ENERGY

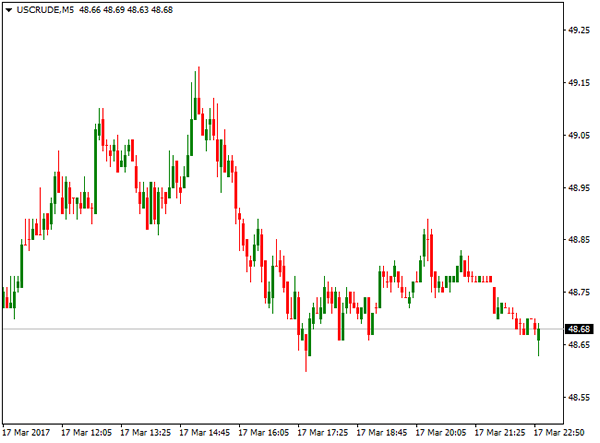

WTI Crude oil fell to multi-month low at $47.08 per barrel at the beginning of last week, extending previous week’s strong bearish acceleration on very strong rise of US oil inventories and oversupply concerns.

The price managed to recover losses on weaker dollar after Fed and fall in oil stocks this week that eased strong pressure on oil price.

US Crude stocks fell last week as imports plummeted, dropping after nine consecutive increases. Meantime gasoline and distillate inventories declined more than expected. The oil inventories have been closely watched by oil traders, who are looking to determine whether OPEC November’s agreement to cut output is reducing global supply excess.

Crude inventories fell by 237,000 barrels in last week, well below expected 3.7 million barrels build and previous week’s shocking 8.2 million barrels build that sent oil price to fresh three-month low.

However, oil price recovery is showing initial signs of stall, just under strong psychological / technical resistance at $50.00, which may further delay recovery. On the other side, oil price is attempting to hold above strong technical support at $48.70, which may trigger fresh upside attempts if remains intact.

All these factors will be closely watched next week, as oil price is showing no clear short-term direction, with focus implementation of OPEC production cut agreement and oil inventories.

However, technical studies remain weak and signal persisting downside risk while the price remains under $50.00 barrier.

COMMODITIES

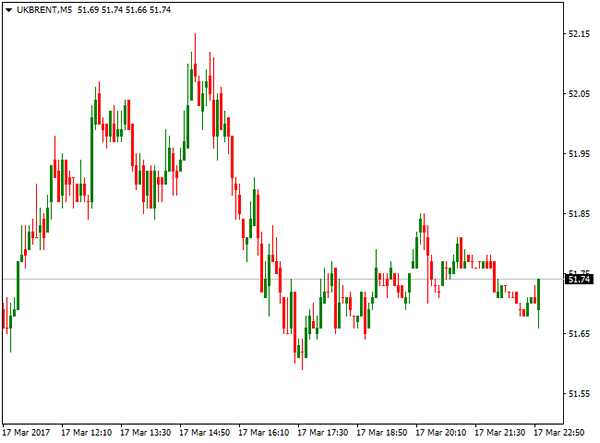

WTI Crude oil fell to multi-month low at $47.08 per barrel at the beginning of last week, extending previous week’s strong bearish acceleration on very strong rise of US oil inventories and oversupply concerns.

The price managed to recover losses on weaker dollar after Fed and fall in oil stocks this week that eased strong pressure on oil price.

US Crude stocks fell last week as imports plummeted, dropping after nine consecutive increases. Meantime gasoline and distillate inventories declined more than expected. The oil inventories have been closely watched by oil traders, who are looking to determine whether OPEC November’s agreement to cut output is reducing global supply excess.

Crude inventories fell by 237,000 barrels in last week, well below expected 3.7 million barrels build and previous week’s shocking 8.2 million barrels build that sent oil price to fresh three-month low.

However, oil price recovery is showing initial signs of stall, just under strong psychological / technical resistance at $50.00, which may further delay recovery. On the other side, oil price is attempting to hold above strong technical support at $48.70, which may trigger fresh upside attempts if remains intact.

