After a short break in June, the Fed is expected to announce its eleventh rate hike on Wednesday at 18:00 GMT. Most analysts think this will be the last rate increase of the tightening cycle that began in March 2022, but they will seek confirmation and look for signs of a possible rate cut next year. If the Fed dismisses these rumors and takes more time to assess the effects from previous tightening, the greenback could still gain new traction.

“Tightening is not over yet” is a phrase that has been ringing in investors’ ears for a couple of months now. The Fed has been hiking interest rates every single meeting since March 2022, from nearly zero to a range of 5.0-5.25%, applying its most aggressive monetary tightening policy by historical standards.

As it pledged, the Fed left rates steady in June, but it indicated that two additional quarter-percentage point rate increases are on the way in the remainder of the year. It’s not clear whether the Fed wanted to take some time to assess the impact from previous rate increases as the Fed chief explained, or rather provide a breather to the financial sector as the Treasury department refills its coffers following the scrapping of the debt ceiling. In any case, the hawkish guidance revived the dollar’s rally until a faster-than-expected drop in CPI readings flipped back those gains.

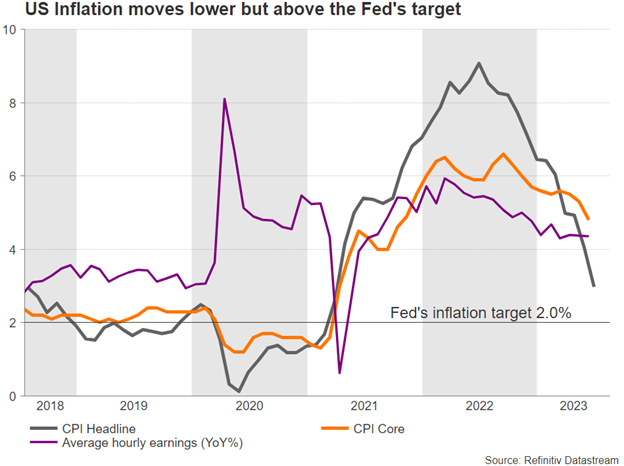

Headline inflation fell notably to 3.0% in June to the lowest since March 2021 and since before the aggressive rate increases started to take effect. The fall in the core measure to 4.8% from 5.3% before was also good news, though the gap with the central bank’s 2.0% target remained wide, suggesting that Americans are still feeling the pinch in their wallets. Hence, another 25bps rate hike is a done deal according to futures markets, especially as job openings keep outpacing job seekers and wage growth remains relatively robust compared to pre-pandemic levels. Besides, the Fed might want to follow the rate hike signal it sent during June’s gathering as the latest hawkish communication from Fed policymakers suggests.

What’s next?

Now the real question should be what the Fed will do after the summer. The majority of policymakers expected rates to rise twice by the end of the year in June, but investors are currently prepared for one-and-done. What’s more striking is that 2024 rate cut pricing persists despite policymakers consistently playing down the case, with investors foreseeing 125 bps of monetary easing. Hence, for the US dollar to preserve its recovery above the 100 level against a basket of major currencies, the Fed will need to dismiss the rate cut scenario and keep the door open for further tightening from September onwards. At this point, it is also important to mention that promises for lower interest rates could play out during the 2024 election campaigns, but that might be a story for another day.

Terminating the tightening phase at this current stage could be premature, as price stability is not in sight yet. Therefore, the Fed could still cite the resilience in the US economy and say that the fight against inflation is not over yet if it aims to extend its current hawkish guidance. But after three bank closures and given the uncertainty about when and how previous rate hikes will hit the economy, the central bank may adopt a neutral tone regarding the September meeting. There are two more CPI inflation and employment reports before its next gathering, while the Jackson’s Hole central bank symposium is scheduled for Aug.24-26. Therefore, the Fed might want to ensure a sustainable decline in inflation and see serious signs of a decelerating economy before announcing the end of the tightening phase.

