- Investors price in rate cuts despite BoE’s ‘higher for longer’ mantra

- Will the UK CPI and GDP data confirm that view?

- CPI inflation on Wednesday (07:00 GMT), GDP on Thursday (07:00 GMT)

Traders assign an 80% chance of a June BoE rate cut

When they last met, Bank of England (BoE) policymakers decided to keep interest rates unchanged at 5.25%. However, the decision was not unanimous. Two members voted for raising interest rates by another 25bps and one favored a same-sized rate cut.

Although officials removed from the statement the part saying that further tightening may be required if inflationary pressures persist, at the press conference following the decision, Governor Bailey pushed back against rate cut expectations, saying that they are not yet at a point where they can lower borrowing costs, adding that policy needs to stay sufficiently restrictive for sufficiently long.

That said, remarks by chief economist Huw Pill this week had a somewhat more dovish flavor, with the senior BoE official noting that key gauges of price pressures were not yet at a level that would permit easing policy, but also that there is no need for inflation to hit 2% before they begin to do so. “Lowering interest rates is a reward to the economy for better inflation performance,” he also said, allowing market participants to continue penciling in a high 80% chance for a first quarter-point reduction in June.

Inflation could further slow, recession may have been avoided

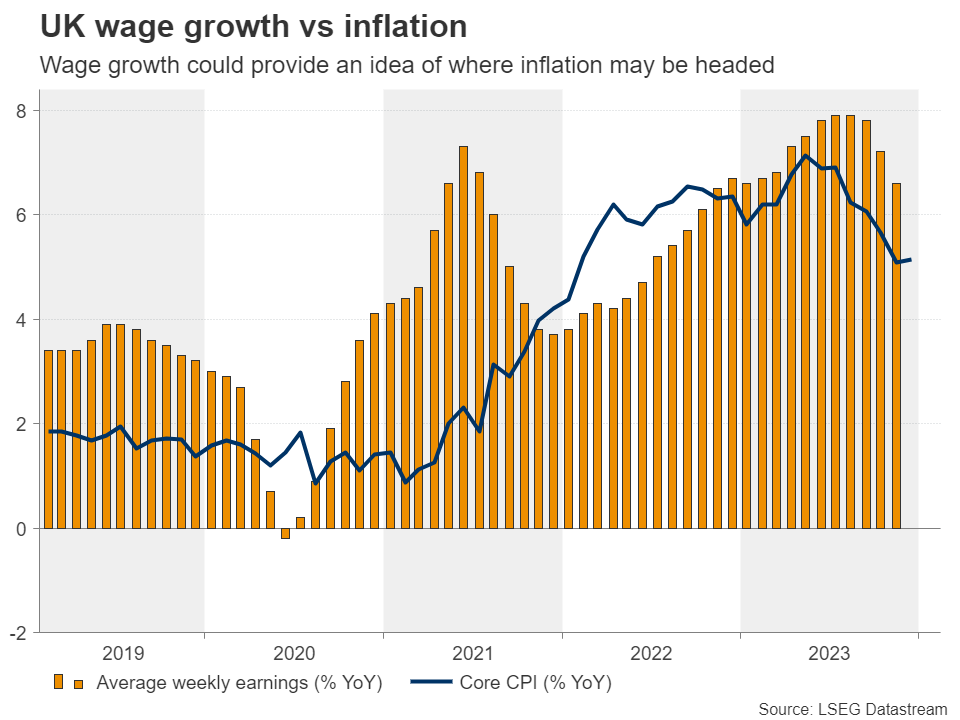

With all that in mind, pound traders will stay locked in front of their screens next week, as the calendar is packed with UK economic releases. On Tuesday, the jobs report for December is due to be released, with the focus likely to fall on average weekly earnings as investors try to figure out where inflation may be headed next.

