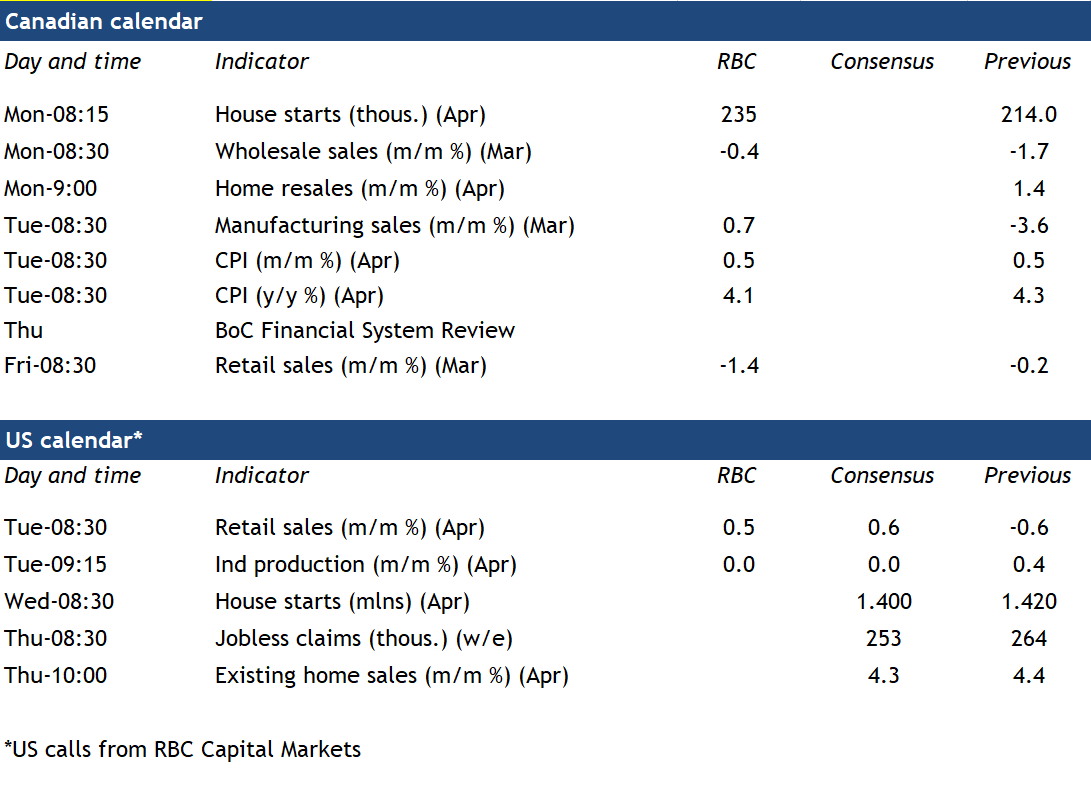

Canada’s April inflation reading likely ticked lower again. We expect to a 4.1% year-over-year rate from 4.3% in March. A 6% increase in gasoline prices from March suggests energy prices fell a little less. But grocery price growth has been slowing and we expect broader gradual softening in underlying inflation pressures to have continued.

