The Reserve Bank Board meets next week on October 3 with Governor Bullock presiding over her first meeting.

We are certain that the Board will decide to continue the pause that began at the July meeting.

The Board meetings which occur immediately before the release of the quarterly Inflation Report and the updating of the staff’s forecasts (namely those in April, July and October) have been ones where the Board has shown a preference to pause – even during this long tightening cycle.

At the October meeting last year, there was a surprise slowing in the pace of tightening from 50bps to 25bps; in January this year there was no meeting; April saw the first pause in the cycle after consecutive hikes in February and March; and July saw a pause after consecutive hikes in May and June.

Rates remained on hold in August and September so a move in October would be very surprising.

That does not preclude the Board from continuing to consider the two options – an increase of 0.25% or hold rates steady.

After describing the decision in June as “finely balanced” the Board has described the “on hold” decision as the “stronger one” in subsequent meetings – indicating a clear preference for the pause option.

The October decision statement is likely to repeat the sentiment, “members noted that some further tightening in policy may be required should inflation prove more persistent than expected.”

That statement is a sensible position for a cautious central bank to hold, while inflation remains above the target band, while also providing some residual support for the vulnerable AUD (recently fallen below US64¢).

It is unlikely that the August monthly Inflation Indicator is a game changer. Annual inflation lifted from 4.9% in the year to July to 5.2%, mainly reflecting a 9% lift in petrol prices. A more reliable monthly Indicator than the Trimmed Mean monthly, which excludes volatile items, actually slowed from 5.8% to 5.5%.

The more comprehensive September quarterly Inflation Report will be watched closely by the Board and the market – with information from that quarterly update to feed into the RBA’s considerations at the November Board meeting.

While the Bank does not publish its forecasts for annual inflation to the September quarter it does provide December and June.

It is currently expecting inflation to fall from around 6.0% in June (Trimmed Mean 5.9%; Headline 6.0%) to around 4% in December (TM 3.9% and Headline 4.1%).

Results around 5% for the September quarter would be in line with their expectations. These numbers would also have to be considered in the context of ongoing weakness in household spending; signs of a turning point in the labour market (job vacancies fell 9% in the three months from May to August); and real concerns around the outlook for China.

The market is currently giving around a 40% chance of a rate hike in November lifting to 90% in March.

Despite this market pricing, which is also indicating no rate cuts until 2025 we expect that the cash rate will remain on hold until August next year when the first rate cut can proceed. Our forecast for the conditions the Board will be facing by then will be an inflation rate that has fallen from 4.1% to 3.4%; an unemployment rate of 4.5%; and economic growth through the year to June of 1.0%.

One argument we see for the expected rate hike by March is that Australian rates are just too low relative to other central banks.

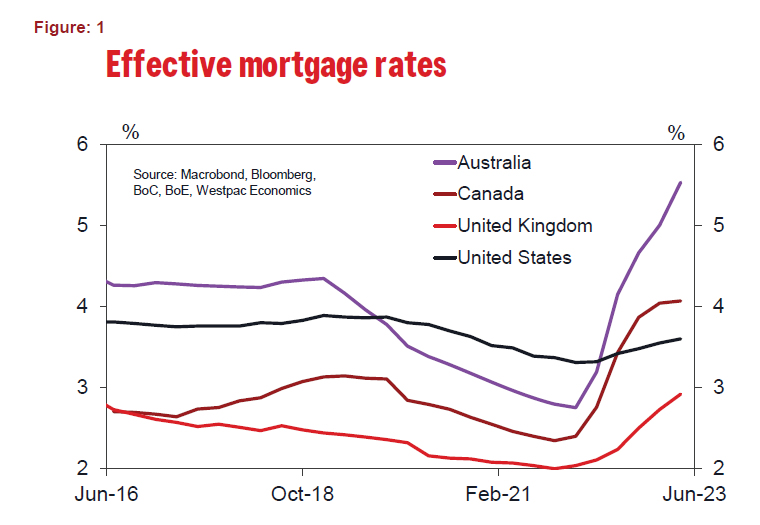

Figure 1 compares the movement in the effective mortgage rate for Australia and other majors.

