U.S. Highlights

- And just like that, the Fed’s short-lived pause is likely done after a bevy of positive economic data show an incredibly resilient economy.

- This morning’s payrolls report showed a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months.

- Financial conditions have tightened this week, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target.

Canadian Highlights

- The relentless upward march in bond yields continued this week, pushing riskier assets lower. Oil plunged, dragging down the TSX and Canadian dollar.

- Multi-year highs for rates flag further softness in Canadian housing markets. Data from local real estate boards showed falling sales and prices last month, alongside a concerning rise in supply.

- Canada added 63k positions in September – shattering expectations – and wage growth accelerated. While other details were softer, the odds of another rate hike have gone up.

U.S. – The Jobs Machine Keeps Whirring

And just like that, the Fed’s short-lived pause is likely done. Markets have responded aggressively to a bevy of positive economic data and sent ten-year government bond yields up 20 basis points since the start of the week. The bond rout had abated mid-week, only to be abruptly undone by Friday’s gangbusters payrolls report that sent yields surging. This week’s data stream shows an economy that continues to shrug off a higher policy rate, likely forcing the Fed to action before the end of the year.

With all eyes focused on this morning’s payrolls report, it didn’t disappoint with a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months. The print for September effectively doubled up on the market’s expectations. Industry figures lined up with this week’s ISM services index, as gains were concentrated in the services sector – with leisure and hospitality leading the way.

There isn’t much need to address the details. The strong addition to payrolls squares with the Job Opening and Labor Turnover Survey (JOLTS) that came earlier this week and showed job openings jumped in August, reversing the two prior months’ declines, as firms continue to search for talent. While the number of open positions continues to trend lower from its pandemic-era surge, there remain a whopping 44% more job openings as of August than there were in December of 2019.

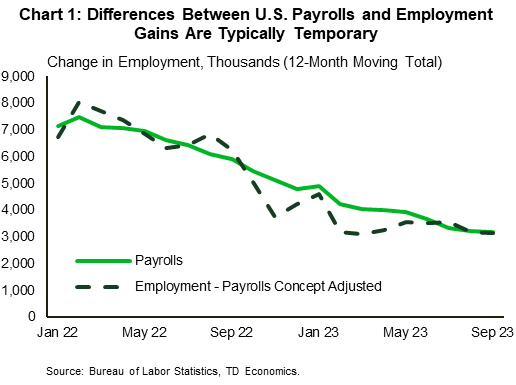

The labor market is tight with jobs aplenty. That said, one apparent contradiction in the report is the wedge between the household employment and payrolls reports. Despite the stellar jobs gains, the unemployment rate was unchanged (3.8%), the labor force participation rate didn’t budge and the number of employed people only rose by 86k. However, deviations of this size are typical and tend to even out in the long run (Chart 1), keeping the focus firmly on the headline job creation figure.

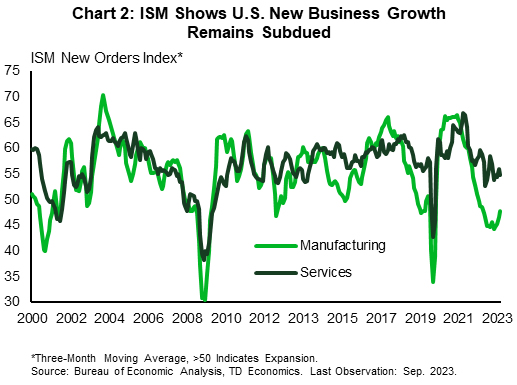

Private sector data that came earlier this week also supported the notion that the economy remains is fairly good shape despite the rate hikes. The ISM Manufacturing Purchasing Managers’ Index (PMI) firmed in the month, showing the contraction in the sector slowed. Meanwhile, its services sector counterpart held in expansionary territory despite slowing for the month. Rate hikes are clearly working as new business growth for both the manufacturing and services sectors (Chart 2) is moderating, but for all the work the Fed has done, it just isn’t proving to be enough.