All these factors will be closely watched next week, as oil price is showing no clear short-term direction, with focus implementation of OPEC production cut agreement and oil inventories.

However, technical studies remain weak and signal persisting downside risk while the price remains under $50.00 barrier.

INDICES

US Stocks added to gains after raised interest rates. Gains in Financial sectors after rate hike were offset by strong losses in health care sector, after President Trump’s budged plan proposed budget cut of $5.8 billion to the National Institutes of Health. This caused strong fall in Healthcare stocks.

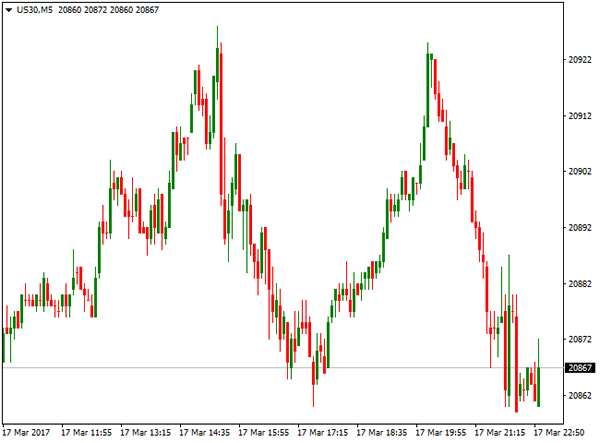

Dow Jones contract for June peaked at 21028 but failed to sustain gains and ended week in neutral mode at 20900 zone.

Nasdaq 100 contract for June posted new all-time high at 5439 on rally from weekly low at 5359.

S&P 500 contract for June ended week neutral after ranging between 2357 and 2391 during the week, but remains under fresh record high at 2400, posted on Mar 1.

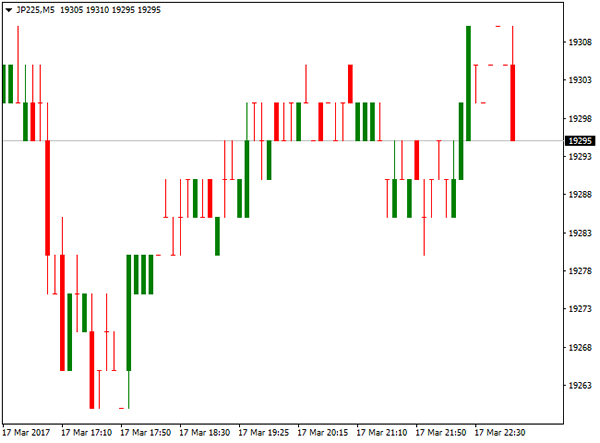

Japan’s benchmark Nikkei 225 ended week in red, after recovery attempts stalled at 19570, weekly high and index closed near weekly low at 19260. US Secretary of State Tillerson visited Japan and countries in the region, in attempts to find new approach to deal with threats from North Korea, that also influenced performance of Japan’s index.

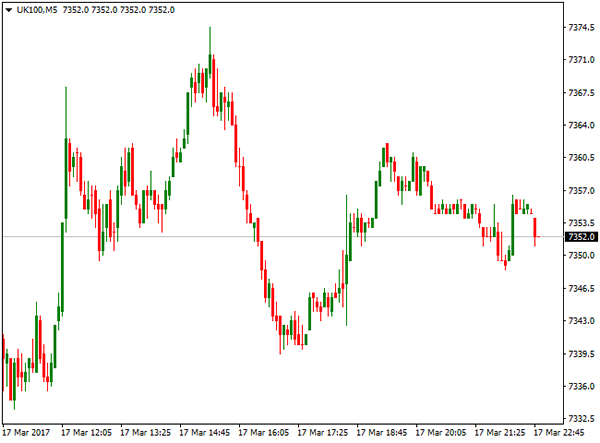

UK FTSE 100 index ended week positively but closed well below fresh all-time high at 7444, posted earlier this week. The index was up on renewed Brexit fears after UK PM May got approval from UK parliament to start process of negotiations between UK and the EU and received additional boost from initial decision of Bank of England to keep rates unchanged. However, vote of one of MPC members for rate hike, brought positive sentiment among traders and raised hopes that BoE may act earlier than expected and start tightening the policy. This accelerated the rally of British pound and pushed FTSE 100 away from new record high to end week at 7350 zone and leave Friday’s gap intact.

