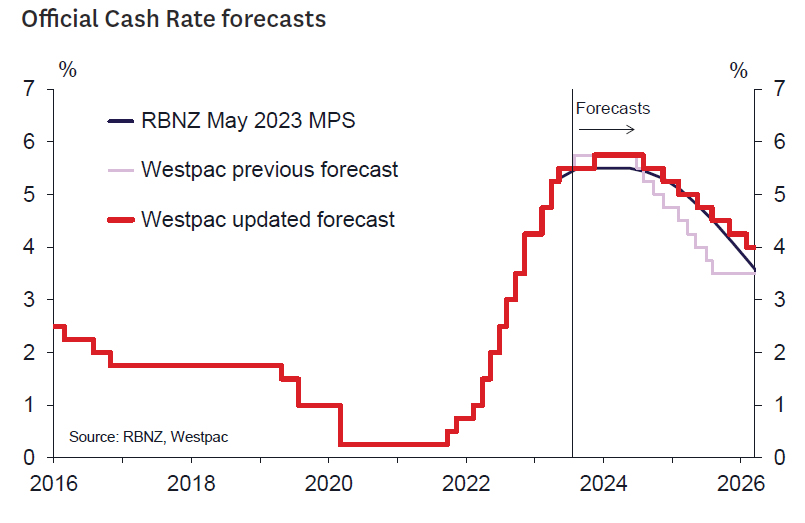

- We continue to see the RBNZ raising the cash rate to 5.75%, but in November instead of August.

- Evidence has accumulated suggesting persistent inflation pressures as feared.

- The economy is slowing from a very overheated position but is still growing.

- Even so, recent data have likely not been strong enough to overcome the RBNZ’s strong bias to keep the OCR at 5.5%

- We think the theme of economic resilience and sticky inflation will persist and will eventually force the RBNZ to act.

- With the current sticky domestic inflation pressures likely to ease only gradually, we see a slow rate reduction cycle beginning in the second half of 2024.

Since May 2023, we have had the view that the RBNZ would need to tighten policy further to ensure a timely fall of inflation to the 1-3% target range. This view was predicated on a sense that current very high rates of inflation would be slow to recede and that risks to the inflation outlook were tilted to a slower-than-needed fall. Strong net migration was seen as supporting both the housing market and the economy right at the time the RBNZ would have hoped that growth would be quickly slowing and providing much needed disinflationary impetus.

