U.S. Highlights

- Fitch became the second major credit rating agency to downgrade the U.S. from the top AAA rating, citing the growing fiscal debt burden and an erosion in governance.

- The U.S. economy added 187k new jobs in July, representing the slowest pace of hiring in over two years.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed credit standards tightened across the board in the second quarter, weighing on loan demand.

Canadian Highlights

- The Canadian economy shed employment in July, pointing to looser labour market conditions. Wage growth accelerated on the month but is expected to normalize in the coming months.

- Our internal data suggests that Canadian families tightened their purses in June. All in, it looks like personal consumption expenditures are poised to decelerate notably in the second quarter.

- With employment and consumption shifting into a lower gear, the Bank of Canada will feel less pressure to hike again.

U.S. – Tighter Credit Weighs on Resilience

Nearly twelve years to the day of the first U.S. credit rating downgrade in 2011, Fitch became the second major rating agency to lower its evaluation of the government’s creditworthiness. Fitch’s rationale was related to growing fiscal deficits in the near-term, medium-term fiscal challenges stemming from aging demographics, and a multi-decade erosion of governance. Since the decision was announced on Tuesday, Treasury yields rose and equities fell, with the ten-year Treasury up 11 basis-points (bps) and the S&P 500 down 1.8% as of the time of writing. Broader implications are expected to be muted as the U.S. economy continues to have strong fundamentals, however it comes at a time when credit standards are already tight.

Monday’s Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) showed that a significant share of banks had tightened business and consumer lending standards in the second quarter. Unsurprisingly, demand for most loan types fell over the period, with the only exception being credit card loans, which saw no change in demand. The economy is clearing feeling the effects of the rapid rise in interest rates over the past 17 months.

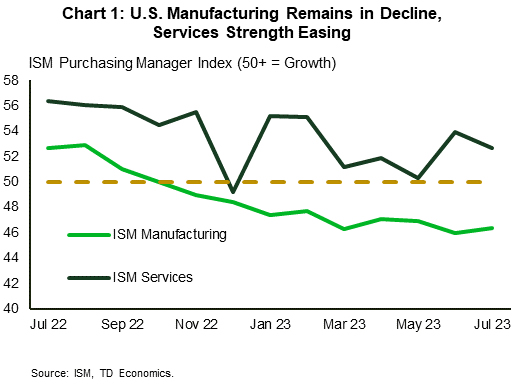

Despite tightening credit conditions, pockets of resilience remain. The ISM PMI data this week continued to show a notable divergence between the manufacturing and service sectors, with the former contracting for a ninth consecutive month and the latter expanding for a seventh straight month in July (Chart 1). Employment growth in both sectors slowed last month, but the services sector is still creating jobs as demand remains robust, whereas the manufacturing employment subindex hit its lowest level in three years.

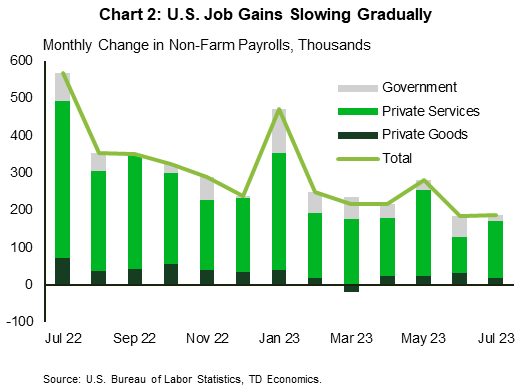

Looking more closely at the most recent labor market update, 187k jobs were created in July, which along with the revised reading for June, represent the slowest pace of job creation in over two years (Chart 2). While this puts job growth on a more sustainable footing, the labor market remains tight, as evidenced by the 4.4% year-on-year(y/y) growth in average weekly earnings in July. The moderation in hiring will be seen as a positive development by the Federal Reserve, but it is unlikely that they will take the prospect of further policy tightening off table until the sustainability of the trend is determined.