Market reaction

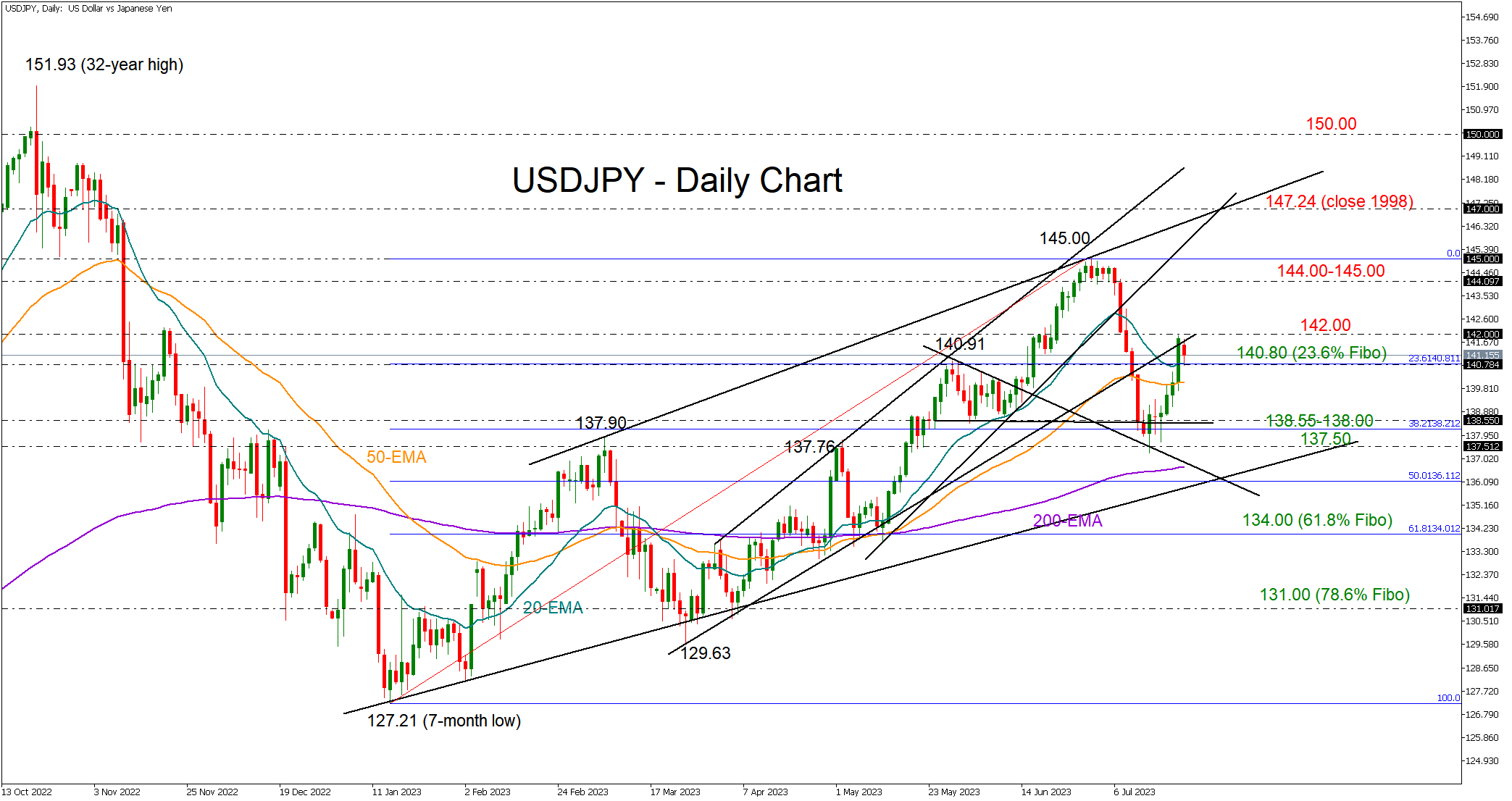

In FX markets, a neutral stance could limit dollar gains unless Powell judges that interest rates should stay elevated for longer and rate hikes could still happen in the coming months. In this case, dollar/yen could climb the 142.00 wall and run towards the crucial 144.00-145.00 resistance zone. The 147.00-147.24 region could attract attention in the event of steeper increases. A less hawkish communication from the ECB and BoJ this week could bode well for the greenback too.

Alternatively, if the Fed appears satisfied with the drop in inflation, questioning the need for additional rate increases, the US dollar could drift lower. Initial support could develop around the 140.00 level, a break of which could stabilize somewhere between 138.50 and 138.00. A decisive step lower could meet the 200-day exponential moving average at 136.70. Overall, any signals that the Fed has reached its terminal interest rate could trigger a new bearish wave.

{kind=link}