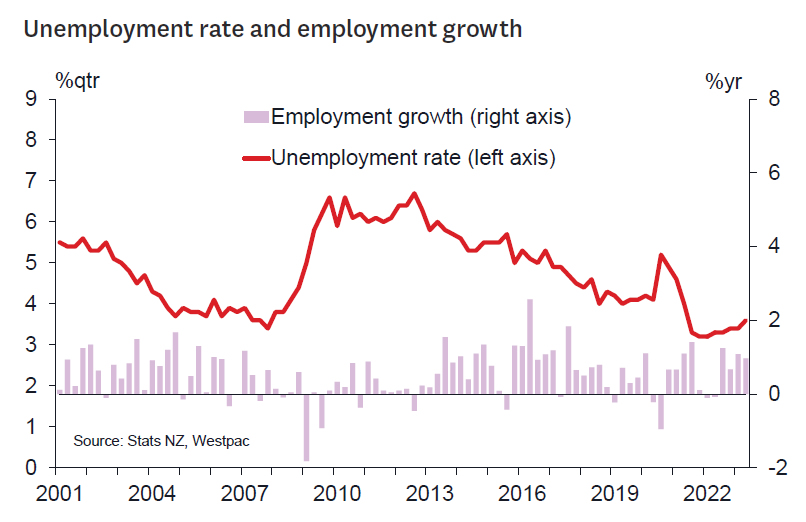

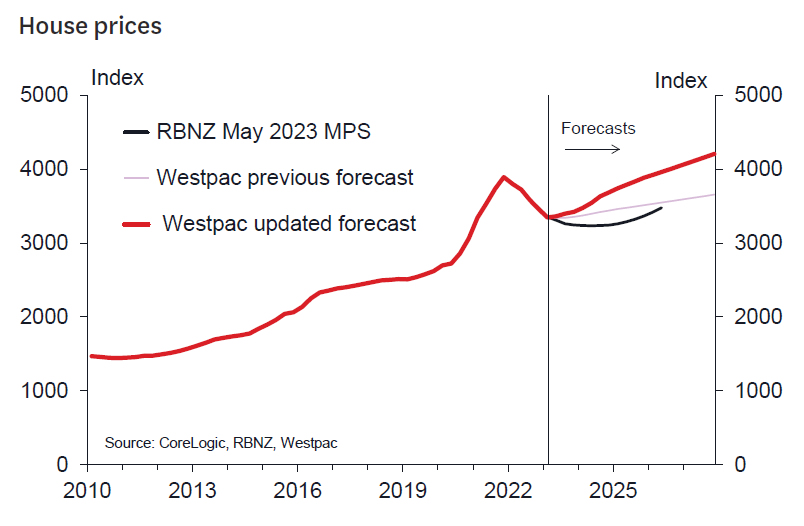

In large part, the accumulated evidence has supported our view. While GDP in the March quarter was somewhat weaker than expected, we also can see tangible signs that strong migration is supporting the economy. The housing market has exhibited strength compared to the relatively dire predictions of commentators earlier this year. Business and consumer confidence have bottomed out and are staging a tentative recovery, which is unusual if the end of the tightening cycle has been reached. The labour market has been a particular area of strength. Employment growth has remained strong in defiance of concerns of a recessionary economy. Large numbers of migrants have found jobs in a labour market that, while better balanced than a year ago, remains tight. The strong labour market has meant that household incomes have continue to grow strongly, leaning against the considerable disinflationary impact of the RBNZ’s 525 bps of interest rate increases delivered in recent years.

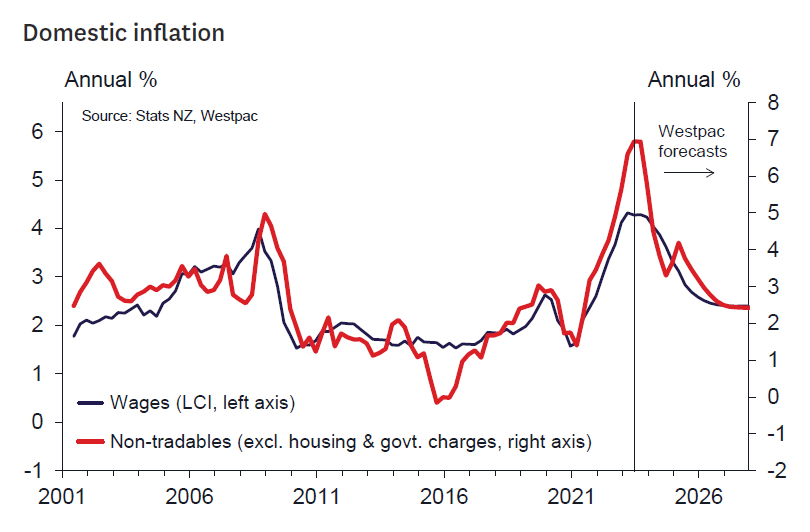

The June quarter CPI provided a timely reminder of upside risks to the inflation outlook. While annual headline inflation fell to 6%, in line with projections, lower imported inflation masked widespread and unexpectedly strong home grown non-tradables inflation. Non-tradables inflation is the part of inflation most impacted by RBNZ policy and fell only slightly to 6.6%. More generally, overall inflation remains far north of the promised land of the 1-3% target range. However, this strong and potentially concerning data needed to overcome the RBNZ’s very strong bias to keep the OCR steady at 5.5% until the second half of next year. A high hurdle was in place, and we don’t see the evidence as sufficient to move the RBNZ in August.

We retain confidence that recent trends will continue. The economy will likely continue to be supported by ongoing strong migration, the housing market will continue to strengthen, and inflation will only slowly moderate at current interest rates. We continue to doubt the economy will experience outright recession in the second half of 2023 as forecast by the RBNZ (although risks from the concerning situation in China and weaker agricultural commodity prices warrant keeping a close eye on that element of the forecast). But the data probably won’t be sufficient to budge the RBNZ Monetary Policy Committee in August – so we must play the man (the MPC) as opposed to the ball on this one.

Our forthcoming August Economic Overview will describe our new forecasts in greater detail. However, the bottom line is that the interest rate reductions we had previously expected to occur in the second half of 2024 will likely now occur more slowly, consistent with the RBNZ only easing cautiously as inflation moderates slowly. We suspect many other central banks will be taking a similar, cautious approach.

{kind=link}