The Fed will get another important indicator next week in the form of the CPI inflation reading for July. June’s print showed core CPI fell below 5% y/y for the first time since December 2021 and the Federal Reserve will be looking to see further progress. With preliminary evidence that the cumulative effects of past rate hikes are working to cool inflationary pressures, we expect that the FOMC will leave the policy rate unchanged when they meet in September. However, they are likely to continue to emphasize the importance of incoming data on determining the future path of interest rates as the ultimate form of ‘landing’ for the economy becomes clearer.

Canada – Shifting Into Lower Gear

The weather cooled this week and so did the economy. A negative employment surprise helped prop the S&P TSX Index, which had suffered a steep selloff throughout the week, finishing 1.5% lower (at the time of writing). The 5-year Government of Canada Bond yield move lower, as financial markets recalibrated the expected probability of another Bank of Canada rate hike in September from 30% to 25%.

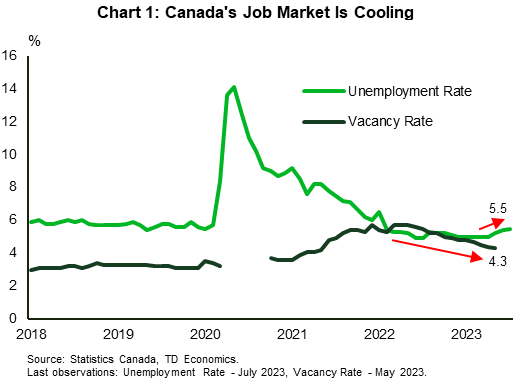

Canada’s economy shed 6k jobs in July, missing consensus forecast for 25k growth. Smoothing out the employment numbers over the peaks and valleys of the last three months, provides good evidence of cooling in the labour market: the three-month average change in employment moved decisively below the pre-pandemic average. Likewise, the unemployment rate ticked up to 5.5%, marking a third consecutive month of increases. The speed of the increase in the unemployment rate (half a percent in three months) suggests that a cooling trend is starting to take hold in the job market, even as the level of unemployment rate remains below the 2019 average. The vacancy rate (the share of unfilled positions relative to total number of vacancies) has also been on the downward trend since May 2022, shedding 1.4 percentage points over the course of the last year (Chart 1).

However, wage growth moved in the wrong direction. Average hourly earnings growth accelerated relative to the previous month, increasing by 5.0% over the past year. This is good news for consumer purchasing power, but bad news for inflation dynamics. Typically, looser labour conditions should be followed by slower wage growth with a bit of a lag. We expect wage growth will step back on the downward trend as the labour market cools further in the months ahead, helping to turn the heat down on inflation.

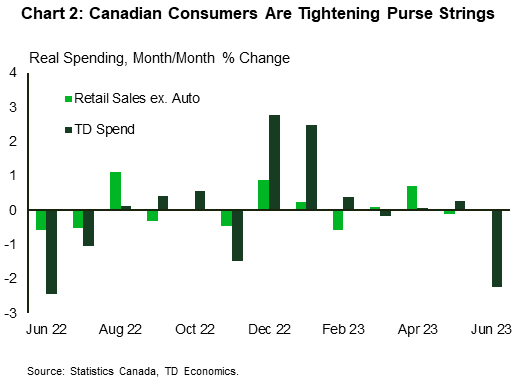

Another sign that the economy is shifting into lower gear is consumer spending. According to our internal card spending data, Canadian families tightened their purse strings in June, spending 2% less than a month prior, with sales up 1.6% versus a year ago, down from a 1.8% pace in May (Chart 2). The series are understandably volatile and affected by TD’s geographic concentration, but they usually offer a good directional guide for retail spending and personal consumption expenditures. A closer look at this data shows that the higher cost of living and rising interest rates are starting to catch up with consumers, as discretionary items, such as travel and entertainment were low on consumers’ shopping list in June.

With recent data incorporated, real consumption is expected to slow to below 1% in Q2 from an impressive 5.7% growth in Q1 2023. This is good news for the Bank of Canada, as it lowers the pressure for it to hike again at the time when cumulative hikes are starting to play a more prominent role in stemming consumer demand. We expect that the Bank will remain on pause for the rest of the year.

and the S&P 500 down 1.8% as of the time of writing. Broader implications are expected to be muted as the U.S. economy continues to have strong fundamentals, however it comes at a time when credit standards are already tight.){kind=link}