Summary

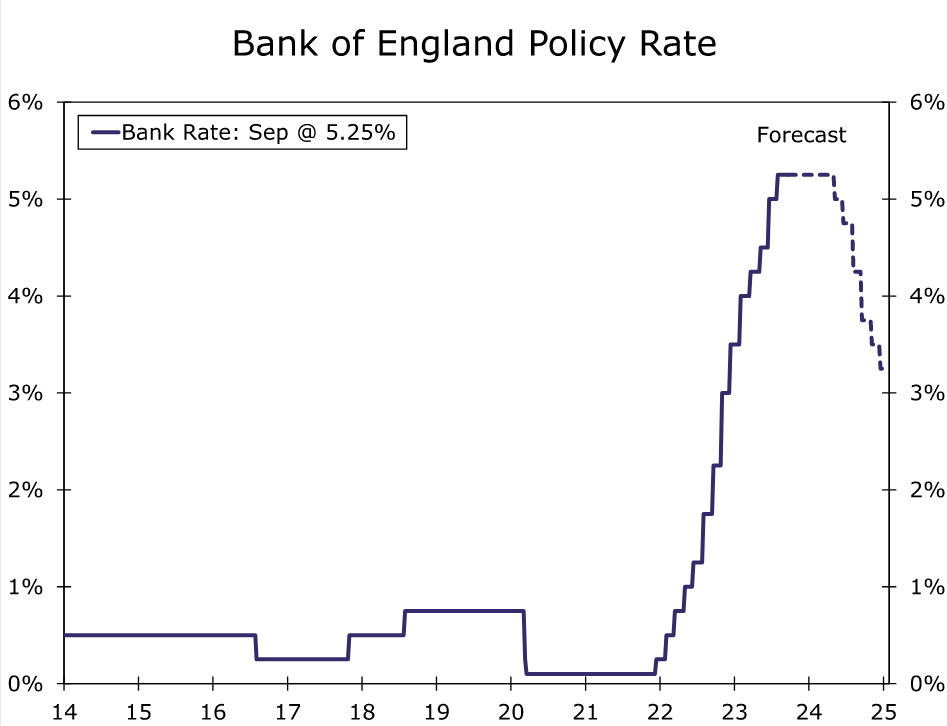

- In what was a finely balanced decision, Bank of England (BoE) policymakers held their policy rate steady at 5.25% at today’s monetary policy announcement. In a significant change, the BoE said there were mixed developments on indicators of inflation’s persistence, noting slower varied signals on wage growth and slower services inflation.

- We believe today’s interest rate pause could also represent an interest rate peak. The BoE said it views the current level of interest rates as restrictive, and that monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation towards target.

- We do not anticipate an initial 25 bps rate cut until the May 2024 meeting, and see the BoE’s policy rate ending next year at 3.25%. Today’s decision also represents a loss of interest rate support for the pound. In that context, we view the risks as tilted towards further U.K. currency weakness through early 2024, and cannot rule out a move towards $1.2000 or below.

Bank of England Holds Rates Steady

In what was a finely balanced decision, Bank of England (BoE) policymakers held their policy rate steady at 5.25% at today’s monetary policy announcement. BoE policymakers voted 5-4 to keep interest rates unchanged, with four policy committee members favoring a 25 bps increase. Separately, the BoE continued with its quantitative tightening, saying it would reduce the size of its balance sheet by £100 billion over the next 12 months.

