U.S. Highlights

- The ISM Services index surprised on the downside, falling 1.6 points to 50.3 in May. The employment sub-index drifted below the 50-point contractionary threshold for the first time since December.

- Initial jobless claims rose by 28,000 in the week ending on June 3rd, lifting initial claims to 261,000 – the highest level in 20 months. However, this week included the Memorial Day holiday, which may have distorted the data.

- The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The widening of the trade deficit in April indicates that trade is likely to subtract from growth in the second quarter.

Canadian Highlights

- The Bank of Canada (BoC) raised the overnight rate by 25 basis points to 4.75%, the highest level since early-2001. The BoC has left the door open to further interest rate hikes.

- The Canadian job market was set back -17.3k jobs in May, the first contraction in nine months. It is too early to tell if this crack will continue to grow in coming months.

- Next week’s national housing market data will be watched to see if home sales continued their rapid ascent in May.

U.S. – Mild Signs of a Slowdown Continue

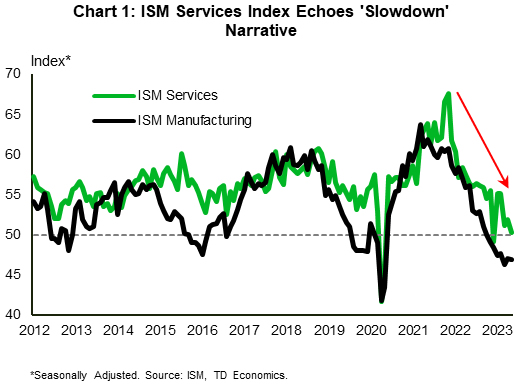

In the wake of last week’s debt ceiling deal, markets had the opportunity to catch their breath in a quiet week for data releases. The ISM Services report disappointed, with the headline index falling 1.6 points to 50.3 in May, instead of improving moderately to 52.4 as per market expectations. The recent downtrend reflects an economy that is gradually decelerating, echoing the ‘slowdown’ narrative advanced by its manufacturing counterpart (Chart 1). This theme was further supported by the report’s details, with all the main sub-indicators – including business activity, new orders, and employment – declining on the month. Of note, the employment index fell 1.6 points to 49.2, drifting below the 50-point contractionary threshold for the first time since December.

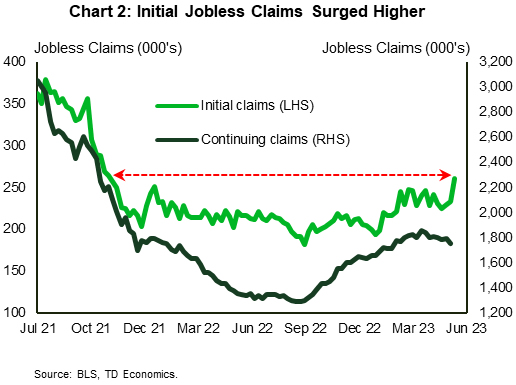

Continuing with signs for some potential softening in the labor market, initial jobless claims surged higher in the week ending on June 3rd, rising by 28,000 – much more than anticipated. This lifted initial claims to 261,000 – the highest level in 20 months (Chart 2). While the increase is substantial, for now we caution against reading too much into this. The weekly data can be noisy, and the week included the Memorial Day holiday, which may have also injected some volatility. Secondly, looking at seasonally unadjusted figures, the increase lacked breadth across states, as it was concentrated in Ohio, California, and Minnesota.

April’s international trade report did little to lift the mood. The U.S. trade deficit jumped by $14 billion or 23% in April to $74.6 billion – the widest level in six months. The most noticeable change was in the goods category. The U.S. goods deficit grew by close to 18%, as exports fell 5.3% and imports grew 2%, with the latter marking a rebound after two consecutive monthly declines. Trade made no contribution to economic growth in the first quarter of this year. The widening of the trade deficit in April indicates that it is likely to subtract from growth in the second quarter.