Bottom line, a week of stronger-than-expected economic data have now all but put an end to the Fed’s pause. Financial conditions have tightened this week and will work to slow activity, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target. This means a hike by year end is now on the table as the Fed continues its work to restore balance and slow price growth.

Canada – Higher and Hire

This week was not exactly one of triumph for riskier assets. Oil prices tumbled, dragging the TSX down with them. For its part, the Canadian dollar also lost some ground, dropping half-a-cent to 73 cents US. The source of this angst? The relentless upward march in bond yields, as investors continue to recalibrate to a “higher-for-longer” backdrop. Notably, the Canadian 10-year yield hit a fresh, 16-year high this week. Ditto for the 5-year yield, and blowout jobs reports on Friday on both sides of the border simply added to this narrative.

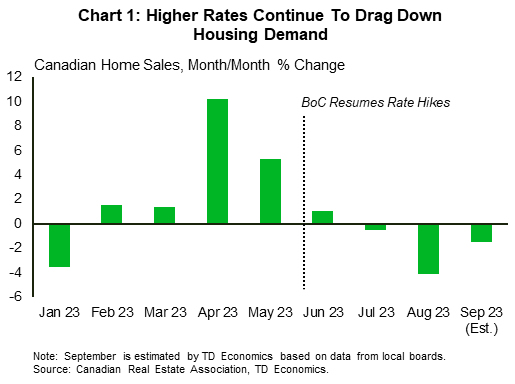

This elevated rate backdrop will make for a ghoulish October for housing. This week featured the release of local real estate board data capturing developments in September (Chart 1). Unsurprisingly, home sales declined in markets such as Toronto and Vancouver. Even the near-unflappable Calgary market finally stumbled, with sales down around 1% month-on-month. Valuations, meanwhile, appeared relatively resilient, with average prices flat in Toronto and benchmark prices down only slightly in Vancouver. These outcomes were consistent with what we had imbedded in our latest housing forecast. More surprising (and concerning) was the surge in new listings, particularly in Toronto. In the GTA, listings increased to levels typically only seen in periods of frenzied activity or extreme housing market weakness. Accordingly, the sales-to-new listings ratio (a measure of the supply-demand balance in housing) eased to its lowest level since the Financial Crisis – a surefire signal that prices are set to sag further in coming months.

Developments in housing always draw interest from Canadians, but undoubtedly the marquee report this week was the jobs data for September. The overall jobs gain shattered expectations, with 63k positions added last month. Still, not all aspects pointed in the same direction. For one, a large share of hiring came through the notoriously volatile self-employment sector, while private sector hiring was effectively flat. Accordingly, part-time employment surged, accompanied by a more pedestrian gain in full-time hiring. Hours worked also fell in September, which is typically a negative signal for monthly GDP. And, even with the powerful headline jobs tally, the unemployment rate was unchanged, thanks again to a surging population and robust labour force growth.

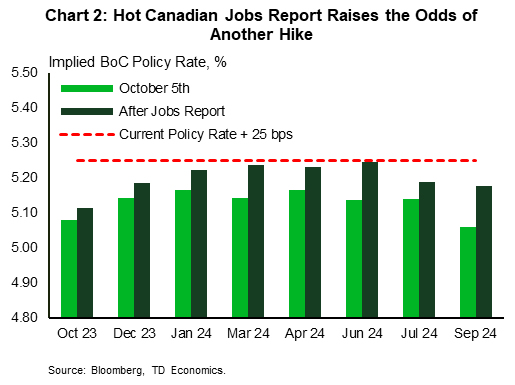

These wrinkles aside, the jobs report is certainly going to ruffle some feathers for central bank policymakers. Perhaps most notably, wage growth accelerated, and at 5% year-on-year, continues to run at a pace well above what’s needed bringing inflation back to the 2% target. This is especially true given the lackluster productivity that continues to plague the Canadian economy. In our view, the odds of another increase in the Bank’s policy rate just went up this morning. Markets had looked like they were on the fence as to whether the BoC would hike again, and this morning’s data was enough to shove them fully in that direction (Chart 2).

{kind=link}