U.S. Highlights

- Retail sales disappointed market expectations overall in June, but underneath the surface sales in the control group, which are used to calculate consumption, were much stronger, rising 0.6% on the month.

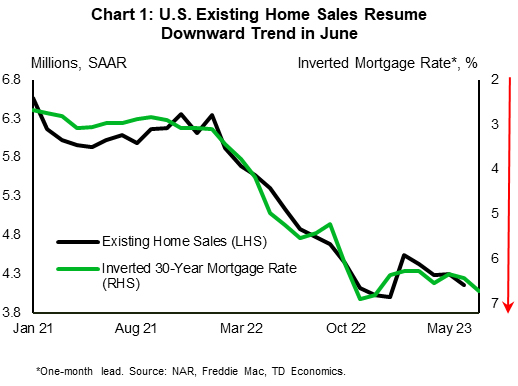

- Elevated mortgage rates and low inventories continue to weigh on existing home sales. The latter resumed their downward trend in June.

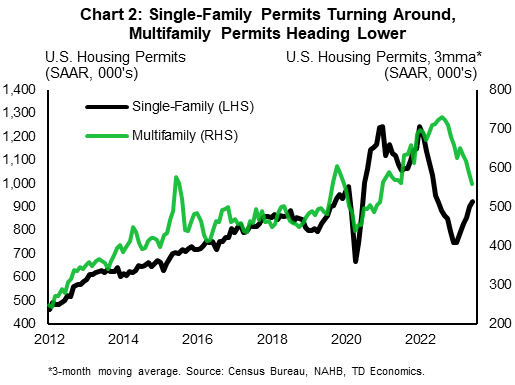

- Housing starts also fell in June. But, permitting data reveals a clear divergence between an upward trend in single-family permits and a downswing in multifamily permits.

Canadian Highlights

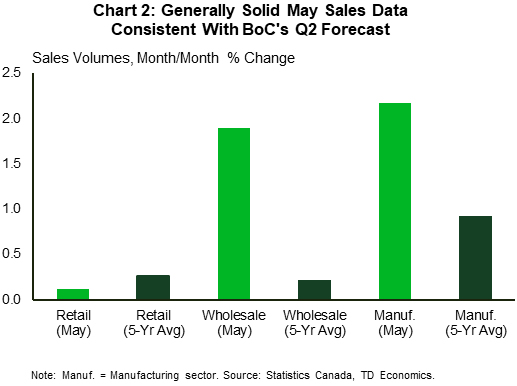

- Gains in manufacturing, wholesale, and retail volumes are roughly consistent with the Bank of Canada’s economic growth forecast for the second quarter.

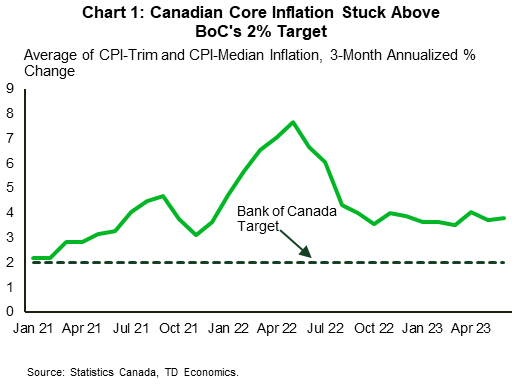

- However, the Bank’s preferred core inflation metrics continued to run too hot in June, with the average of CPI-trim and CPI-median inflation stuck too far above the 2% target.

- All told, developments this week likely did nothing that would move the Bank of Canada off of its hawkish stance.

U.S. – Fed Gearing Up for Another (Likely Final) Hike

Economic data this week wasn’t entirely positive, but it still pointed to an economy that continues to chug along at a decent clip. With no major red flags on the way, the Fed has the green light to hike the policy rate once more next week, before likely hitting the pause button.

While we expect the labor market to cool ahead, recent high frequency data still points to resilient demand for workers. Continuing jobless claims rose in the week ending July 8th, but initial claims continued to trend lower, easing for the second week in a row last week. With unemployment near multidecade lows, June retail sales suggested consumers are still spending, even as inflation bites into purchasing power. Headline retail sales growth was below market expectations, but an upward revision to the month prior helped provide some offset. The headline was dragged down by lower sales at gasoline stations, and at building material and garden equipment stores. A notable deceleration in sales at auto and food service establishments didn’t provide much support either. Stronger momentum was seen in the control group, which are used to calculate personal consumption expenditures, with sales rising 0.6% m/m – continuing a healthy pattern for the quarter.

