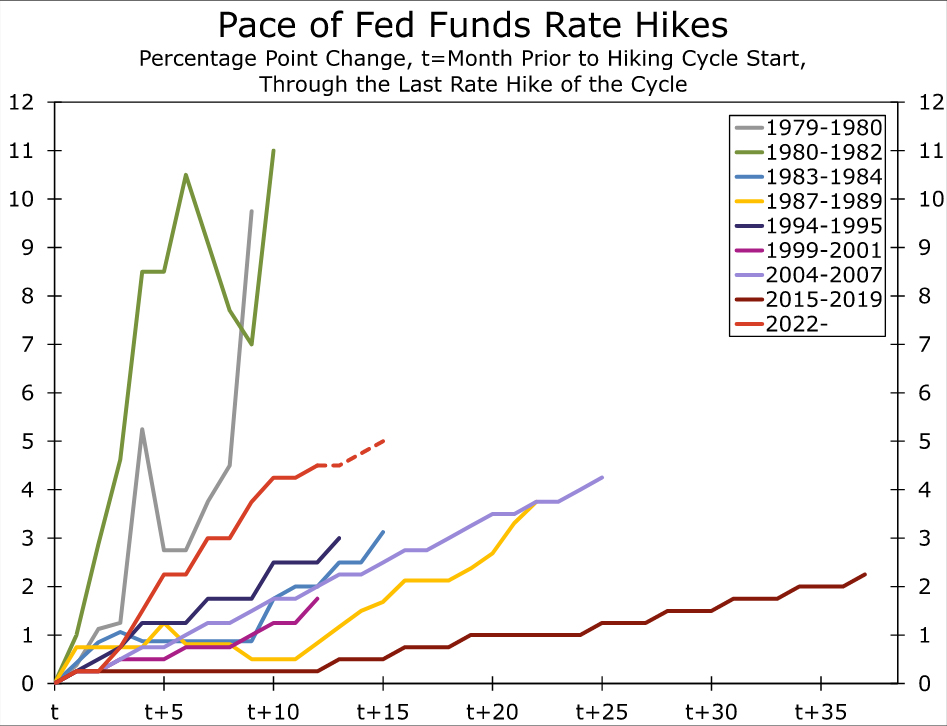

We covered these bank failures and the policy response in a recent special report. Both SVB and Signature Bank had some unique characteristics that made them particularly susceptible to a bank run. However, the failures brought to light the risks to financial stability that lurk behind the most aggressive monetary policy tightening in four decades (Figure 2). The FOMC was already performing a delicate dance by trying to rein in inflation without inflicting undue harm on the labor market. The recent financial market turmoil adds another dimension as policymakers must balance their efforts to quell inflation against the risk of igniting additional financial system stress.