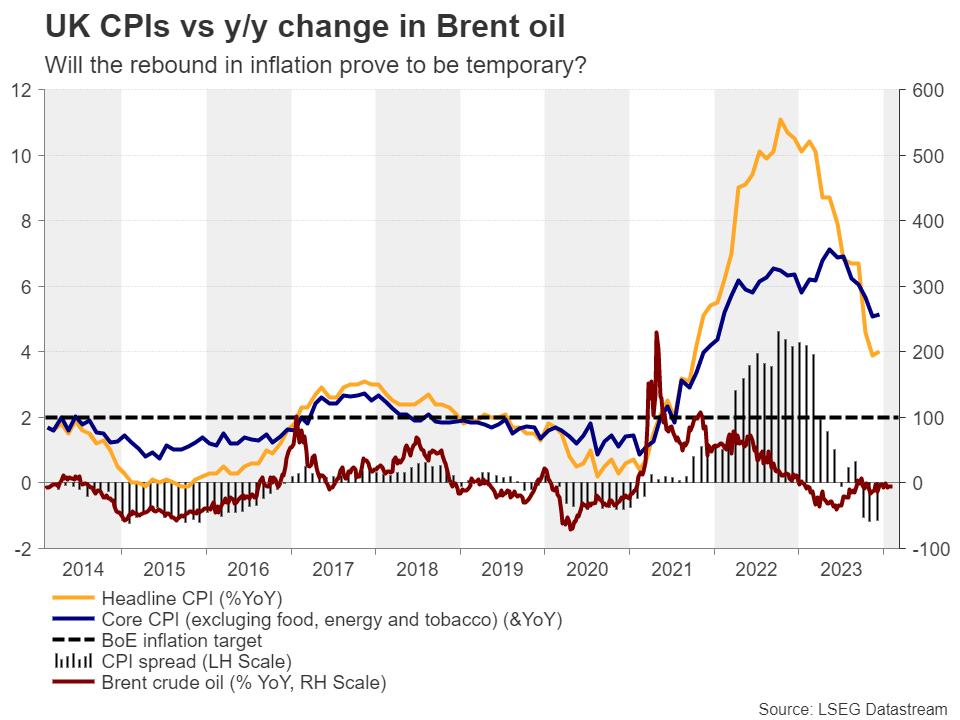

Yet, the centerpiece may be Wednesday’s CPI numbers for January. According to the UK PMIs for the month, although rising ocean freight rates resulted in cost burdens across the manufacturing sector and despite service providers signaling another steep rise in input prices, overall, prices charged by private sector firms increased at the weakest pace since last October. This likely shifts the risks surrounding the CPI numbers to the downside.

Though, with the y/y change in oil prices remaining close to zero, the gap between the headline and core inflation rates may continue to narrow, which means that the headline rate may not decline as much as the core one.

Be that as it may, slowing inflation may corroborate the market’s view that the BoE will start lowering borrowing costs in the summer, but the expectations about the pace of subsequent reductions may also depend on growth related data. On Thursday, the preliminary GDP data for Q4 and the month of December are due to be released, alongside the industrial and manufacturing production stats for the same month.

The downside revision of the Q3 GDP print revealed that the economy shrank 0.1%, and the 0.3% monthly contraction for October sparked recession fears, but those fears receded after the November monthly rate clocked at at 0.3%. Ergo, Thursday’s data may attract extra attention as it may confirm whether the UK economy has dodged a bullet.

According to the NIESR GDP estimate, the UK economy flatlined in the last three months of 2023, and should this be the case, the release may be cheered by pound traders. However, it is unlikely to tempt them to raise their BoE implied rate path. Any GDP related gains may remain limited and short-lived, especially if inflation further slows the day before. For the pound to end up gaining and sustaining those gains, an upside surprise may be needed. Retail sales are also due to be released on Friday.

