- The Fed maintained Fed Funds Rate target unchanged at 5.25-5.50% as widely anticipated, but surprised hawkishly with clearly more optimistic projections.

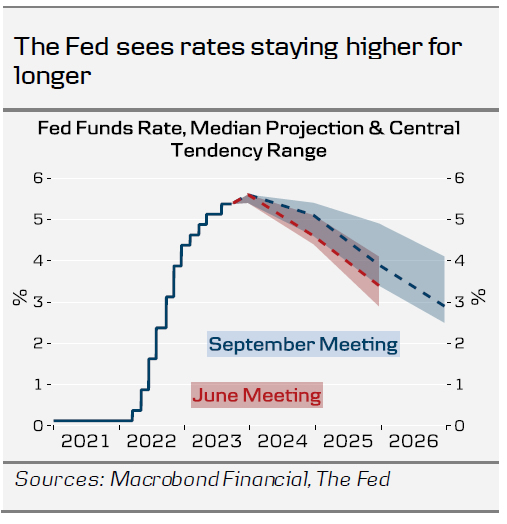

- Median growth forecasts were revised higher for 2023-2024, warranting a 50bp upward revision to both 2024 & 2025 median rate projections.

- We remain more pessimistic on the economic outlook, and make no changes to our Fed call. We still expect no further rate hikes, and quarterly 25bp cuts starting from Q1 2024.

Powell delivered a ‘hawkish hold’, as the updated economic projections outlined an optimistic path towards soft(-er) landing. Real GDP forecasts were revised up to 2.1% (from 1.0%) for 2023 and 1.5% (from 1.1%) for 2024, while inflation forecasts only received minor adjustments. Median forecast for unemployment rate was also revised higher, with the peak now seen at only 4.1% in 2024-2025 (from 4.5%).

Powell underscored that the more optimistic growth outlook warrants rates remaining higher for longer, and the median ‘dots’ were revised up by 50bp for both 2024 (5.1%) and 2025 (3.9%). Markets erased some of the cuts priced in for 2024, with 2y UST yield rising some 12bp. Powell mentioned solid realized data and recovering real income growth as factors lifting the outlook, and while the looming government shutdown and UAW strike were seen as downside risks, they have not materially impacted the baseline view for now.

The FOMC statement was mostly unchanged, economic growth was described as ‘solid’ rather than ‘moderate’ while job gains were seen ‘slowing’ rather than ‘robust’. Powell also maintained strong emphasis on data-dependency.

A key factor driving the renewed hawkish market reaction during the press conference was Powell’s surprisingly open view regarding potentially higher neutral rate. While the longer-term Fed Funds Rate estimate was unchanged at 2.5%, Powell mentioned that it does not necessarily suggest that neutral rate could not be higher, which in turn would suggest monetary policy is not as restrictive as previously thought. While not our base case, we discussed the idea and potential drivers back in August, see Research US – Could investment boom pave the way for a soft landing?, 22 August.

In any case, the Fed anticipates that the economy is going to remain more resilient to the effects of restrictive monetary policy than we do. In our Fed preview, 15 September, we highlighted recent tightening in financial conditions and already restrictive level of real rates are key headwinds for the economy, and ever since the latest University of Michigan consumer survey confirmed a further decline in inflation expectations. Powell explicitly mentioned that higher real rates due to declining inflation could warrant earlier rate cuts, and we still stick to our view of quarterly 25bp cuts starting from Q1 2024.

Also, while the ‘dots’ were 7-12 in favour of one more rate hike later in the year, we doubt it will materialize. This would imply downward pressure on UST yields going forward, but if we will be proven too pessimistic on our macro outlook by incoming data, rates are likely to remain higher for longer than what we assume.

FX: Near-term USD tailwinds could be fading

EUR/USD moved lower around a half figure on the hawkish hold from the Fed. The outcome was about as hawkish as the Fed could have engineered without actually delivering a surprise hike. Despite the ongoing USD strength, we think there could be some potential for some EUR/USD tailwinds in the near-term. We think that peak policy rates, improving manufacturing sector relative to the service sector and/or easing pessimism priced on China could add some support to EUR/USD within the next month. On the longer horizon, however, we maintain our strategic case for a lower EUR/USD, expecting the cross at 1.03 in 12M.

{kind=link}