Scales Tilted Toward a Pause, but It’s a Close Call

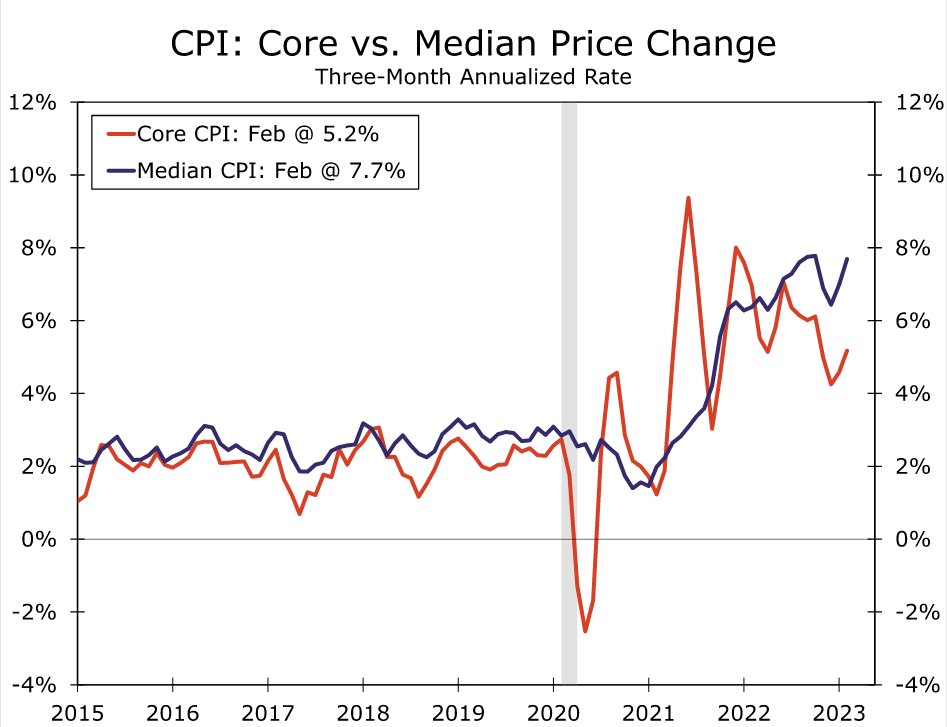

Whether or not the FOMC will proceed with policy tightening at its March meeting is not an easy call. Recent economic data clearly argue for at least another 25 bps rate hike. Not only does inflation remain well above target, but the underlying trend appears even higher than when the FOMC concluded its last meeting. Upward revision to last year’s inflation data and hot reports in January and February pushed the three-month annualized change in core CPI to 5.2%. Gains remain broad-based, with the median CPI advancing at a 7.7% annualized clip over the same period (Figure 3). What’s more, job growth has remained exceptionally strong. The economy added a combined 815K jobs in January and February on top of meaningful upward revisions to hiring in the fourth quarter of last year. Even with nascent signs of the jobs market cooling, such as the unemployment rate ticking up and average hourly earnings growth ticking down, the labor market remains incredibly tight. Opting to continue its tightening campaign would be a crystal-clear signal of the Fed’s commitment to bringing down inflation. It would also display confidence in the measures put in place to stem recent financial system stress.

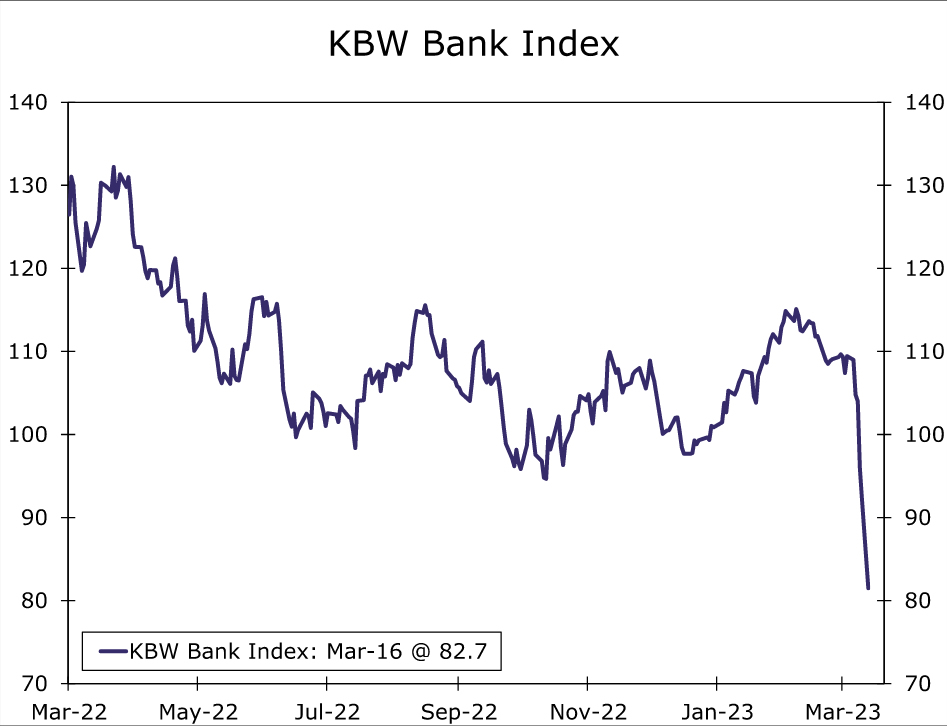

However, we believe the FOMC will pause its hiking campaign at next week’s meeting. The dust is still settling on the fallout from the second and third largest bank failures in the nation’s history. Headlines have swirled this week about additional financial system stresses, and share prices of many banks have tumbled (Figure 4). A brief pause gives policymakers time to ensure they have the situation under control and signal that they are attuned to the wide range of possible outcomes that could occur. Once financial markets have stabilized, additional monetary policy tightening can resume at subsequent meetings. Although there could be a small cost to the Fed’s inflation-fighting credibility with a pause, we believe the cost is outweighed by the possibility of fanning the flames at a time of heightened vulnerability. Put another way, the last thing the FOMC wants is more financial instability that threatens the banking system and forestalls any additional rate hikes down the road.

Ultimately, neither outcome would surprise us. A 25 bps rate hike at the March 22 meeting is clearly on the table, and other outcomes, such as a rate hike but a pause to quantitative tightening, strike as plausible, albeit less likely. Regardless, Chair Powell and his colleagues will have a very difficult tightrope to walk with their communication. We suspect the statement will include new language that references recent events but expresses confidence in the financial system and calls for additional monetary policy tightening to ensure the inflation fight is seen through to its conclusion. Chair Powell’s public remarks likely will reinforce this message. Looking ahead, we forecast that the FOMC will resume its tightening cycle in subsequent meetings with a 25 bps hike on May 3 and a final 25 bps increase on June 14. See our most recent U.S. Monthly Economic Outlook for more details regarding our forecast.

Summary of Economic Projections: The Tightening Cycle Is Unlikely to Be Over Yet

Even if the FOMC opts to pause, we doubt most members of the Committee will want to signal that the current tightening cycle has come to an end. The post-meeting statement and Chair Powell’s press conference will contain clues, but this meeting will also include an update to the Summary of Economic Projections (SEP). Chair Powell stated in his congressional testimony on March 7 & 8 that the recent stronger-than-expected data “suggests that the ultimate level of interest rates is likely to be higher than anticipated”. But, that was before the recent bank failures and subsequent financial system stress.

