Summary

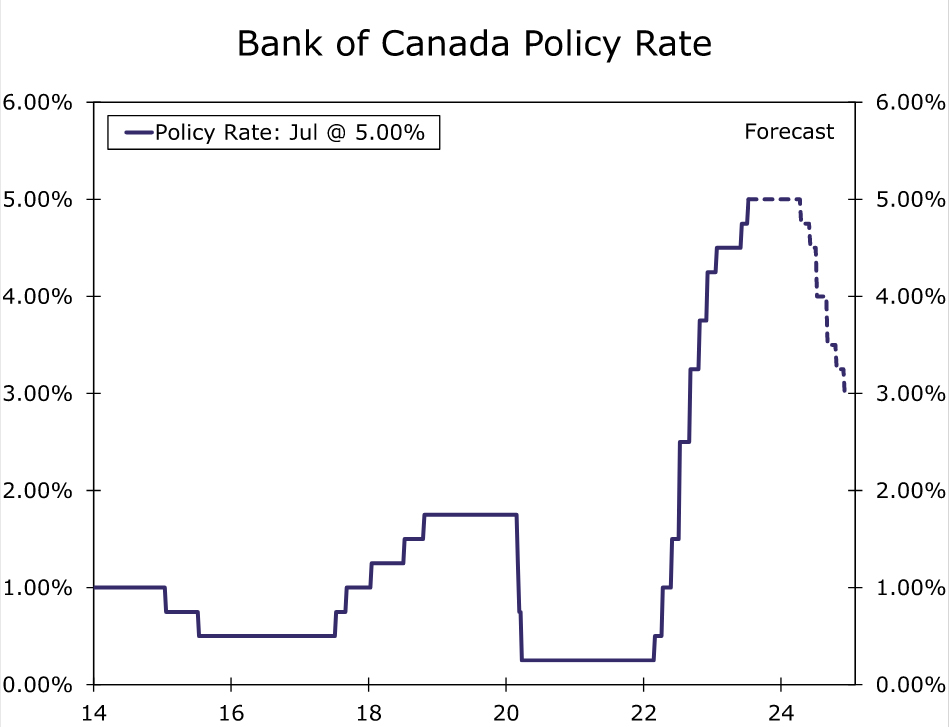

The Bank of Canada (BoC) raised its policy rate 25 bps to 5.00% at last week’s announcement, and while BoC Governor Macklem suggested the end of the tightening cycle was close, there were nonetheless several hawlish elements in the announcement. In particular, the Bank of Canada expects excess demand within the Canadian economy to persist for longer than previously anticipated, while also raising its CPI inflation forecasts.

In our view, the onus is on the data to soften to dissuade the central bank from tightening further. So far there is limited evidence of a downshift, with employment, retail sales and GDP expanding at a steady pace, and underlying inflation trends persistent. While at this stage we lean towards the BoC remaining on hold at its September meeting, and for its policy rate of 5.00% to represent to peak for the current cycle, that view is heavily data dependent. If upcoming data, including July employment, the July CPI and Q2 GDP fail to show a perceptible softening, then the risk scenario of a 25 bps rate hike in September to 5.25% could crystalize. Either way, we do not expect rate cuts to begin until well into next year, and forecast a cumulative 200 bps of rate cuts between Q2-2024 and Q4-2024.

Bank of Canada Hikes Rates, Leaves The Door Open For Further Tightening

After resuming its rate hike cycle in June, the Bank of Canada (BoC) followed up with another 25 bps rate hike at its July announcement. While BoC Governor Macklem said “we think we’re close” to the end of the tightening cycle, there were nonetheless several hawkish elements to the announcement:

- consumer spending has been stronger than expected, and the housing market has seen some pickup, suggesting more persistent excess demand in the economy.

- despite signs of increasing worker availability, labor market conditions remain tight and wage growth has been around 4%-5%

- three-month rates of core inflation have been more persistent than anticipated, running around 3.5%-4% since last September. Inflation is now expected to hover around 3% for the next year before gradually declining towards 2% by mid-2005, a slower return to target than forecast previously.

