- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 February, which is in line with consensus and current market pricing.

- Overall, we expect the MPC to deliver a dovish tilt to its guidance coupled with a downward revision to its inflation forecast.

- We expect EUR/GBP to move modestly higher upon announcement.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 February, which is in line with consensus and current market pricing. We expect the vote split to be 9-0, although we stress that risks are two sided for a three-way split. Note, this meeting will include updated projections and a press conference following the release of the statement.

Overall, we expect the MPC to deliver a dovish tilt to its guidance coupled with a downward revision to its inflation forecast and more explicitly to remove its tightening bias in the form of “further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.” However, we think the BoE will be cautious in being too optimistic on the inflation outlook to prevent premature easing of financial conditions.

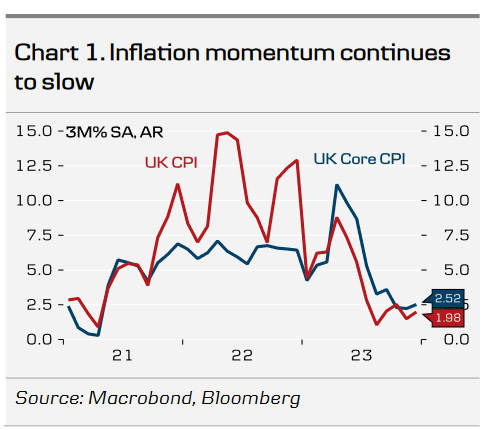

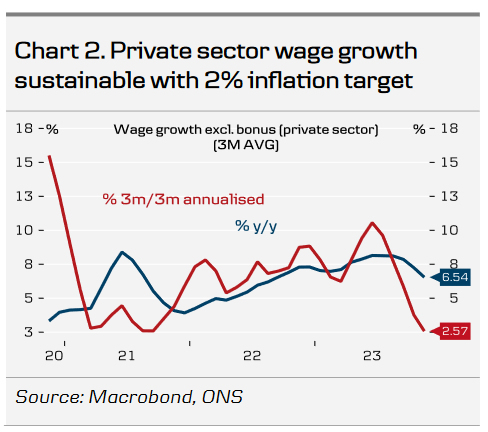

Since the last monetary policy decision in December, data releases have overall pointed to more muted price pressures. November delivered a sharp broad-based downside surprise and while December brought an uptick, primarily due to volatile components such as air fares, it highlights that the road back to 2% will be bumpy. Importantly, the Q4 2023 headline print now stands at 4.2% y/y, which is below the BoE’s forecast from the November MPR at 4.6% y/y. Large base effects from energy prices last spring are set to bring headline inflation back to 2% during the first half of the year. As previously flagged, we do not see inflation developing materially different in the UK compared to elsewhere. Wage growth continues to edge lower with the pace of wage growth in the private sector now sustainable with a 2% inflation target (assuming 1% productivity growth), see chart 2. The growth backdrop remains a challenge for the MPC, with both composite and service PMIs remaining in expansionary territory pointing to the UK avoiding a recession in 2024.

Fiscal policy remains a joker for the monetary policy outlook. The chancellor is expected to have a larger than expected headroom at around GBP 20bn in the Spring Budget presented on 6 March. Coupled with an upcoming general election, the budget will likely include tax cuts. However, we expect measures to be largely supply side driven, which would minimise the potential upward pressure on inflation.

BoE call. We expect the BoE to prime markets for an upcoming rate cut at the May meeting while delivering the first cut of 25bp in June and subsequently 25bp cuts in the following quarters, totalling 75bp of cuts for 2024. This is less than current market pricing of 100bp. Importantly, we do not see the BoE deviating from the Fed and ECB by the extent currently priced by markets and expect markets to scale back on expectations from the latter.

FX. In our base case we expect EUR/GBP to move higher on softer guidance and updated projections. Overall, we see relative rates as a negative for GBP and see the recent rebound as attractive levels to sell GBP. We continue to forecast EUR/GBP towards 0.89 and stay short GBP/USD.

to keep the Bank Rate unchanged at 5.25% on 1 February, which is in line with consensus and current market pricing. We expect the vote split to be 9-0, although we stress that risks are two sided for a three-way split. Note, this meeting will include updated projections and a press conference following the release of the statement.){kind=link}