In the most recent SEP, published at the December 2022 meeting, participants’ median expectation for the fed funds target range at the end of 2023 was 5.00-5.25%, roughly a quarter-point higher than the market at the time of its publication. But, the distribution skewed higher (Figure 5). Given the recent financial system turmoil, we doubt the dots will move higher in a major way. But, with inflation’s momentum proving more difficult to break and the economy continuing to expand at a solid rate, we expect the median dot for 2023 to shift up to a target range of 5.25-5.50%, 25 bps higher than the December projections. An increase of a similar magnitude for the median dots in 2024 and 2025 also strikes us as reasonable. In our view, this would be a way for the FOMC to illustrate its intentions that, despite a brief pause, monetary policy tightening will resume in the near future.

We suspect the dispersion of the dots will become even wider. In the December projections, most of the 2023 dots were clustered between 5.0% and 6.0%. Yet in 2024 and 2025, there was a much broader ranger of views among Committee members, with the lowest 2024 dot (3.125%) well below the highest 2024 dot (5.625%). Given the elevated uncertainty in the economic outlook, we would not be surprised if the distribution of dots becomes even less concentrated for 2023 and beyond.

The recent strength of the economy and inflation are likely to be evident in the Committee’s economic projections. We estimate that real consumer spending grew at a solid 2.8% annualized rate in Q1, and, as a result, we expect the Committee’s median projection for 2023 real GDP growth, which was 0.5% in the December projections, to be revised up by at least a few tenths-of-a-percentage point. However, with the effects of policy tightening seeming to take longer to feed through to the economy, we would not be surprised to see the median GDP growth estimate for 2024, most recently at 1.6%, revised somewhat lower.

Similarly, the year-end 2023 estimate for the unemployment rate is likely to be revised down slightly. The unemployment rate ended 2022 two-tenths of a percentage point lower than the FOMC’s projection in December, and it stood at just 3.6% in February. If the median estimate for the unemployment rate in Q4 remained unchanged at 4.6%, it would imply FOMC participants expect the labor market to deteriorate more rapidly this year, which seems unlikely.

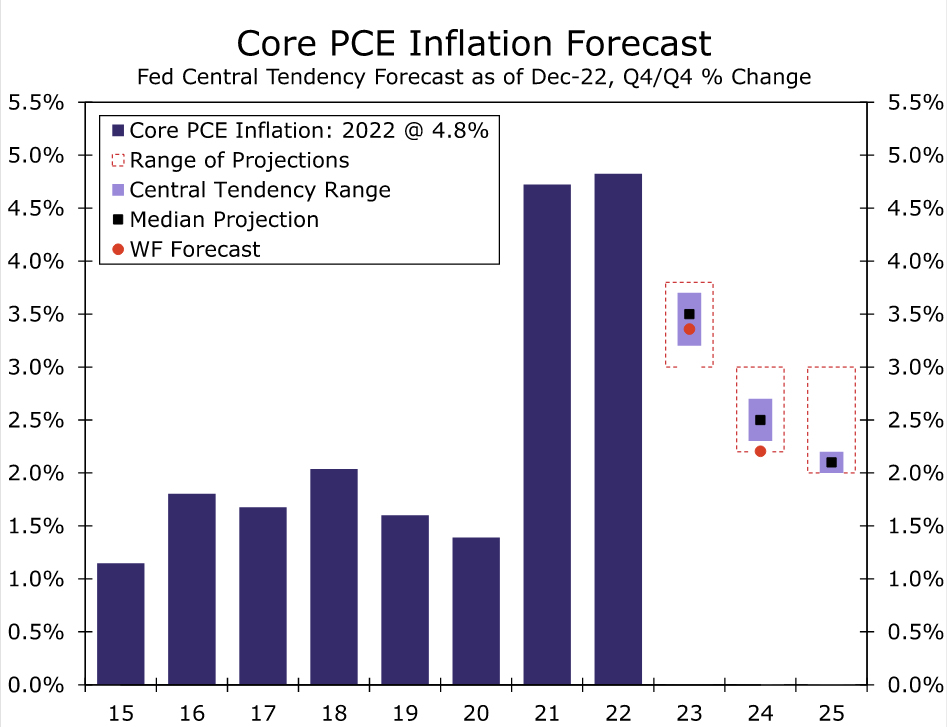

While the recent run of strong inflation data has led market participants and many economists, including ourselves, to mark up inflation forecasts, Fed officials appear to have been less caught off guard. The median estimate for Q4/Q4 core PCE inflation was 3.5% in the December SEP, roughly half a percentage point above the December Bloomberg consensus and median submission to the New York Fed’s December primary dealer survey. Our most recent forecast is for core PCE inflation of 3.4% in Q4-2023 (Figure 6). We think the Committee’s median inflation projections for 2023 and beyond could tick higher by a tenth or two, but we would be surprised by a move any larger than that.

{kind=link}