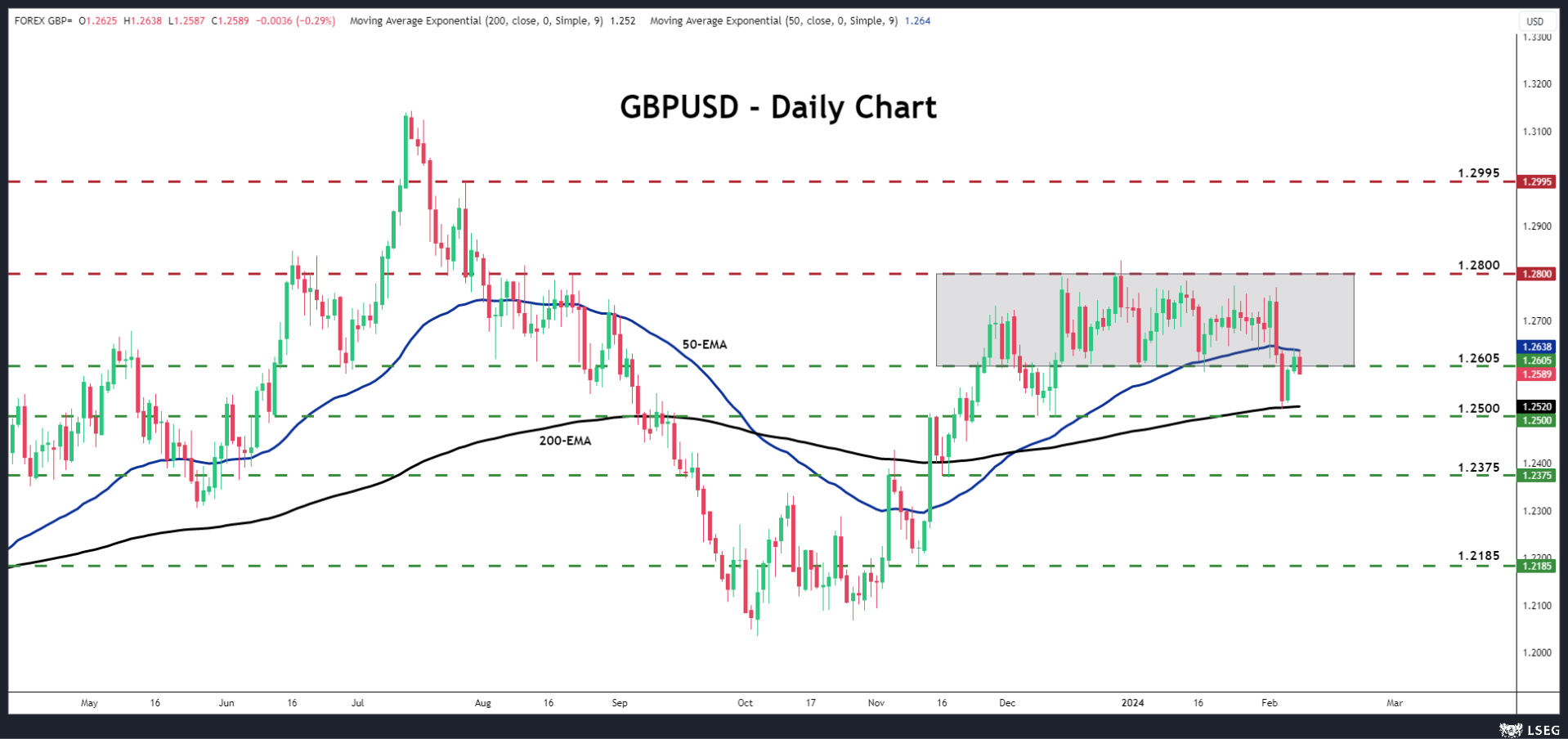

Pound/dollar could turn south again

From a technical standpoint, on February 5, pound/dollar fell below the lower end of the sideways range that was in place since December 14. However, just the following day, it rebounded after hitting support slightly above the 1.2500 zone and the 200-day exponential moving average (EMA). The recovery allowed the pair to test the 50-day EMA before turning south again.

A slowdown in UK inflation on Tuesday could result in more selling, with the bears aiming for another test near the psychological barrier of 1.2500. However, growth data confirming the no-recession case may be a reason for a pause around there. For the outlook to be considered bullish, the pair may need to climb all the way above the upper bound of the range at around 1.2800.

A slowdown in UK inflation on Tuesday could result in more selling, with the bears aiming for another test near the psychological barrier of 1.2500. However, growth data confirming the no-recession case may be a reason for a pause around there. For the outlook to be considered bullish, the pair may need to climb all the way above the upper bound of the range at around 1.2800.

policymakers decided to keep interest rates unchanged at 5.25%. However, the decision was not unanimous. Two members voted for raising interest rates by another 25bps and one favored a same-sized rate cut.){kind=link}