- Policymakers argue surge in yields counts as hike

- US economy continues to fire on all cylinders

- Fed to stand pat, but may deliver a hawkish message

- Decision on Wednesday at 18:00 GMT; press conference at 18:30 GMT

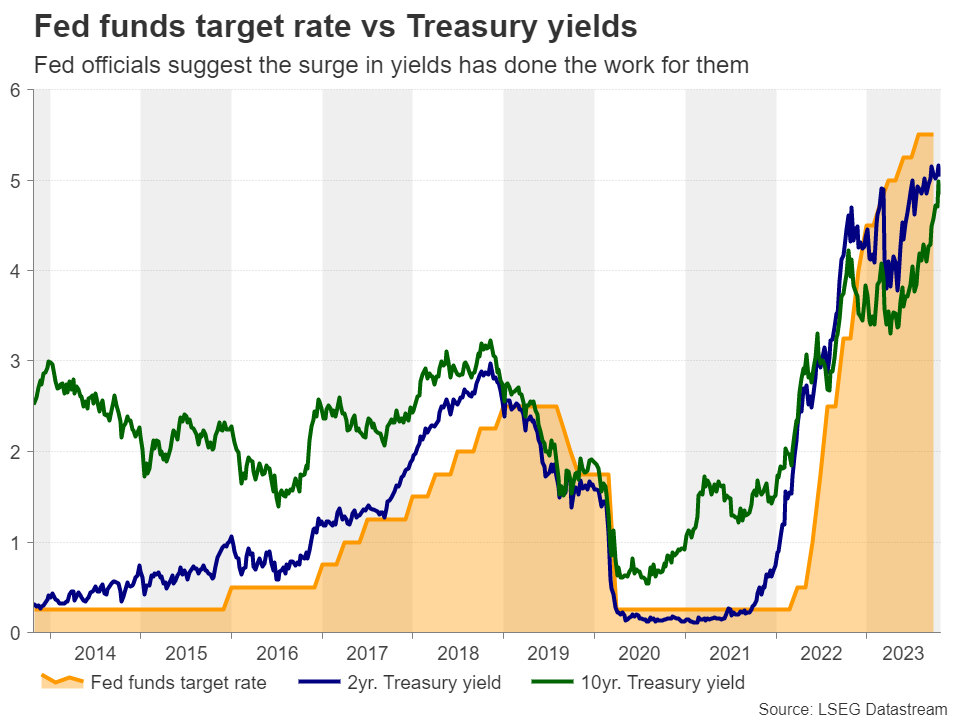

Yields do the work for the Fed

Although at their last gathering Fed policymakers maintained their projections of one more hike before the end credits of this tightening cycle roll, they have been appearing in dovish suits recently, signaling that the surge in Treasury yields since then has done the work for them, implying that another hike may eventually not be needed.

They stressed though that for inflation to return to their 2% objective, interest rates need to stay high for a prolonged period, with some of them leaving the door open to additional increases. Minneapolis Fed President Neel Kashkari, who has been an outspoken hawk during this hiking cycle, agreed with his colleagues but added that if long-term yields are higher due to expectations about what the Fed might do, then they may need to satisfy those expectations to maintain yields at those levels. More recently, Fed Chair Powell also acknowledged the role of rising yields, but still left additional action on the table.