Consumers weren’t as upbeat on homes, with existing home sales resuming their downward trend in June (see here). Elevated mortgage rates are likely to have been a major hurdle, given the tight relationship with sales recently (Chart 1). The higher rate environment has persisted through the first half of July, suggesting that there’s no turnaround in sight for the weakness in existing home sales. Low inventory is also restraining activity. There were only 1.08 million homes for sale in June – 170k less than last year and 840k less than in June 2019 – making for slim pickings.

As we note in a recent report, the tight conditions in the resale housing market are pushing more people toward the new home market. This is much to the delight of homebuilders, whose confidence has been improving rapidly since the start of the year. This optimism has been confined to the single-family segment, however. Multifamily homebuilders have been pulling back. Housing starts retreated in June in both segments, but permitting data reveals a clear divergence between the two segments (Chart 2). The recent softness in the multifamily space is consistent with a rise in the multifamily vacancy rate, and a record-setting number of units under construction in June.

All told, interest-sensitive areas of the economy remain under pressure. But with the employment backdrop continuing to hold up well, consumers still spending, and inflation appearing to move in the right direction, chances of a soft-landing look to have improved. The Federal Reserve is nonetheless expected to maintain a tightening bias over the near-term, and is almost certain to hike the policy rate once more next week. A Fed hike is fully priced in by markets at this point. Provided inflation continues to cool, this will likely be the Fed’s last hike this cycle.

Canada – Resilience is the Name of the Game

It was risk-on for financial markets this week, buoyed by a sense of optimism that the elusive soft landing is now seemingly more achievable for the U.S. economy. Notably, the TSX was tracking a 1% weekly gain (as of writing), while longer-dated bond yields pushed higher, and oil prices increased for the third straight week.

This week’s flow of top tier economic indicators portrayed a Canadian economy that continues to hang tough. While headline inflation showed some encouraging signs in June, surprising to the soft-side at 2.8% year-on-year, developments under the hood were less favourable. For one, the softness in the headline was due to base effects for energy prices, like gasoline. And, gasoline is likely to exert less of a year-on-year drag on the overall index in the months ahead.

In addition, Russia pulled out of a deal struck one year ago that ensured the safe export of Ukrainian grains. It also warned that ships servicing Ukrainian ports could be attacked (a threat reciprocated by Ukrainian authorities about ships servicing Russian-occupied Ukraine), while attacks at key ports have destroyed 60 thousand tons of grain and key infrastructure. Amid these tensions, prices for grains like wheat have predictably pushed higher. This could have knock-on effects to food prices in the coming months.

Most importantly for the Bank of Canada, core inflation is proving stubbornly persistent. Average core inflation (measured as the average of the BoC’s CPI-trim and CPI-median) accelerated in 3-month annualized terms (Chart 1).

The B.C. port strike is also hitting Canadian supply chains, creating backlogs that industry participants suggest will take months to clear. The work stoppage has already disrupted the flow of about $10 billion worth of cargo. The status of the labour dispute is still up in the air, but it seems to be moving in an encouraging direction.

Indicators of economic activity were almost uniformly strong during the week (Chart 2). Housing starts surged to 281k units in June – the highest in 9 months. Meanwhile, improving auto supply chains made their mark on manufacturing and wholesaling activity, with volumes in the former up 2% month-on-month (m/m) and 3% m/m in the latter. Retail sales were the one fly in the ointment, with volumes up a modest 0.1% m/m, while the preliminary estimate for June showed only flat growth in nominal sales.

While the activity data was generally firm, it was still consistent with economic growth expanding around 1.5% annualized in the second quarter, which is what the Bank of Canada’s expects. In that respect, this data would be unlikely to shift the pendulum on monetary policy (though policymakers should draw some comfort from evidence of softer consumer spending). Core inflation, however, continues to hover in ranges that are too high for the Bank’s comfort. All told, events this week likely did nothing to move policymakers off their hawkish stance.

{kind=link}