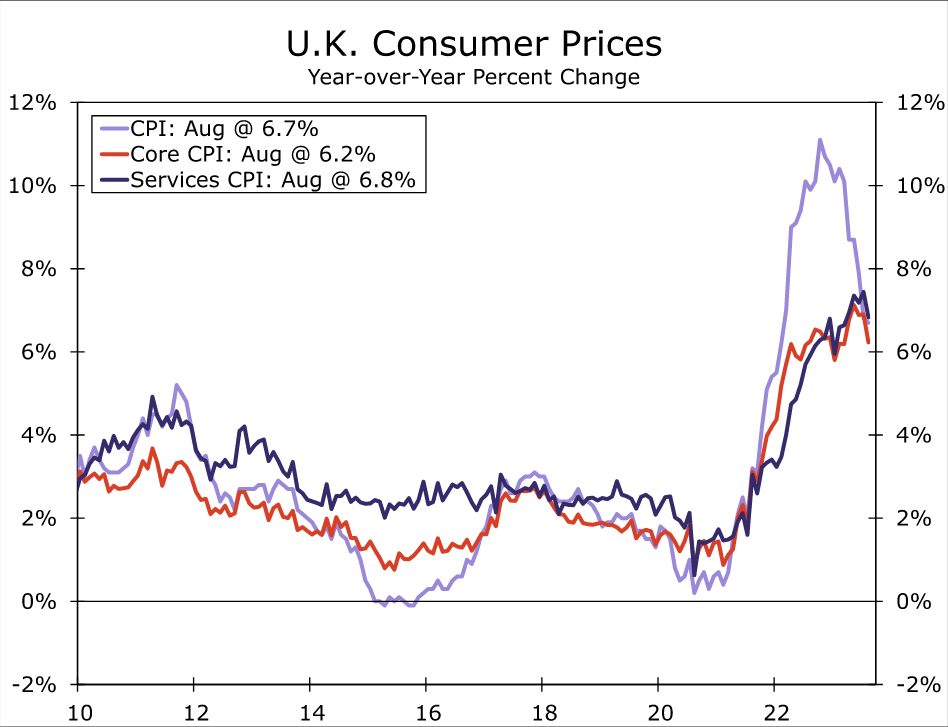

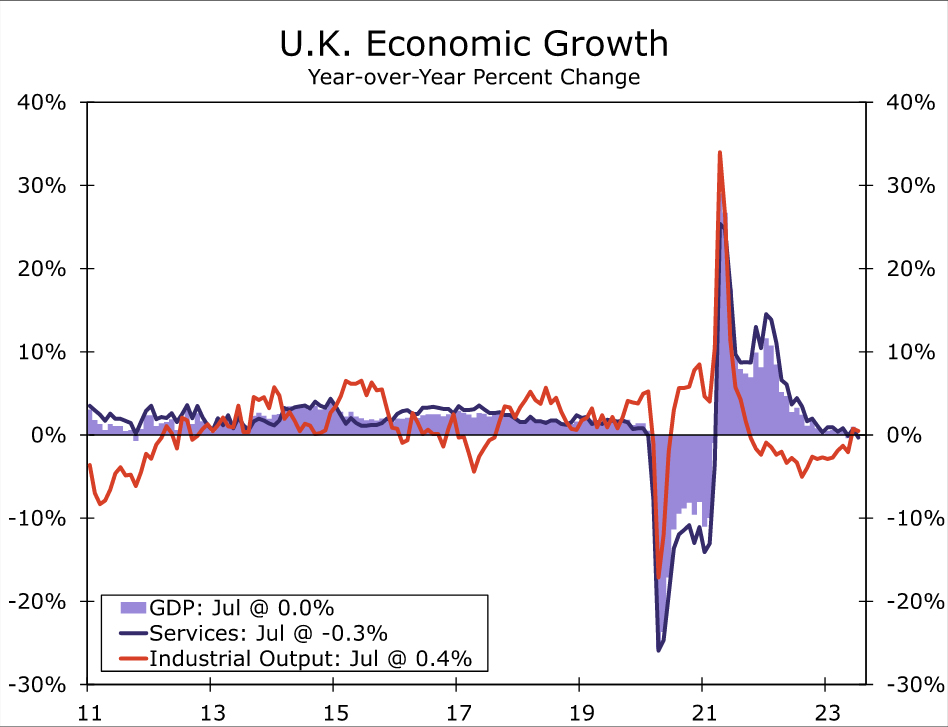

In holding interest rates steady, the Bank of England in a key change noted mixed developments on indicators of inflation’s persistence. The central bank said the recent acceleration of average weekly earnings is not consistent or apparent in other wage measures, while also noting downside news on services inflation, which slowed to 6.8% year-over-year in August. Separately, the Bank of England also said core goods inflation is much weaker than had been expected. Finally, the Bank of England also said there are increasing signs of some impact of tighter monetary policy on the labor market and on momentum in the real economy more generally. On that front, we note that July GDP fell 0.5% month-over-month, while the unemployment rate rose to 4.3% in the three months to July.

Policy Rate Pause Could Also Be A Policy Rate Peak

In our opinion, there are also indications that today’s policy rate pause could be a policy rate peak. The BoE said “given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance is restrictive”, while adding that “monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term.” We view that language as consistent with the Bank of England keeping rates at the current level for an extended period. The central bank did leave the door open to further rate hikes, saying a further tightening in monetary policy would be required if there were to be evidence of more persistent inflation pressures. However, given the weakening in the economy to date and the mild U.K. recession we forecast, along with the more significant deceleration of inflation that now appears to be underway, we believe such rates hikes are unlikely to eventuate.

As a result, we now forecast that the current policy rate of 5.25% will be the peak for this cycle. We do expect rates to remain at that level for some time and, following a mild recession beginning from late this year and as CPI inflation moves closer the 2% target, forecast an initial modest 25 bps rate reduction only by the time of the May 2024 policy meeting. We expect the pace of rate cuts to gather momentum through the rest of next year, and see the Bank of England policy rate to end next year at 3.25%. From a currency perspective, today’s decision to pause and the probable end to policy tightening represents a loss of interest rate support. As a result and even though the GBP/USD exchange rate has already moved below our medium-term target of $1.2300, we think the risks remain tilted toward further sterling weakness through early 2024. In that context, a move to $1.2000 or below cannot be ruled out.

policymakers held their policy rate steady at 5.25% at today's monetary policy announcement. In a significant change, the BoE said there were mixed developments on indicators of inflation's persistence, noting slower varied signals on wage growth and slower services inflation.){kind=link}