U.S. Highlights

- A week’s worth of solid data did little to contradict Fed Chair Powell’s comments suggesting more monetary tightening is on the way.

- However, May’s personal consumption expenditure (PCE) report did provide a bit of reassurance for the Fed that demand is slowing down as real expenditure growth has been flat in three of the past four months.

- The problem remains that inflation is showing little sign of relenting and Fed officials are going to stay focused on tightening policy to cool the price pressure.

Canadian Highlights

- With less than two weeks to go until the next Bank of Canada (BoC) rate decision, economic data this week prompted financial markets to cement expectations for another rate hike this summer.

- Headline inflation did cool to the lowest pace in two years in May. But, progress on the BoC’s core measures is much slower. This raises concerns that inflation will remain stuck above the Bank’s 2% target.

- On the growth side, industry-level GDP signaled that the population driven boost to GDP growth during the winter continued into the spring. Growth appears to be running ahead of the BoC’s expectations yet again.

U.S. – Healthy Data Keep Pressure on Fed

Fed Chair Jerome Powell noted this week that Fed officials, “believe there’s more restriction coming” from monetary policy in light of the persistently strong economic data. This week’s data stream did little to dissuade the sentiment. We got healthy prints from the housing market, consumer confidence, and manufacturing orders along with a personal consumption expenditure (PCE) report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.

First up, activity in the housing market has ticked up. New home sales rose to their highest level since February 2022 in May. The market for new single-family homes troughed in July 2022 and has been trending upwards since, as inventories in the existing home market remain tight (see commentary). Sales in the existing market did move up in May as well, as a solid labor market helps drive demand.

Consumers’ moods have also been improving lately as the Conference Board consumer confidence index for June jumped up to its highest reading since January 2022. With both consumers’ assessment of the present situation and future expectations moved up on the month. Overall, consumers are not as confident as they were prior to the pandemic, likely as they contend with high inflation, but their higher spirits defy the recession warnings.

The good news didn’t just stop there. The industrial side of the economy saw manufacturers’ new orders of durable goods blow out expectations for a contraction, with a healthy advance. Taking a closer look at a key indicator of business investment, new orders excluding defense and aircraft advanced a solid 0.7% in the month, and 0.3% month-on-month when stripping out the effects of inflation.

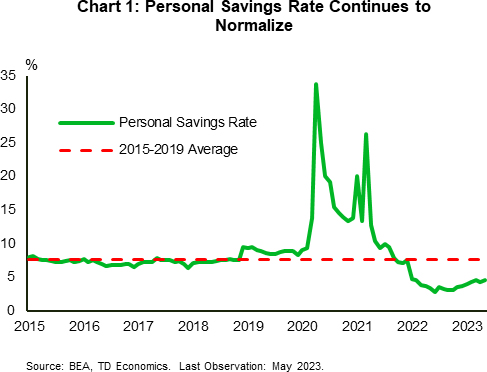

However, May’s consumer spending report suggests that demand has paused from its strong start to the year. Real expenditures were flat for the third time in fourth months, as an advance in services spending was offset by a drop in goods spending. Moreover, it looks like consumers are adjusting habits as they save a bit more of their disposable income. The personal savings rate ticked up to 4.6% in May, nearly two percentage points higher than its low registered in June 2022 (Chart 1). With the Supreme Court striking down the Biden administration’s student debt relief plan today, and a separate student loan payment moratorium set to end, headwinds to the consumer spending outlook continue to build heading into the second half of 2023.

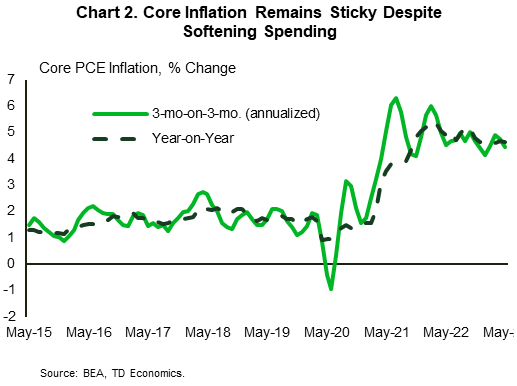

However, inflation continues to be problematic. Core PCE inflation (Chart 2) is showing little sign of relenting, up 4.6% y/y, with the near-term trend cruising along at 4.4% (annualized). Inflation has been stuck well above the two percent target, which is likely to keep officials focused on tightening policy to cool it down. Markets are looking for the Fed to hike rates again this year by another 25 basis points – taking the policy rate to a 22-year high of 5.5%. The FOMC’s next decision is at the end of July, giving it some time to see a few more readings on economic momentum before making its decision. Next week’s June jobs data is likely to be a key piece of it’s calculus.