The updated economic projections from the Bank of Canada were particularly noteworthy. The central bank now sees GDP growth of 1.8% in 2023 (versus 1.4% in April), 1.2% in 2024 (versus 1.3%) and 2.4% in 2025 (versus 2.5%). Specifically, excess demand within the Canadian economy is now not projected to be eliminated until early 2024, three quarters later than previously forecast. CPI inflation is also forecast to be higher at 3.7% for 2023 (versus 3.5% in April), 2.5% in 2024 (versus 2.3%), and 2.1% in 2025 (also 2.1%) Overall, considering the upwards revisions to both growth and inflation forecasts, and with the BoC having raised interest rates at the past two meetings, we believe the onus is on both the growth and activity data to soften to dissuade the central bank from tightening further. For now, however, there appears to mixed evidence of a meaningful downshift in economic trends, meaning a September rate hike remains a possibility.

Growth in Activity Still Resilient

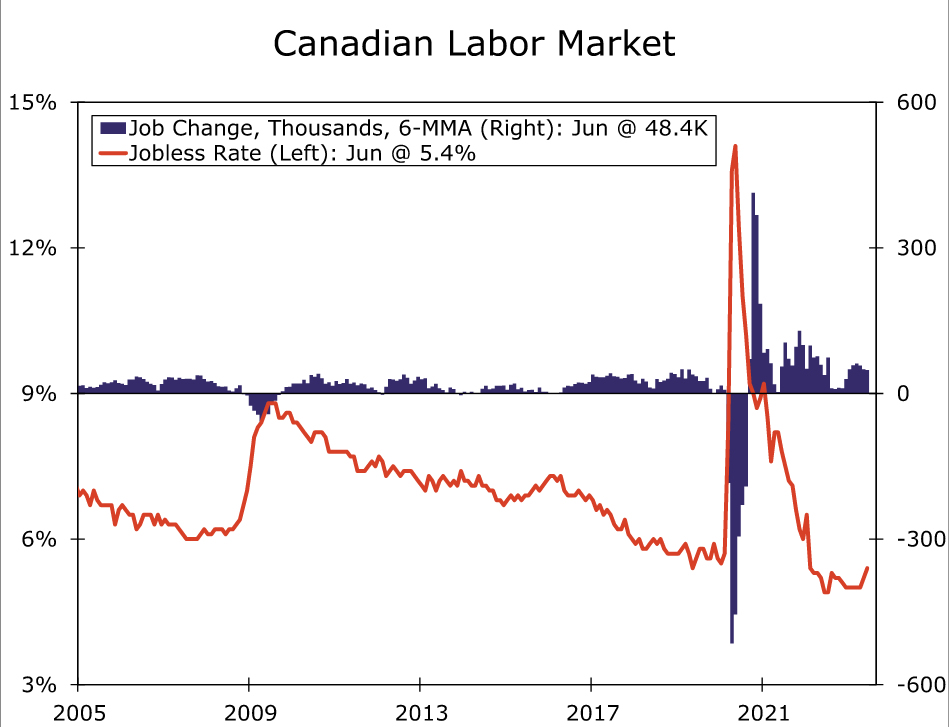

Recent data suggest growth in activity remains steady for now, and in some cases, even sturdy. June employment jumped 59,900, led by a full-time job gain of 109,600. The jobless rate moved slightly higher to 5.4% but, even so, is only moderately above the cyclical low of 4.9% from mid-2022. In terms of other activity indicators, retail sales showed a solid gain in April (1.0% month-over-month) and a further gain in May (0.2%), and although April GDP was flat for the month, Statistics Canada’s early estimate is for GDP to rise 0.4% in May. The main negative signal was the BoC’s Q2 Business Outlook Indicator, which fell further to -2.2. But that decline in sentiment would likely need to be confirmed by a slowing in the hard data to bring the BoC’s tightening cycle to a decisive end. Given the resilience so far this year, it is not clear to us that key activity data between now and the 6 September BoC policy announcement (July employment, May GDP and Q2 GDP, June retail sales) will show a meaningful slowing of momentum, thus keeping a September rate hike in play.

