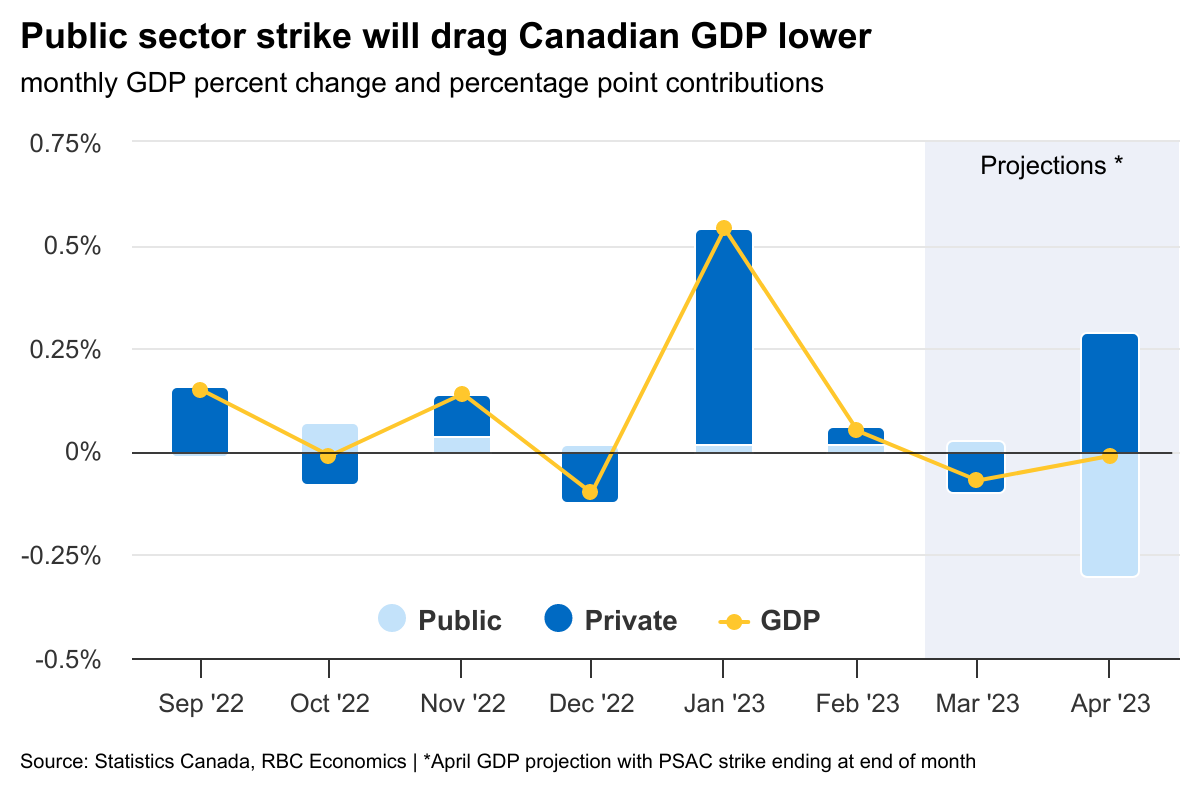

We expect next week’s Q1 GDP report to show a strong start to 2023—with real output up 2.5% on an annualized basis. Aside from a significant add from exports (thanks to a rebound in motor vehicle and parts), domestic demand was probably on the softer side. And rate-sensitive sectors continue to be squeezed by tighter monetary policy. This has had the most notable impact on residential investment, which we expect to post another significant decline. Business investment is also expected to have slowed and our own RBC cardholder data signaled softening discretionary goods-sector spending throughout the quarter. Resilience gave way in March. Monthly GDP data is likely to be broadly in line with Statistics Canada’s initial flash estimate for a 0.1% decline in March. Weakness in wholesale and retail trade and residential investment was enough to offset strength in manufacturing sales.

We anticipate another small monthly decline in April. The strike by workers with the Public Service Alliance of Canada (PSAC) is expected to shave 0.3 percentage points from April GDP. But aside from public sector weakness, activity was likely largely flat. The impact of the Bank of Canada’s aggressive rate hikes will continue to be felt with a lag as household debt servicing ratios become more burdensome. Demand is expected to weaken into Q2 as Canada enters a mild recession.

Next week’s monthly GDP release will be the final reading before the Bank of Canada’s June rate decision. An increase in headline CPI in April and four months of exceptionally strong labour market data have increased the risk of an additional hike. However, softening monthly GDP may help solidify the Bank of Canada’s present stance of staying on the sidelines (for now).

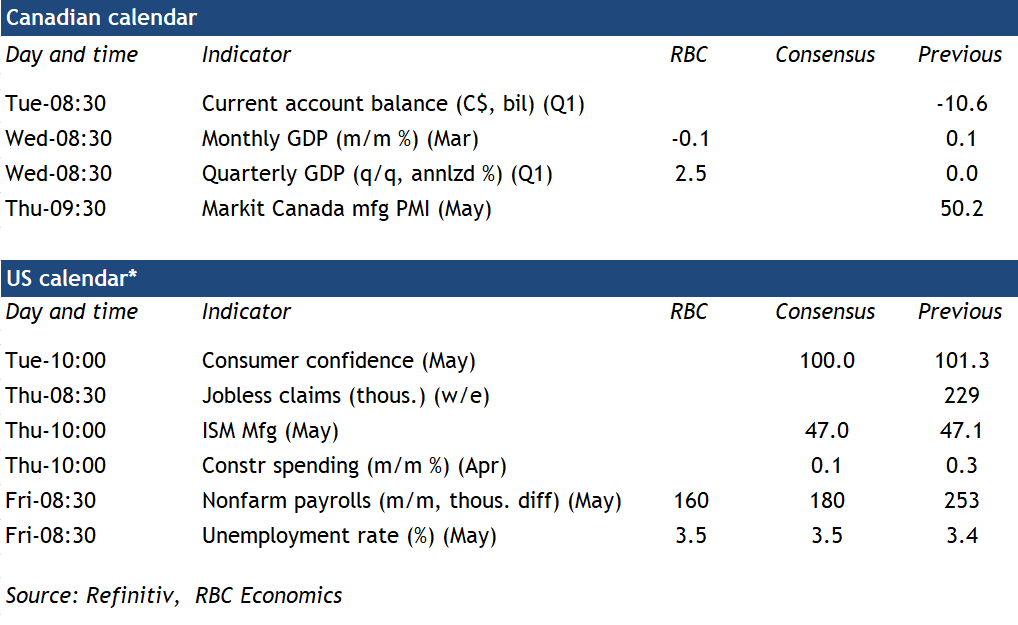

Week ahead data watch

U.S. employment numbers will likely come in weaker in May. The unemployment rate is expected to tick slightly higher but remain at historic lows. While U.S. labour markets remain exceptionally strong, early signs of a slowdown are emerging. U.S. job openings and quits are trending lower as wage growth slows.

, domestic demand was probably on the softer side. And rate-sensitive sectors continue to be squeezed by tighter monetary policy. This has had the most notable impact on residential investment, which we expect to post another significant decline. Business investment is also expected to have slowed and our own RBC cardholder data signaled softening discretionary goods-sector spending throughout the quarter. Resilience gave way in March. Monthly GDP data is likely to be broadly in line with Statistics Canada’s initial flash estimate for a 0.1% decline in March. Weakness in wholesale and retail trade and residential investment was enough to offset strength in manufacturing sales.){kind=link}