Data points to a robust economy

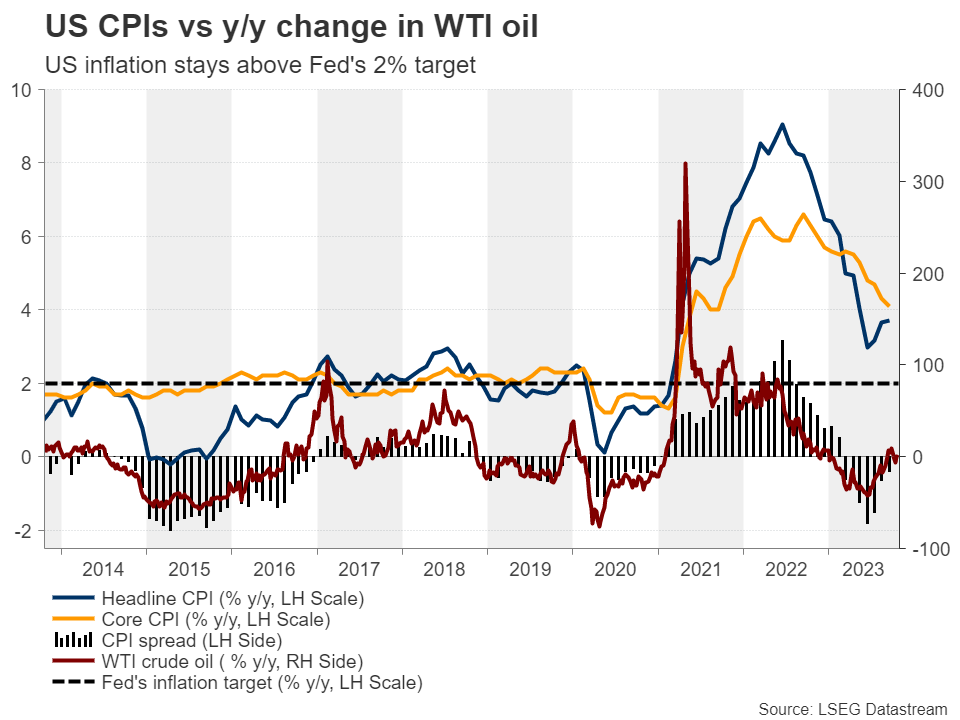

The dollar corrected lower on officials’ yields-related remarks, but with economic data continuing to point to a resilient economy, its losses remained limited and short lived. The latest CPI data showed that headline inflation held steady at 3.7% y/y in September, instead of slowing to 3.6% as expected, while the employment report for the month pointed to a still-tight labor market.

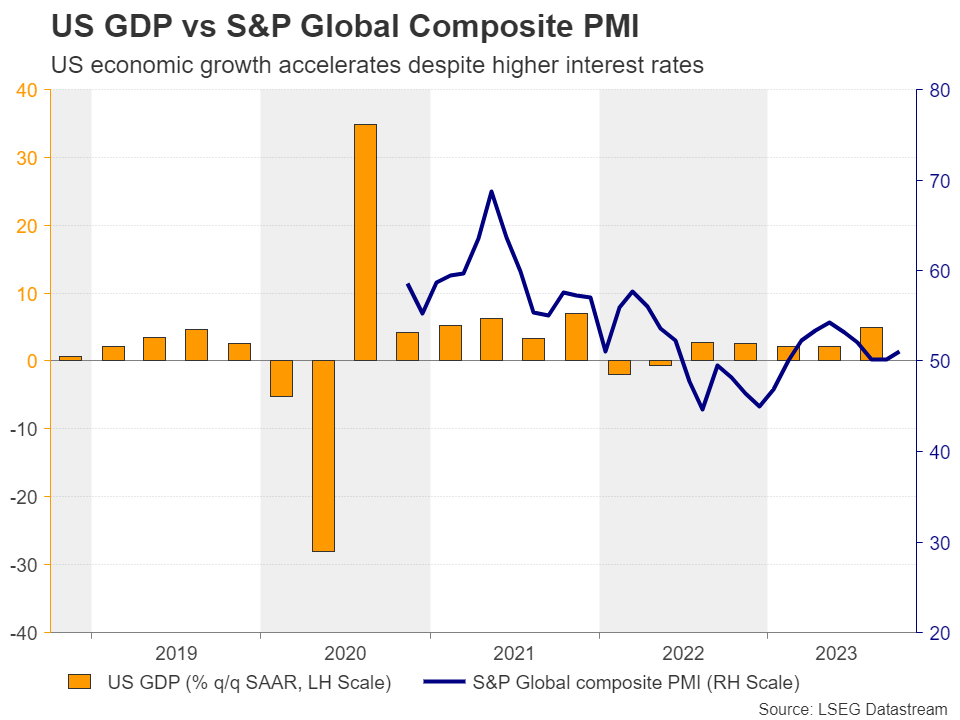

On top of that, Wednesday’s GDP data revealed that the US economy grew by an astounding 4.9% q/q SAAR in Q3, well exceeding the already encouraging forecast of 4.3%, while the preliminary PMIs for October suggested that the world’s largest economy fared better than expected during the first month of the fourth quarter.

