There is a heavy load of US economic releases coming up this week. The highlight will be the latest GDP report on Thursday, which will help shape market expectations about the trajectory of interest rates as the Fed prepares to roll out the final rate increase of this cycle next week. As for the dollar, it has been on the ropes lately, but better days may lie ahead.

US economy regains steam

The economic data pulse in the United States has improved significantly lately. Business surveys point to an economy that is regaining growth momentum, the banking crisis has receded, and the unemployment rate remains near historic lows. It seems that fears of a recession were overblown, or at least premature.

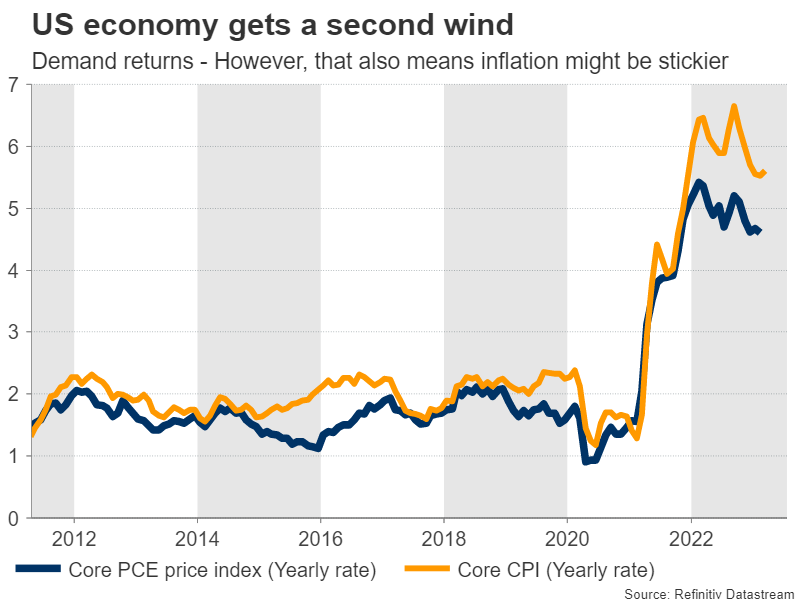

But not everything is rosy. The dark side of this surge in demand is that inflationary pressures have received a second wind too. Companies continue to raise their selling prices at a rapid clip, and this has been reflected in the core inflation rate, which remains sticky at elevated levels. In other words, the inflation battle is not over.

And yet, investors think the Fed is about to conclude its tightening cycle. Market pricing suggests the US central bank will deliver one final 25bps rate increase next week and then move to the sidelines while the economy absorbs the lagged impact of previous rate hikes. Traders are also betting the Fed will start to cut rates before the year ends.

With the Fed currently in its blackout period ahead of next week’s policy decision, there won’t be any public comments from FOMC officials this week, so the spotlight will be entirely on data releases.

Upside GDP surprise?

The show will get going on Tuesday with the Conference Board consumer confidence index, ahead of the latest batch of durable goods orders on Wednesday. Both are considered forward-looking measures of economic activity, so they will be closely watched.

Turning to the main event, the preliminary estimate of GDP growth for the first quarter will be released on Thursday. The US economy is expected to have grown at an annualized pace of 2%, driven mostly by an upturn in consumption. There is some scope for a stronger-than-expected print, considering that the Fed’s GDPNow model estimates growth at 2.5% instead.

Wrapping things up on Friday will be the core PCE price index for March, alongside personal consumption and income figures. Forecasts point to a minor decline in the yearly PCE rate, although the risks seem tilted to the upside in this case too, judging by the spike higher in the core CPI rate during the month.

A round of strong data could dispel some speculation for Fed rate cuts this year, and help the dollar recover some poise. Looking at the euro/dollar chart, the 1.0910 zone could serve as the first durable obstacle to any declines.

One interconnected trade

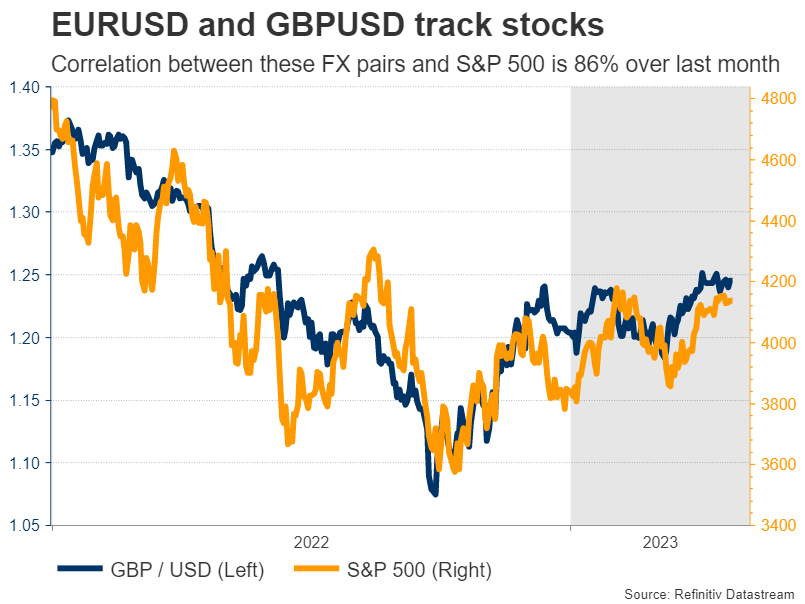

In the big picture, the dollar has been underperforming for several months now. Some of this weakness is linked to the brighter outlook in Europe that has fueled expectations for continued ECB rate increases and boosted the euro, but perhaps an even bigger driver was the cheerful tone in stock markets.

The 30-day rolling correlation between euro/dollar and the S&P 500 currently stands at 86%, and it is even higher for sterling/dollar. This suggests that recent FX moves have been mainly a reflection of the mood in stock markets.

Hence, any turnaround in stocks could be particularly painful for pairs like euro/dollar and sterling/dollar. With equity valuations having reached extreme levels again just as corporate earnings growth has turned negative, the risks surrounding stock markets seem tilted to the downside.

In turn, this allows some scope for a comeback in the dollar, especially if euro/dollar is unable to pierce above the 1.1070 region.

{kind=link}