- Macro and banks’ balance sheet data covering the period after SVB’s collapse shows that immediate negative consequences to real economy have been modest.

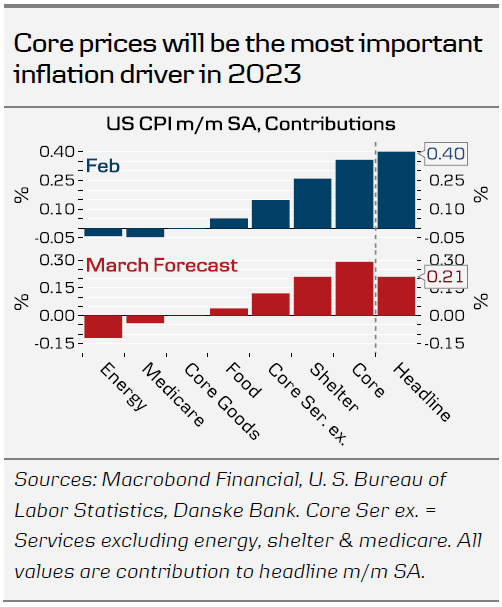

- The March Jobs Report and CPI will be the final key releases before Fed’s May meeting. We see Core CPI at +0.4% m/m, and look for 250k NFP growth.

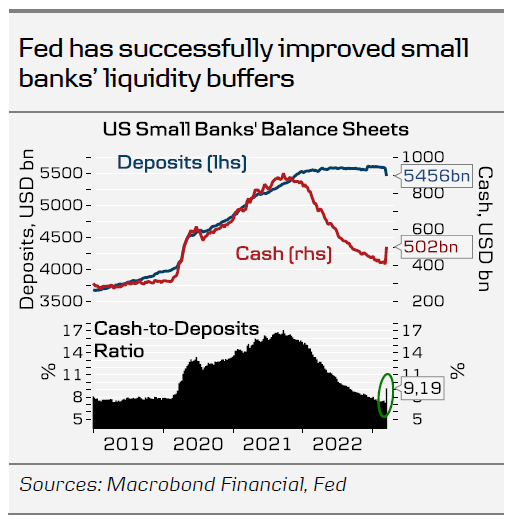

The series of stronger-than-expected macro data releases seen in February appears to have continued into March. This is consistent with the most acute banking sector risks now seemingly easing, as Fed’s emergency lending facilities have improved even the smaller US banks’ liquidity buffers above pre-pandemic levels. The combined use of the facilities edged lower this week and interbank lending markets remain calm for now.

Bank deposits as a whole are declining due to Fed’s QT reducing the supply of money in the system, and not due to money being pulled out of the banks. Money can only exit the banking system via cash withdrawals (which remain stable) or reverse repos to the Fed. Money market funds have seen sizable inflows over the recent weeks, likely reflecting some deposit outflows from smaller banks, risk aversion from equities and relatively high short-term interest rates, but as the use of Fed’s reverse repo facility has been little affected, the amount of total bank deposits has not been affected.

The risk of a ‘credit crunch’ weighing on regional bank lending has drastically weighed on markets’ expectations of future growth, inflation and consequently also the level of nominal yields. The focus has been on commercial real estate, a sector hit by both lower demand for office space and rising yields. Small banks account for more than 70% of total bank lending to CRE sector, and practically all of the lending growth seen over the past 5 years.

That said, Fed’s Senior Loan Officer Survey suggests that small banks’ credit standards for non-residential CRE lending have tightened already since Q3 2022, largely in line with developments seen in broader financial conditions. Around USD50bn of regional banks’ CRE loans will mature in 2023, which is only 4% of the total CRE loans issued by small US banks. While the rapid monetary policy tightening combined with regional banks’ past years’ looser regulation could pose longer-term challenges, we think markets might overestimate the near-term negative growth impact from the banks’ lower lending appetite. Furthermore, market-based financial conditions indices, such as our in-house ‘growth tax’ measure or the GS index, have actually eased, as the decline in yields, mortgage rates and oil prices has more than compensated for the wider credit spreads.

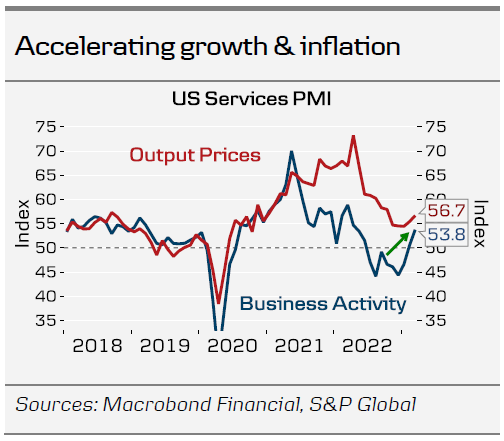

The March Flash PMI data, largely collected after SVB’s collapse, pointed towards a clear pick-up in economic growth. Furthermore, inflation pressures in the services sector, closely followed by the Fed, appeared to accelerate. While lower energy prices will ease March headline inflation to around +0.2% m/m, we expect core inflation to remain elevated at +0.4%. We also think employment growth remained upbeat in March, and look for +250k NFP gain in the next week’s Jobs report. Altogether, we see central banks sticking to the tightening bias for now. As focus turns back towards macro data, we think markets are likely to reverse some of the Fed’s rate cut pricing for 2023.

{kind=link}