Australian borrowers have been much more sensitive to the recent sharp tightening cycle than other countries due to the low proportion of fixed rate loans – even recognising that the share reached around 35% in 2022. Effective mortgage rates have lifted from 3.3% to 3.6% in the US compared to 2.75% to 5.6% in Australia.

The impact, which from Australia’s rates holding well below US rates has been through the AUD/USD, which remains fragile at US64¢.

But this negative yield differential with the US is not a new story.

The “new story” is the relentless upgrade of the growth outlook for the US economy. Earlier this year Consensus forecasts for US growth in 2023 were around 0.4%, with general expectation of a recession at some time over 2023 and into 2024. Recent Consensus and FOMC forecasts have lifted growth in the US for 2023 to 2% while talk of recession has been scaled right back.

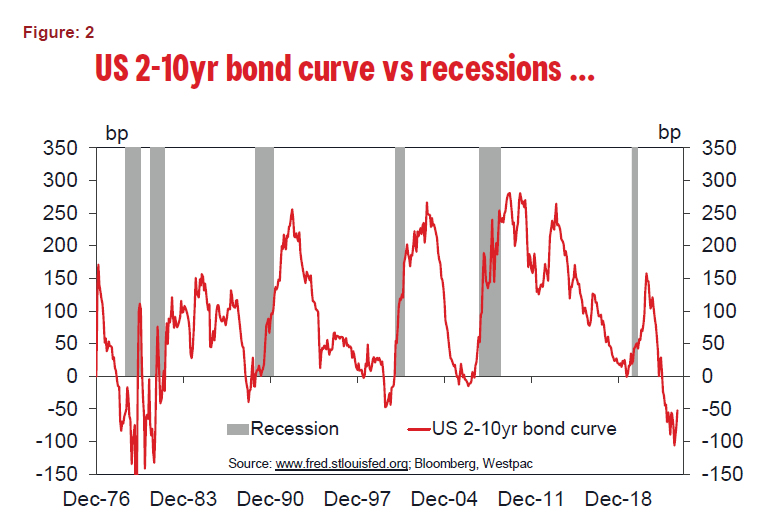

As we show in Figure 2, the shape of the US yield curve continues to be consistent with a recession. But in recent weeks yields have risen and the curve has begun to flatten – a bear flattener where long bond rates have risen by more than short rates.

That lifting of the yield curve has also impacted the near term prospect for the RBA, but reflects, in our view, more of a curve movement driven by rising long rates than the expectation of an RBA rate hike.

The decision by the FOMC to issue guidance in its “dot plot” that there will only be two rate cuts next year rather than four has had some impact but, at this stage, surprisingly less than might have been expected. The key reason why the FOMC scaled back its rate forecasts was a reduction in its forecast for the unemployment rate by end 2024 from 4.5% to 4.1%. Westpac is more cautious on the US economy next year, expecting the unemployment rate to reach around 5%. We have therefore retained our call for four FOMC rate cuts in 2024.

However, we have sharply lifted our profile for the US ten year bond rate by end 2024 by 60bps to 4%. That still leaves a slightly inverse yield curve for the US by end 2024.

Despite the FOMC cutting rates next year bonds may be even less attractive than we are expecting. With the US economy avoiding a recession and the FOMC cutting rates the market may require a regular shaped yield curve much earlier than we are currently expecting.

That need for a regular shaped curve signals a sharp rise in bond rates. A potential outcome would pressure the equity market.The issue here is that despite the sharp tightening cycle which the FOMC has implemented equity markets have been resilient – limiting the main channel through which FOMC policy can impact the US economy.

As we saw in 2018, any major negative outcome in the US equity market is likely to trigger an aggressive response from the FOMC.

A much more rapid easing cycle from the FOMC in 2024 would take pressure off the AUD; and certainly, set the scene for the RBA to follow.

{kind=link}