Another speculation of earlier than expected interest rate hike from ECB policymaker comments, lifted Eurozone on Friday, sending banking stocks higher. German DAX index peaked at 12177 on Thursday, the highest level since early Jan but was unable to hold gains and eased to 12100 zone, where it ended the week.

FOREX

Foreign exchange market was in focus last week, as four major central banks delivered their monetary policies: US Federal Reserve, Bank of England, Bank of Japan and Swiss National Bank.

All eyes were turned towards Fed, who hiked interest rates by 0.25%, as widely expected, but failed to show more aggressive approach regarding their future steps that defined closely watched FOMC’s Statement and press conference of Fed Chair Yellen, as dovish.

This was enough to send the US dollar lower across the board, on traders’ disappointment by Fed’s tone, expecting central bank to flag plans to accelerate the pace of monetary tightening.

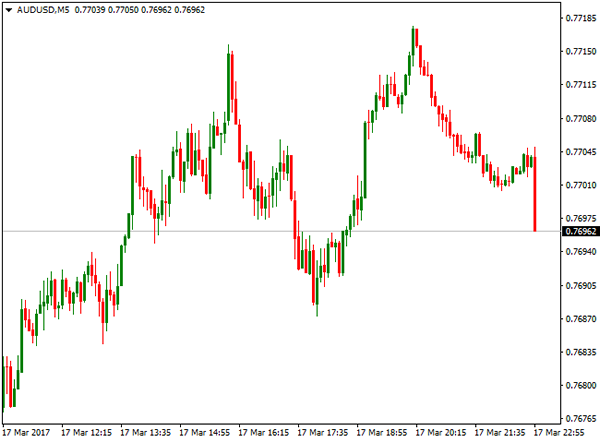

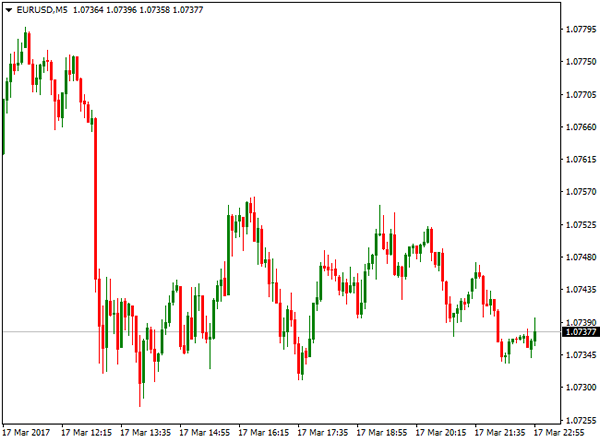

EURUSD surged to 1 ½ month highs at 1.0780 after Fed disappointed traders who jumped out of US dollar. The pair accelerated through strong technical barriers and managed to hold gains and end week positively, extending weekly gains into third consecutive week.

Gains were additionally supported by results of Dutch elections that soothed growing EU breakup fears and comments from ECB’s policymaker, who hinted ECB’s early rate hike, towards the end of the year.

