U.S. Highlights

- Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers grabbing attention.

- A slew of Federal Reserve speakers hint that the central bank may skip a rate hike at the next meeting, as the Beige Book (the Fed’s survey of economic conditions) suggests that the economy closed out the summer on a modest note.

- Oil markets were also on the move, after Saudi & Russian supply cuts were extended. Higher energy prices are a challenge to the needed cooling in inflation.

Canadian Highlights

- As widely anticipated, the BoC remained on hold, keeping the overnight lending rate at 5% while keeping the door open for another hike.

- The labour market moved towards greater balance in August with job gains not keeping pace with population growth, although wage growth remains too strong.

- The Bank of Canada needs to see more softness in the labour market to put a permanent end to this tightening cycle. We expect this to manifest more clearly by the October decision.

U.S. – Higher for Longer Seems Surer

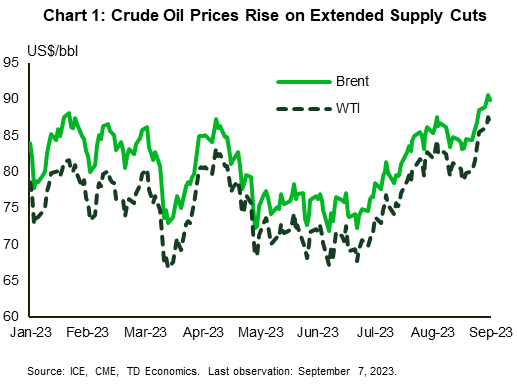

Hard economic data was thin on the ground over the Labor Day shortened week, with survey indicators and Fed speakers the main highlights on the calendar. Crude oil markets were also a bit livelier after Saudi Arabia and Russia both announced extensions to their supply cuts through to the end of the year.

Since July, Saudi Arabia has voluntary removed 1 million barrels per day (b/d) of crude from global oil markets. While the measure was cited to be temporary, it was already extended to September, with this week’s announcement extending it once again. Russia added their own export reduction of 300,000 b/d. On the day of the announcement, Brent crude, the international benchmark, rose 1.2% to close at $90.04 – exceeding $90 a barrel for the first time this year (Chart 1). Prices have since given back some of the gain, but the general move higher in oil prices over the past few weeks is likely to threaten efforts to tame inflation.

On that front, this week featured a full roster of Fed speakers. Governor Waller was also in the news making more dovish than usual statements. He noted that data showing a cooling job market meant the Fed should “proceed carefully”, and does not necessitate an imminent rate hike. Bostic echoed these sentiments. Logan noted that it could be appropriate’ to skip an interest-rate increase in September. Williams left whether the Fed would hike again as an open question, while Goolsbee, hinting at a higher for longer stance, sees a “golden opportunity” for the Fed to tame inflation without triggering a recession. All speakers emphasized that the Fed will be paying close attention to the data.

The Fed’s latest survey of economic conditions, the Beige Book, noted that the U.S. economy grew at a modest pace during July and August, relative to slight growth in the previous report. This was bolstered by a final bout of pent-up demand for leisure activities. Outside of leisure travel and a rise in auto sales due to better inventory, nonessential retail sales slowed. Job growth was generally subdued nationwide with wage growth elevated but expected to moderate in the months ahead. Prices for consumer goods fell faster than in many other categories. Demand for manufactured goods waned while the supply constrained single-family housing market continued to be challenged by higher financing costs and rising insurance premiums.

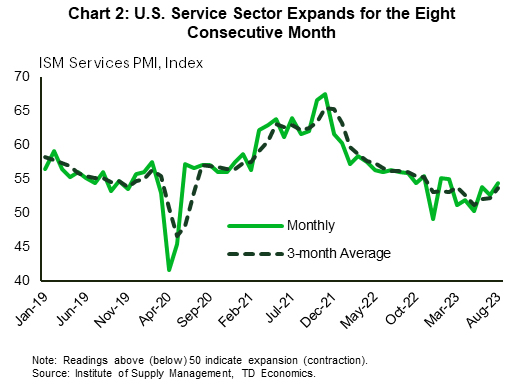

The ISM services index surprised to the upside this week, reaching a six-month high of 54.5 in August (Chart 2). The survey continued to highlight a service sector that is still in expansion mode, with survey respondents expressing positive sentiments about business and economic conditions. Beneath the headline, the positive details were an increase in business activity (+0.2 pts), new orders (+2.5 pts), and employment (+4.0 pts).

