- Japanese yen loses over 13% this year as interest rate differentials widen

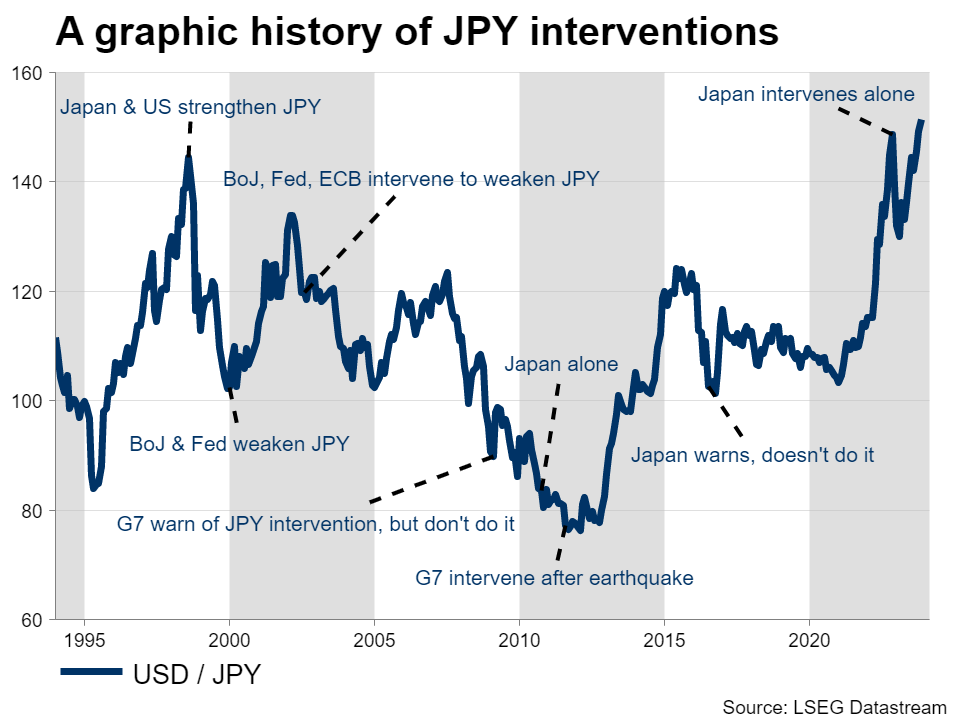

- Risk of another round of FX intervention is rising, but where exactly?

- Trend reversal is a story for next year – for now, outlook remains negative

Yen sinks despite favorable news

The Japanese yen remains the ‘sick man’ of the FX market. It almost touched a three-decade low against the US dollar this week, falling back to levels that prompted Tokyo to intervene in the FX market last year to defend the currency.

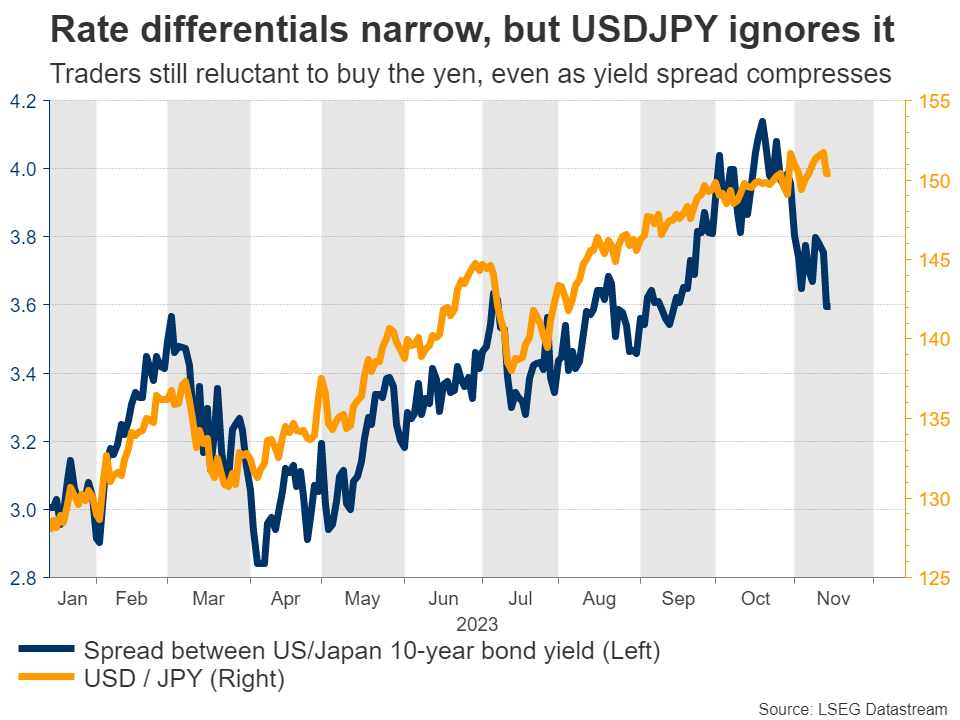

Interest rate differentials have been the driving force behind this relentless selling. The Bank of Japan has refused to raise rates, keeping them in negative territory even as foreign central banks like the Fed have raised their own rates to 5% or beyond. This enormous gap has seen capital leave Japan, searching for higher returns abroad.