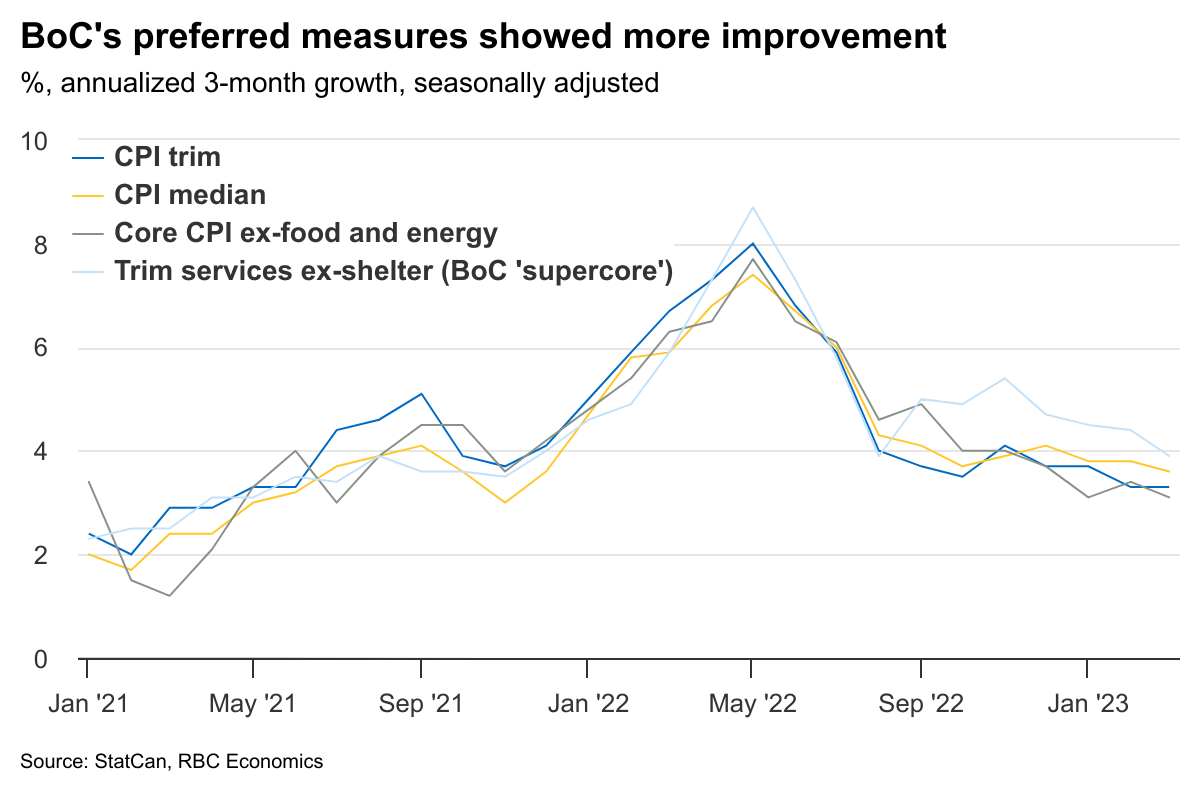

With headline CPI moving in the right direction, all eyes will be on the Bank of Canada’s preferred measures of core inflation for signs that higher interest rates are slowing price growth. Year-over-year growth for the CPI trim, median, and the new ‘super core’ services ex-shelter measure introduced in the BoC’s last Monetary Policy Report should all slow substantially as large monthly increases in April a year ago fall out of the annual growth rates. More recent month-over-month core price increases have been running around a 3 ½% (annualized) rate. That’s still above the BoC’s 1% to 3% target range, but down sharply from peak levels last summer. The breadth of inflation pressures has narrowed. And early signs that the lagged impact of higher interest rates are weighing on economic growth suggest underlying inflation pressures should continue to ease. Early estimates are pointing to declines in Canadian wholesale and retail sales in March, with a 0.7% increase in manufacturing sales probably tied to a big surge in notoriously volatile aerospace sales.

The Bank of Canada is presently expected to sit on the sidelines for the remainder of 2023. Additional evidence of weaker price growth coupled with softening demand will affirm their present policy stance.

Week ahead data watch

The BoC’s Financial System Review (FSR) will be more closely watched than usual given the tightening credit standards in regional banks, and wobbly commercial real estate (CRE) markets. The BoC’s Q1 Senior Loan Officer survey flagged some tightening in lending conditions, but not to the same extent as has been observed in the U.S.

Statistics Canada’s advance estimate indicated that March manufacturing sales rose 0.7% following a 3.7% pullback in February. Prices likely declined (led by a drop in petroleum & coal prices), implying a larger rise in volume terms. But most of the increase appears to have come from a surge in the often-volatile aerospace component.

Early estimates from Statistics Canada pointed to declines in March retail sales (-1.4%) and wholesale trade (-0.4%.) The former likely included a pullback in auto sales, with industry reports pointing to another decline in motor vehicle sales in April.

Canadian home resales probably ticked higher for a third straight month in April, according to early market reports. Prices likely also edged higher for a second straight month following a year of consecutive declines.

We expect the U.S. retail sales to tick up 0.5% in April, driven by an increase in unit auto sales. U.S. industrial production likely held steady in April, with a sharp decline in heating days resulting a lower output in the utility sector. Manufacturing output probably edged higher, but not by enough to fully reverse the 0.5% decline in the prior month.

{kind=link}