Upside risks surround the gathering

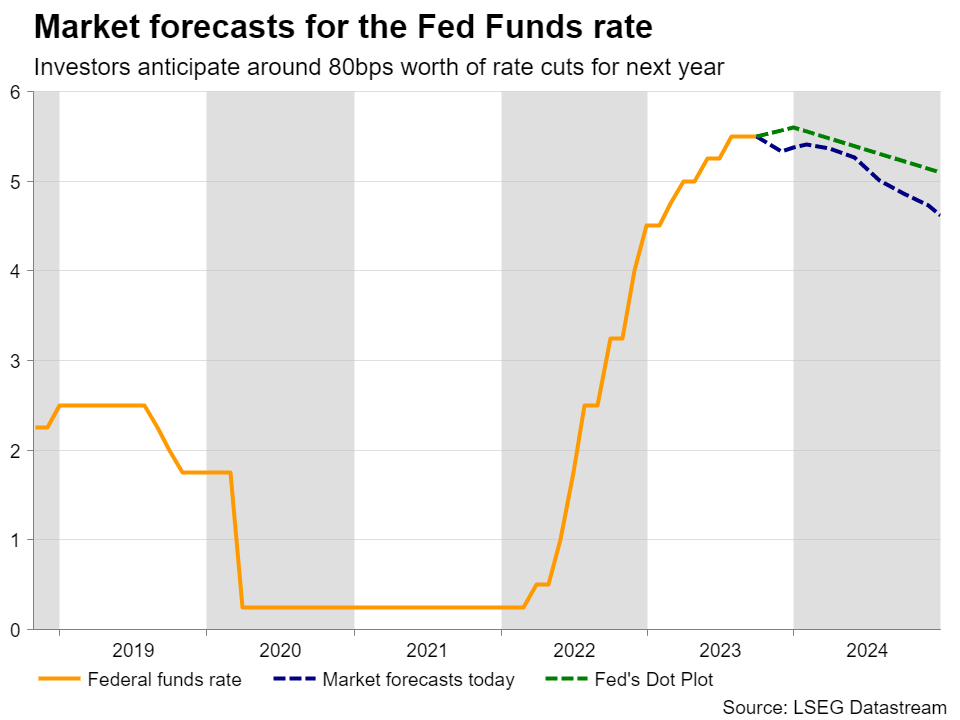

Yet, investors are skeptical on whether another hike may be warranted, perhaps as the rally in Treasury yields shows no signs of abating, despite a small rejection from the 5% zone on Monday. According to Fed funds futures, there is only a 30% probability for another 25bps hike by January and around 80bps worth of rate cuts expected by the end of next year.

Taking all that into account, Wednesday’s FOMC decision may attract special attention. Although virtually no one expects policymakers to act, the statement and the press conference may be scrutinized for clues and hints as to whether the door for more tightening remains open and whether the market is correct in penciling in so many basis points worth of rate cuts.

With the US economy still firing on all cylinders, the risks may be tilted towards a hawkish outcome. Even if officials do not hint at another rate increase, there are no economic signs justifying 80bps worth of cuts. Therefore, there is a decent chance for Powell and Co. to reiterate the view that interest rates may need to stay high for longer than the market is currently anticipating to safeguard inflation’s return to their objective.

Dollar set to continue drifting north

If this is the case, traders may be tempted to lift their implied rate path. They may not significantly add to the probability of another hike as a hawkish outcome will also drag Treasury yields higher, but they may scale back a decent amount of basis points worth of rate reductions for next year.

This could prove positive for the dollar. With the Euro area economy in a much worse shape than the US, and investors pricing in around 75bps worth of cuts by the ECB for next year, even after Thursday’s gathering, euro/dollar may be destined to extend its downtrend for a while longer.

Euro/dollar has been on a downward trajectory since July 18. Although it rebounded recently, just this week, it was rejected by the crossroads of the 50-day exponential moving average and the key resistance zone of 1.0665. A hawkish Fed could encourage the bears to reach and breach the low of October 3 at 1.0445. A break lower would confirm a lower low and perhaps aim for the low of November 30, 2022, at around 1.0290.

On the upside, a move back above 1.0665 would just turn the outlook neutral as it will only signal the pair’s return within the sideways range that contained most of the price action between January and September. For the picture to be considered positive, the bulls may need to drive the action all the way above the 1.1070 zone, which is the upper bound of the aforementioned range.

{kind=link}