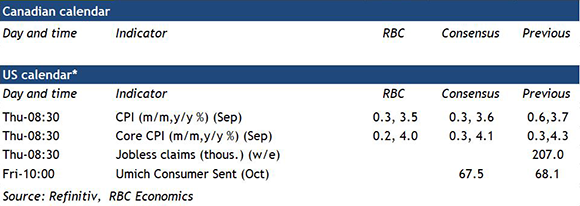

All eyes will be on U.S. inflation data in an otherwise quiet week of economic data releases. CPI growth likely looked a little better in September – we look for a slowing to a 3.5% year-over-year rate from 3.7% in August. Oil prices are still high, but gasoline prices were little changed in September (on a seasonally adjusted basis) after jumping 10.5% on a month-over-month basis in August. Grocery price growth has slowed substantially after surging higher last year, and we look for another tick down in the year-over-year rate of food price growth (to 3.6%) in September.

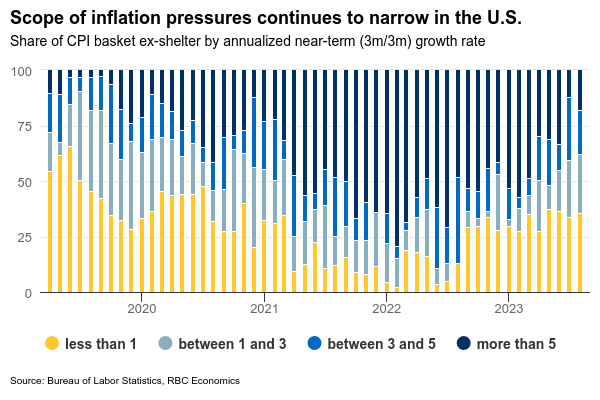

Fed policymakers will be more focused on ‘core’ measures that are more likely to be impacted by domestic economic conditions than global factors like energy price movements. Those measures have also slowed substantially. We look for price growth excluding food & energy products to edge down to a 4.0% year-over-year rate in September from 4.3% in August. The scope of price gains has continued to narrow – the share of the ex-shelter CPI basket growing at a 3% or greater rate over the last three months shrunk to 38% from 87% a year ago and the Fed’s ‘super-core’ (services prices excluding rent) averaged 2.2% growth at an annualized rate over the last three months.

The Fed has signaled that future interest rate decisions are firmly ‘data dependent’ – and, to-date, easing inflation pressures have come alongside an exceptionally resilient economic growth and labour market backdrop. The September jobs report showed strong employment growth, but wage growth continued to slow, reaching the lowest yearly pace in two years. The unemployment rate held at 3.8% and lower job openings and quit rates continue to point to softening in hiring demand that will eventually feed through to higher unemployment. The Fed won’t hesitate to respond with higher interest rates to cool the economy and keep inflation in check. Although our own base-case assumes that won’t be necessary with the recent run of economic resilience not expected to last.

after jumping 10.5% on a month-over-month basis in August. Grocery price growth has slowed substantially after surging higher last year, and we look for another tick down in the year-over-year rate of food price growth (to 3.6%) in September.){kind=link}