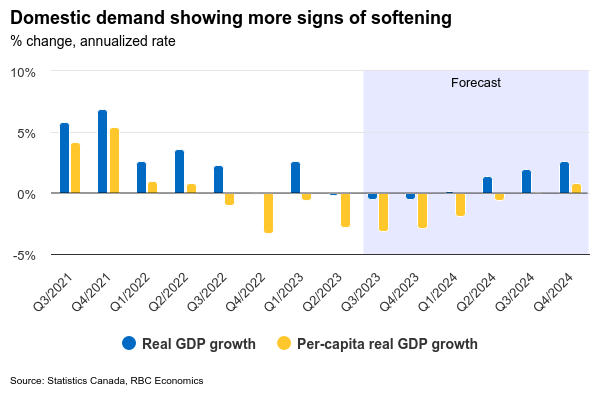

Canadian GDP likely edged lower in Q3 – we expect at a -0.5% (annualized) decline that would be slightly softer than the preliminary -0.1% estimate from Statistics Canada a month ago. Preliminary GDP estimates are highly revision prone, and domestic demand has shown more signs of softening in Q3 with both business and consumer spending slowing. And that small Q3 GDP decline will again look substantially weaker on a per-capita basis given rapid population growth. Canadian real retail sales were down 2.1% (on a quarter-over-quarter annualized basis) in Q3. Restaurant sales declined ~4.5% in Q3 controlling for price changes and our own tracking of service-sector spending softened. Manufacturing output is down 4% from Q2 over July and August, consistent with signs of cooling demand for physical merchandise globally as headwinds from higher interest rates build. Residential investment likely edged higher with higher housing starts offsetting a pullback in home resales. Net international trade will add to GDP growth but largely from lower imports tied to softening in domestic demand.

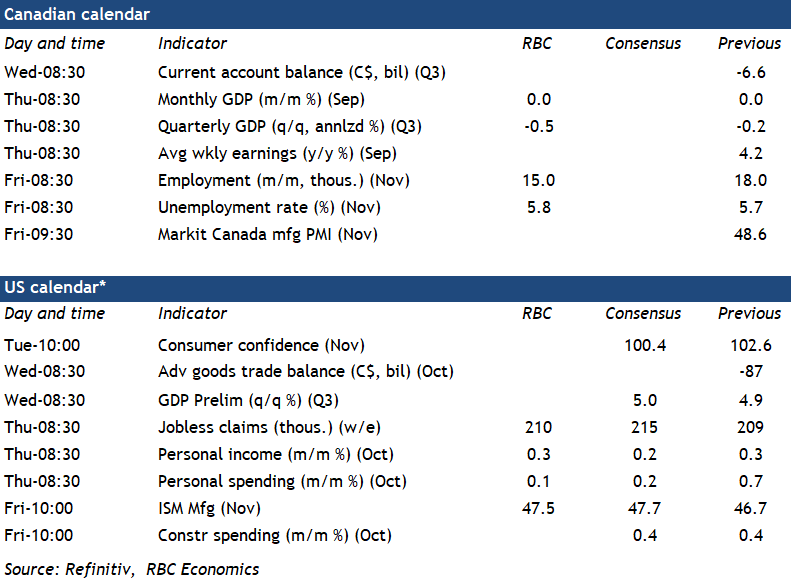

Early data for the fourth quarter does not look much better. The early estimate of October retail sales was stronger (+0.8%) but manufacturing sales fell 2.7%. Hours worked were unchanged in October alongside a small employment gain and another tick higher in the unemployment rate (to 5.7%).

And we expect November’s Canadian labour market data will underscore broader weakness in the economy. We look for a 15k job gain – not enough to prevent the unemployment rate from ticking higher by one-tenth to 5.8%. Soaring population growth has boosted the available labour supply, but as hiring demand slows, labour is being absorbed more slowly by the job market. Wage growth will be watched closely by the Bank of Canada, but softening labour demand is shifting bargaining power back to employers and we look for wage growth to broadly slow going forward.

Week ahead data watch

SEPH employment data for September will also be watched closely for further signs of softening in the labour market. Job openings (not counted in the more timely Labour Force Survey data) are expected to continue to drift lower as labour demand slows.

We expect U.S. personal income to tick up 0.3% in October, the same pace as in September. Employment growth and wage growth both slowed during that month. Real personal spending likely flattened in October from the 0.4% in September, largely due to weaker retail sales during that month.

decline that would be slightly softer than the preliminary -0.1% estimate from Statistics Canada a month ago. Preliminary GDP estimates are highly revision prone, and domestic demand has shown more signs of softening in Q3 with both business and consumer spending slowing. And that small Q3 GDP decline will again look substantially weaker on a per-capita basis given rapid population growth. Canadian real retail sales were down 2.1% (on a quarter-over-quarter annualized basis) in Q3. Restaurant sales declined ~4.5% in Q3 controlling for price changes and our own tracking of service-sector spending softened. Manufacturing output is down 4% from Q2 over July and August, consistent with signs of cooling demand for physical merchandise globally as headwinds from higher interest rates build. Residential investment likely edged higher with higher housing starts offsetting a pullback in home resales. Net international trade will add to GDP growth but largely from lower imports tied to softening in domestic demand.){kind=link}