All told, the few reports that came out this week point to growth in the U.S. economy moderating. The Fed will take this information into account before it meets next week to set monetary policy. The last major piece of information on the docket before the Fed makes its decision is May’s CPI inflation report, which comes out one day ahead of the FOMC meeting. The market consensus forecast calls for core CPI to ease moderately to 5.3% year-on-year in May from 5.5% in April. Surprise rate hikes from the Reserve Bank of Australia and the Bank of Canada earlier this week serve as a reminder that amidst stubborn inflation there’s the potential for the Fed to opt for a hike too. That said, Fed officials have been vocal in signaling that they will forego a hike at next week’s meeting. Market odds are in tune with this view, attaching a 75% probability to a stand pat decision next week (as tracked by CME Group). However, markets still narrowly favor a hike at the next meeting in July (52% odds). In short, while next week is likely to be uneventful regarding policy changes, Fed communication may offer additional insight as to whether the FOMC sees the need for some further tightening over the near-term or not.

Canada – Getting Back Into the Game

The Bank of Canada (BoC) has made headlines once again. The Bank raised the overnight rate by 25 basis points (bps) to 4.75% as the conditions it had set to maintain a pause on interest rate hikes had been violated. The BoC will not step back to the sidelines, instead keeping the door open to further interest rate hikes should data reveal ongoing resiliency. Post-announcement, the Canadian two-year yield jumped by 20-bps to 4.58 (down to 4.50 by the end of the week) while the Canadian dollar rallied half a cent to 0.75 cents U.S. and has largely held at this level.

There has been plenty of justification for a rate hike on the data front so far in 2023. Notably inflation, especially core measures, proved stickier than expected in April. Labour markets wouldn’t let up as monthly employment gains persistently surprised to the upside, contributing to resilient consumer spending. GDP for the first quarter clocked in at 3.1% quarter-on-quarter (q/q) annualized, above the 2.3% projected in the BoC’s April Monetary Policy Rreport. The BoC also called out the recent pick up in spending on interest-sensitive goods and the housing market as evidence that “Excess demand… looks to be more persistent than anticipated”.

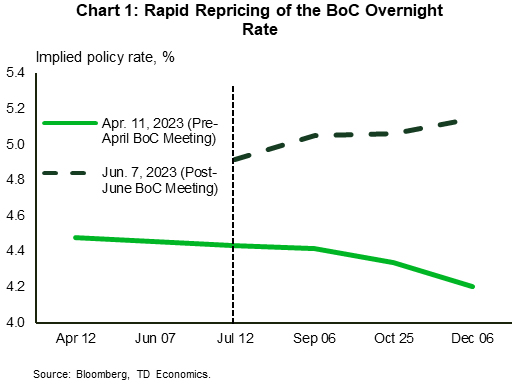

The question is where do they go from here? Chart 1 shows that prior to the April meeting, markets were anticipating the BoC to cut by 25–50 bps by the end of the year. Now, markets expect another 25-bps hike to come, with upside risk for 5.25%. We expect the BoC hike to 5.00% in July and hold at that level into 2024.

The policy rate announcement was delivered before Friday’s labour market release for May, which saw Canada shed 17.3k jobs, ending the longest run of job gains since 2017. Full-time jobs contracted for a second straight month (-32.7k), while the unemployment rate ticked up two-tenths of a percent to 5.2%. Hours worked were down 0.4% month-on-month (m/m), potentially as a result of the Alberta wildfires, while wages clocked in at 5.1% year-on-year (y/y). At an industry level, Chart 2 shows that the breadth of employment change–measured on a three-month moving average basis–is coming back into balance. Productivity, measured as real output divided by hours worked, declined for a fourth straight quarter by 0.6%. Canada has been able to sustain a higher level of output through job creation even as productivity notoriously lags, but this trend is unsustainable as employment eventually moderates. All in all, it’s too early to tell if May’s jobs report signals the start of that trend, or if it is just a small chip on an otherwise super-tight labour market.

Next week features updates to May’s housing data, where we expect home sales to continue their strong bounce back. We’ll also get a pulse check on Canadian industrial activity via manufacturing and wholesale sales for the month of April.

has made headlines once again. The Bank raised the overnight rate by 25 basis points (bps) to 4.75% as the conditions it had set to maintain a pause on interest rate hikes had been violated. The BoC will not step back to the sidelines, instead keeping the door open to further interest rate hikes should data reveal ongoing resiliency. Post-announcement, the Canadian two-year yield jumped by 20-bps to 4.58 (down to 4.50 by the end of the week) while the Canadian dollar rallied half a cent to 0.75 cents U.S. and has largely held at this level.){kind=link}