Summary

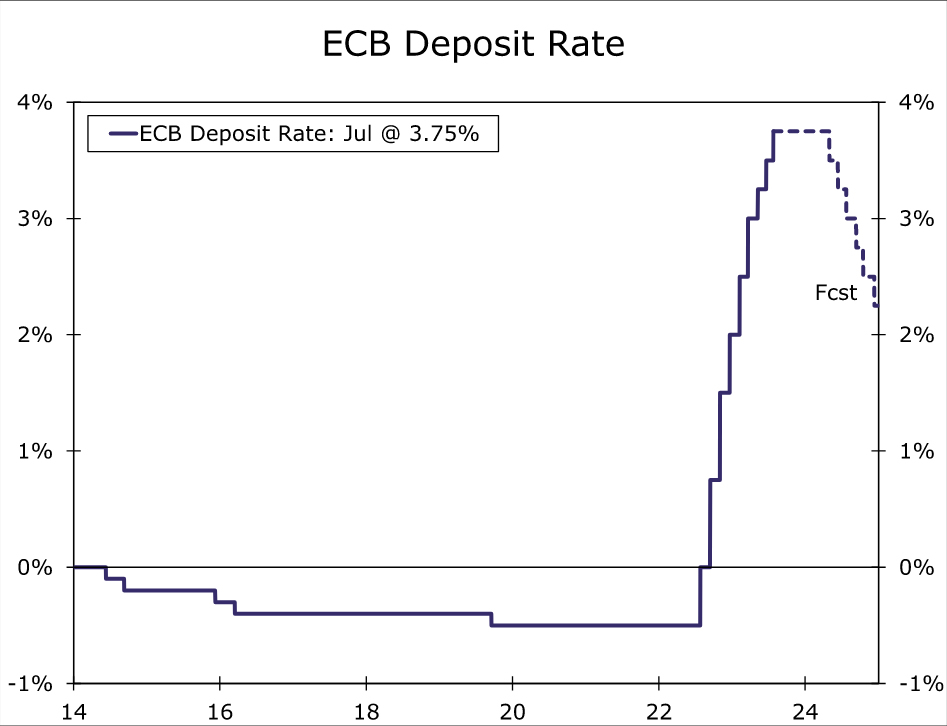

- The European Central Bank (ECB) raised its Deposit Rate 25 bps to 3.75% at today’s monetary policy announcement, matching widespread expectations. More significantly, the ECB sounded more downbeat on the economy and, in contrast to recent meetings, was cautious in offering any guidance about policy beyond this July meeting.

- Ahead of today’s announcement, we believed that a policy rate of 3.75% could mark the peak for this cycle. That view is unchanged, with sentiment and survey data likely to remain subdued for the time being, and so long as inflation continues to trend in a more favorable direction in the months ahead. We do not expect the ECB to begin cutting interest rates until well into 2024, once more convincing progress in reducing underlying inflation closer to the central bank’s target is evident.

European Central Bank Hikes Rates, But Cautious in Offering Policy Guidance

The European Central Bank (ECB) raised its Deposit Rate 25 bps to 3.75% at today’s monetary policy announcement, matching widespread expectations. More significantly, the ECB sounded more downbeat on the economy and, in contrast to recent meetings, was cautious in offering guidance about policy beyond this July meeting. Ahead of today’s announcement, we believed that a policy rate of 3.75% could mark the peak for this cycle. That view is unchanged, with sentiment and survey data likely to remain subdued for the time being, and so long as inflation continues to trend in a more favorable direction in the months ahead.

Overall, there were several comments in the ECB’s accompanying statement, and from ECB President Lagarde’s press conference, that pointed to a shift toward a less hawkish (or more dovish) approach than previously:

- The ECB said future decisions will ensure that key interest rates will be set at sufficiently restrictive levels. That is a change from previous terminology that interest rates would be brought to sufficiently restrictive levels.

- The ECB said past rate increases continue to be transmitted forcefully, and that financing conditions have tightened again and are increasingly dampening demand. ECB President Lagarde reinforced this, saying the central bank is definitely seeing policy being transmitted “strongly.”

- The ECB also decided to set the remuneration of minimum reserves at 0%.

- ECB President Lagarde said the near-term outlook has deteriorated, with manufacturing output held down by weak external demand while services activity was more resilient. The economy is expected to remain weak in the short run.

- Importantly, ECB President Lagarde said policymakers have an open mind on decisions in September and beyond, and that the ECB may vary from one meeting to another. Specifically with respect to September, Lagarde said “we are not going to cut”, and that September could be a hike or could be a pause. This is a significant contrast to recent meetings, where the ECB has explicitly signaled or promised a rate hike at the following meeting.

While outweighed by dovish comments, there were still one or two hawkish elements, most notably the ECB repeating that while inflation continues to decline, it “is still expected to remain too high for too long.”

Overall, while today’s announcement leaves the door slightly ajar for a September rate hike, we think that door may be closed by the time of that meeting. So long as activity data and confidence surveys remain soft (which we think is likely) and inflation trends, both headline and underlying, continue to improve (which we think is more likely than not), we believe the European Central Bank will hold its policy rate steady at 3.75%. Indeed, at this time we believe that 3.75% will be the peak policy rate for the current cycle, and that rates will be held at that level for an extended period. We do not expect the ECB to begin cutting interest rates until Q2-2024, once more convincing progress in reducing underlying inflation closer to the central bank’s target is evident.

raised its Deposit Rate 25 bps to 3.75% at today's monetary policy announcement, matching widespread expectations. More significantly, the ECB sounded more downbeat on the economy and, in contrast to recent meetings, was cautious in offering any guidance about policy beyond this July meeting.){kind=link}