Core Inflation Still Persistent

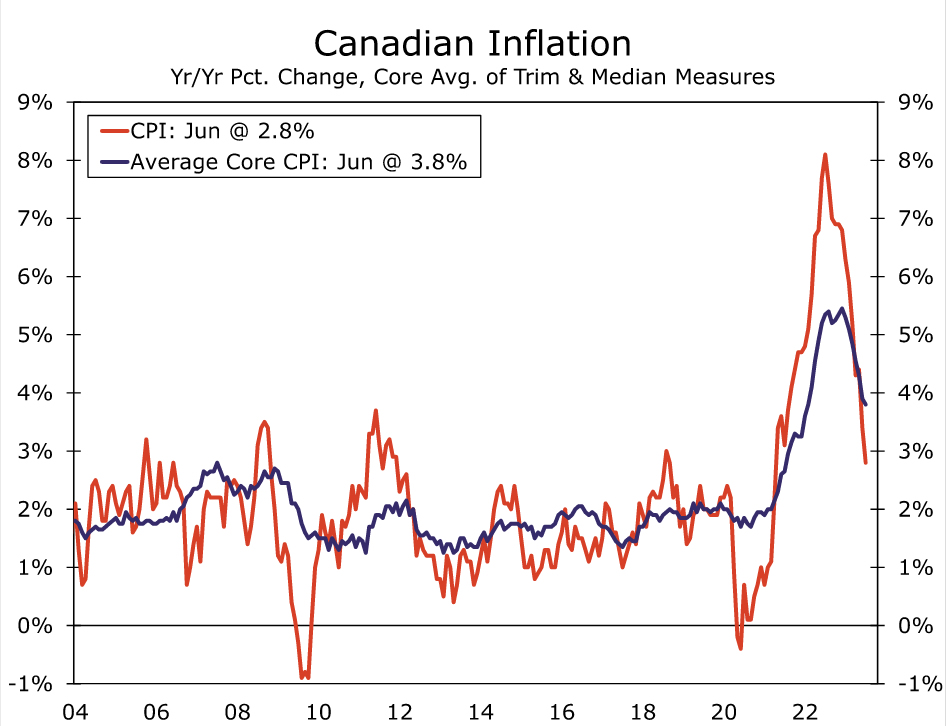

Meanwhile, on the price front, the progress in addressing underlying inflation pressures remains frustratingly slow. The June headline CPI slowed more than expected to 2.8% year-over-year, but the core CPI measures surprised to the upside, both slowing less than expected. Indeed, on a three-month annualized basis the disinflation of the core CPI measures has continued its stall in recent months, and in fact average core CPI inflation ticked higher to 3.8% on a three-month annualized basis in June. Without a significant downside surprise in the July CPI and/or a sharp slowing in July wage growth, the Bank of Canada’s concerns about “sticky” underlying inflation could still be present by the time of September meeting.

For now, we lean towards the Bank of Canada remaining on hold at its September meeting, and for its policy rate of 5.00% to represent the peak for the current cycle. However, that view is heavily data dependent and, as we suggested above, we believe the onus is on the data to soften perceptibly to dissuade the central bank from tightening further. The key figures between now and the 6 September BoC policy announcement include July employment, the July CPI, Q2 GDP, and to a lesser extent June retail sales. Should those data fail to show a perceptible softening, then the risk scenario of a 25 bps rate hike in September to 5.25% could crystalize.

The interest rate sensitivity of Canadian households should still see economic growth slow over time, though to date the impact of higher interest rates has perhaps been blunted to an extent by some deferral in mortgage principal payments. Still, as the BoC’s past interest rate increases bite more meaningfully on the consumer, we expect the Bank of Canada to bring its rate hike cycle to an end. Regardless of whether rates peak at 5.00% or 5.25%, we do not expect rate cuts to begin until well into next year, and forecast a cumulative 200 bps of rate cuts between Q2-2024 and Q4-2024, which would see the policy rate end next year around 3.00% to 3.25%.

raised its policy rate 25 bps to 5.00% at last week's announcement, and while BoC Governor Macklem suggested the end of the tightening cycle was close, there were nonetheless several hawlish elements in the announcement. In particular, the Bank of Canada expects excess demand within the Canadian economy to persist for longer than previously anticipated, while also raising its CPI inflation forecasts.){kind=link}