High energy prices have also inflicted damage on the yen through the trade channel. Since Japan imports nearly all its oil and gas, the nation has been forced to pay more for its energy in recent years, which has deprived the yen from the trade surplus it has historically enjoyed.

The striking part is that both of these forces lost their punch this month, with US bond yields and oil prices declining sharply, and still the yen was unable to recover. Instead, these favorable developments were only enough to stabilize the wounded currency, which underscores that traders are extremely reluctant to buy the yen.

Will Tokyo intervene again?

Without a question, the risk of another round of FX intervention has risen. The currency is already trading around levels that triggered intervention last year, and Japanese authorities have warned that they won’t hesitate to take further action.

The final authority in intervention matters is the minister of finance – Shunichi Suzuki – who recently said the government will ‘take all possible steps necessary to respond to currency moves’. That said, it’s important to note that Suzuki did not use phrases that would suggest intervention is imminent.

In the past, the buzzwords that would signal Tokyo is about to intervene would be describing FX moves as “one-sided” or “disorderly”. The fact that the finance minister refrained from using such language implies we are still some distance from actual intervention.

So the question is, where exactly is the line in the sand for Tokyo? That’s tough to answer, because the speed of currency depreciation matters in this calculation. In general, authorities are more concerned about sharp and sudden moves, as those threaten the nation’s economic stability.

Looking at the USD/JPY chart, some strategists believe the catalyst for intervention would be a break above the 152.00 region. However, the lack of urgency in the finance minister’s tone suggests the real threshold might be higher than that.

In this sense, the next spot to watch would be 155.00. How concerned Japanese officials sound as the yen approaches this area would be an indication of whether intervention is coming.

Is a trend reversal a story for 2024?

For now, it’s difficult to be optimistic on the yen. If the sharp drop in US yields and oil prices was not enough to lift the currency, it’s difficult to see what will, especially while the Bank of Japan remains so hesitant to phase out its colossal stimulus program.

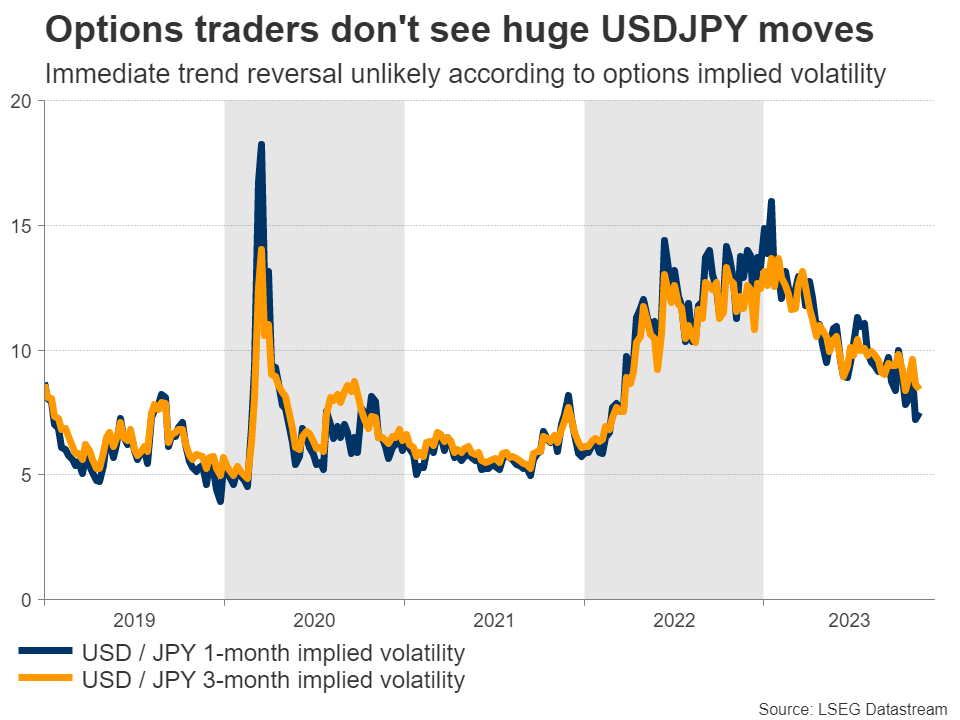

Options traders share this view. Implied volatility in short-dated USD/JPY options has fallen steadily in recent weeks, which means investors are not hedging against any massive yen moves in the next few months, viewing that scenario as unlikely. Hence, according to the options market, there’s no trend reversal on the immediate horizon.

But looking into next year, the outlook appears much brighter. With the global economy losing growth momentum and some regions teetering on the brink of recession, markets anticipate a rate-cutting cycle to begin around the spring. As such, the yen could get some relief from foreign interest rates falling next year.

The yen could also get a lift from the Bank of Japan tightening policy, perhaps by exiting negative interest rates. Markets are pricing in a minor rate increase for April, which coincides with the spring wage negotiations that will be crucial for the BoJ’s decision-making.

Similarly, there’s a chance the BoJ abandons yield curve control. This is the strategy that has crippled the yen, so scrapping it could help revitalize the currency. Whether that happens will depend on the wage negotiations and how the economic landscape evolves, but with the government preparing a heavy spending package to boost growth, the chances seem high.

All told, even though the near-term fortunes for the yen seem bleak, keeping the risk of intervention alive, the bigger picture looks more promising in an environment where interest rate differentials compress next year. The yen’s epic downtrend might be approaching its finale.

{kind=link}