The tone of the economic news this week is likely to keep policymakers in a wait and see mode. Consumers are keeping the service sector humming along, even as the labor market cools. All good news for the Fed, but higher energy prices remain a wildcard that will require close monitoring so as not to undo the progress on inflation thus far.

Canada – Finding a Balance

There was no surprise in the Bank of Canada’s announcement this Wednesday. As widely anticipated, the benchmark overnight lending rate remained at 5%. In the wake of the decision, the market implied policy rate moved lower by roughly 10 basis points over the week. This shift put more pressure on Canadian dollar. When measured in U.S. currency, the loonie got cheaper by almost one cent. The loonie is down nearly three cents since the BoC’s July interest rate announcement.

This was the second pause in this tightening cycle, but this time, the BoC did not characterize it as such. The tone of the message remained hawkish, with Governor Macklem reiterating his loud promise “to take further action”, if needed. Indeed, the first time the Bank went on hold earlier in the year markets resolved that rate cuts won’t be too long in coming. This helped ease financial conditions enough to reinvigorate the housing market and consumer spending in the first quarter.

Fifty basis points of hikes later, the risk of overtightening is higher as weakness in economic activity is more convincing. Recent readings of GDP, retail trade and home sales provide compelling evidence that demand is moderating. Nonetheless, the labour market continues to give mixed signals. August’s headline employment gain at 40K new jobs was twice as high as expected by the consensus, but the pace of employment growth is lower than population growth, leading to a slight rise in the unemployment rate – at least at the second decimal place.

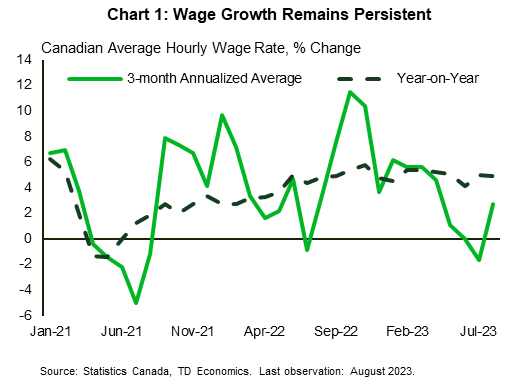

Meanwhile, headline wage growth eased slightly in August (on a year-on -year basis). The three-month annualized average change in wages did pick up, but still points to a cooler pace of wage gains in the months ahead (Chart 1). Overall, the pace remains too strong for broad inflation to move to its target. Additionally, when coupled with a decline in productivity, high wage growth means unit labour costs are rising for businesses. In a strong demand environment, businesses may pass this onto consumers, keeping inflation up, or they may cut costs by reducing investment or shedding workers.

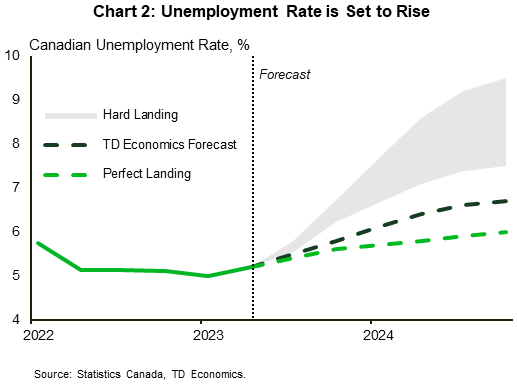

Persistent wage pressure remains the most unfading signal of an unbalanced labour market. Still, we expect it to move to a lower trajectory as employees’ ability to negotiate a pay raise diminishes as job vacancies become scant. As outlined in our recent report, the job market has reached an inflection point, setting a path for the unemployment rate to rise to 6.7% over the next year, slightly overshooting the level required to balance the market (Chart 2).

All told, while the market odds of another rate hike are lower, the Bank of Canada will need to see more softness the labour market and continued slowing in economic momentum through the rest of this year to remain on the sidelines. Until the Bank meets again on October 25th, we will have several economic releases, including two more inflation reports. By then, we expect the progress in rebalancing demand and supply in the economy will manifest more clearly, putting a permanent end to the tightening cycle.

suggests that the economy closed out the summer on a modest note.){kind=link}