Canada – Inflation Eases While Population Pops

The countdown is on to the next Bank of Canada rate decision on July 12th, and there was plenty economic data this week for them to factor into their thinking. All told, the data suggest that monetary policy has yet to exert enough of a braking force on the economy and inflation. Financial markets have further cemented expectations for a BoC interest rate hike this summer, leading the Canada 2-year yield to establish a new cycle high.

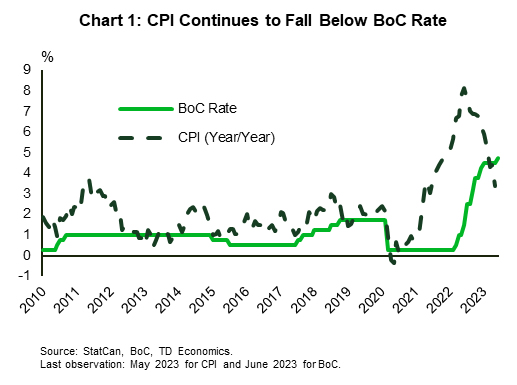

Headline inflation cooled notably in May, but core price pressures are coming down at a glacial pace. The Consumer Price Index was up 3.4% year-on-year (y/y) in May, down from 4.4% y/y in April, more than a percent below the BoC’s policy rate (Chart 1). Gasoline was the main contributor, with prices at the pump now far below year ago levels . Unfortunately, food inflation remained a problem, with prices up 8.3% y/y, having barely budged from their peak in January 2023.

The Bank of Canada’s core inflation metrics (trimmed mean and median) decelerated, but to a lesser degree than the headline figure, averaging 3.9% y/y in May, versus 4.3% y/y in April. More concerning was our measure of ‘supercore’ inflation that reflects cyclically driven services inflation, which at 5.5% y/y is little changed from April’s reading of 5.7% y/y. Travel was the main driver here as Canadians prepare for summer vacations.

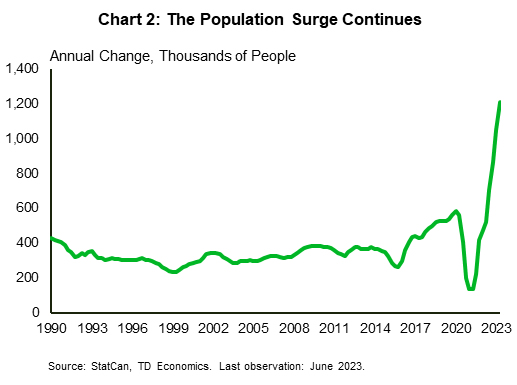

The surge in Canada’s population over the past year has been a big swing factor in the economy. Canada welcomed 292k more people in the first three months of the year, bringing the 12-month total to above 1.2 million (Chart 2). With more people living and working in the country, consumer spending surged by nearly 6% quarter-on-quarter annualized (q/q) in the first quarter. Firms have struggled to keep up with rising demand, so they have been hiring more workers, boosting wages, and raising prices.

We received some insight this week into how much of this momentum has carried over into the second with the release of industry GDP. While the print for April was unchanged, the flash estimate for May showed a big increase. This sets up second quarter GDP to come in above the BoC’s forecast. At the same time, the BoC released its Business Outlook Survey and its companion Canadian Survey of Consumer Expectations. While both have signaled caution going forward, there is growing belief that the worst is over “as uncertainty about the path of future interest rates and concerns of a recession fade”.

The Bank of Canada has less than two weeks before its next interest rate decision. Although there has been a notable improvement in overall Canadian inflation, underlying core measures reveal a big challenge going forward. The economy has continued to grow at a very healthy clip, supported by a surging population. This has kept up pressure on wages and domestic prices. The BoC will have a few more data points next week, including the key June employment data, to help it decide what to do next. But thus far, the data have been leaning towards another hike in July.

report that showed little sign of core inflation abating. All told, the data underscored that the economy continues to chug along at a firm pace.){kind=link}