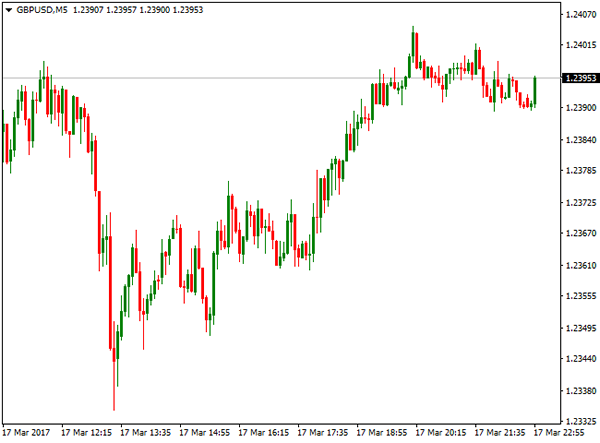

GBPUSD was hit at the beginning of the week and dipped to eight-week low against the dollar and basket of major currencies, by fears of a prolonged period of political jousting over the terms of Britain’s exit from the EU.

British PM Theresa May on Monday won the right to start Brexit process, beginning two-years of talks that will shape the future of Britain and Europe.

Sterling regained ground after Fed’s policy decision that send dollar sharply lower and provided relief to its counterparts, including the pound. Additional support for British currency came after Bank of England kept interest rates at 0.25% as expected, but out of nine MPC’s policymakers voted for rate hike, which markets understood as signal of early rate hike.

Pound extended rally and ended week at 1.2400 zone, levels last seen at the beginning of March and maintaining strong bullish tone.

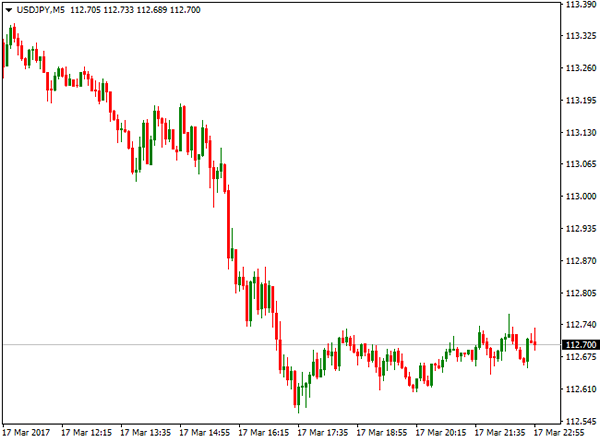

USDJPY fell sharply after dovish Fed, ending week in red on strong bearish acceleration from last week’s upside rejection at 115.50 zone. Technical studies signalled reversal on pattern that was formed, with acceleration through key technical supports, confirming growing bearish tone. The pair ended trading on Friday at 112.70, down from week’s high at 115.19, maintaining risk of further easing on fresh dollar-negative sentiment after Fed.

Meantime, Bank of Japan kept policy unchanged on Thursday’s meeting, with outcome of the meeting having little impact on pair’s performance. BoJ Governor Kuroda said that an uptick in inflation towards 1% would not immediately trigger an interest rate hike, signalling that the central bank will stick to its ultra-easy policy for some time.

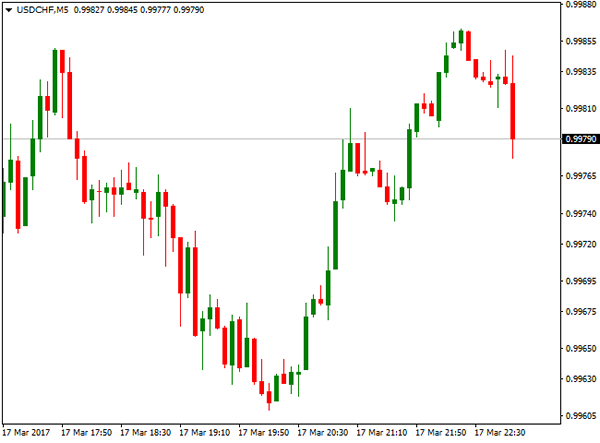

USDCHF ended week strongly in red and under the parity level, as demand for safe-haven Swiss franc grows on political uncertainty. Swiss National Bank stuck to its ultra-loose policy on last week’s monetary policy meeting, highlighting global political uncertainty on European elections this. Central Bank also said it is ready to intervene any time to protect their currency which is overvalued.