Staying the course

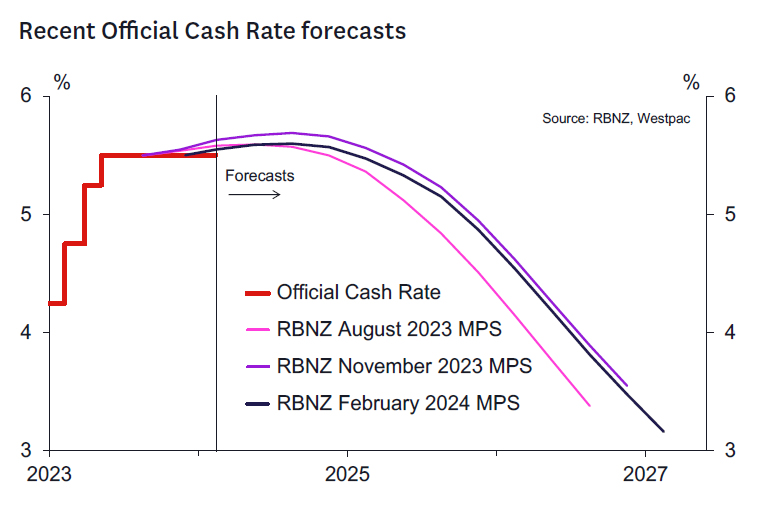

- The RBNZ left the OCR at 5.5%. The forward profile was lowered, and now implies around a 40% chance of a further OCR increase (down from 75% previously) and is in line with our own assessment.

- The record of the meeting noted that the risks to the outlook were viewed as “more balanced” than at the time of the November MPS.

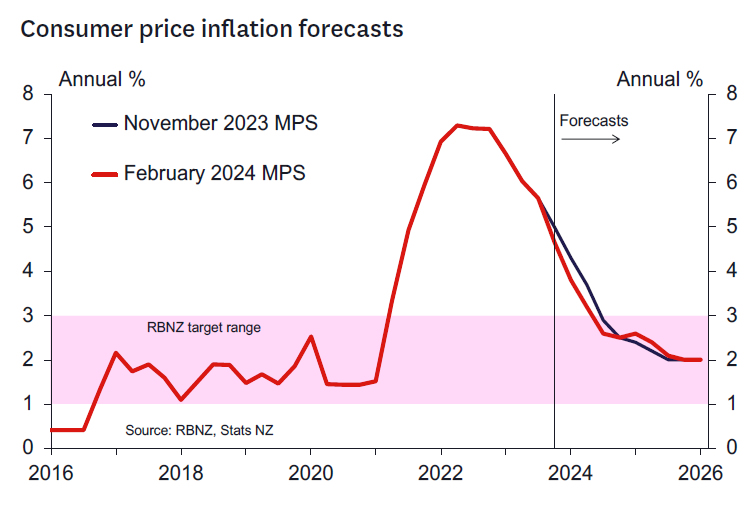

- The RBNZ’s inflation forecasts were revised lower over 2024, reflecting recent data.

- But the RBNZ’s 2025 forecasts were slightly revised up, reflecting persistent domestic inflation pressures.

- The RBNZ reaffirmed their commitment to seeing inflation at 2% in the second half of 2025.

- The RBNZ’s monetary policy strategy remains unchanged, implying the OCR will remain at 5.5% until 2025 – in line with Westpac’s forecasts. The RBNZ is staying the course.

The RBNZ left the OCR at 5.5% as we expected. The overall tone of the Statement remains somewhat hawkish – but much less hawkish than markets feared. The RBNZ still sees a risk of a need for a higher OCR to 5.75% in Q3 this year. However, these risks are lower than seen in November as the RBNZ’s updated OCR track was lowered and now implies around a 40% chance of a further OCR increase (down from around 75% previously). Indeed, the RBNZ’s forecast for the OCR over 2024 now looks much like that published in the August 2023 MPS.

A key excerpt from the MPS summarises the RBNZ’s view:

“Conditional on our central economic outlook, the Official Cash Rate (OCR) is expected to remain around current levels for an extended period in order for the MPC to meet its inflation target. The outlook for the OCR is slightly lower than in the November 2023 Statement. This reflects that the slightly lower outlooks for capacity pressures, import prices and house price inflation more than offset the higher outlook for export prices.”

The record of the meeting noted that members viewed that “overall, risks to the outlook for inflation were more balanced than at the time of the November 2023 Statement. However, from a monetary policy perspective, there remains less capacity to absorb upside inflation surprises, relative to downside surprises.” In the press conference, Governor Orr emphasised that while the risks to inflation are now more balanced, the policy reaction function to any realisation of these risks is asymmetric given the current level of inflation.

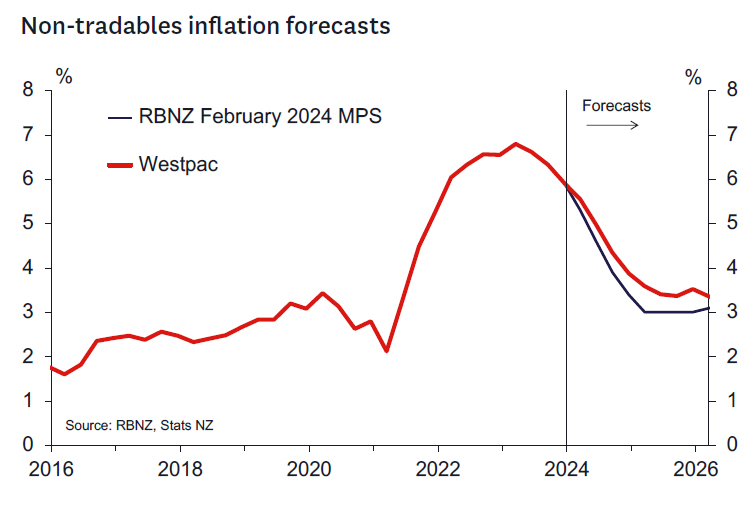

For now, the RBNZ seems comfortable that their monetary policy strategy of holding the OCR at 5.5% for as long as it takes will be sufficient to bring inflation back to 2%. Still sticky non-tradables inflation and a slowly adjusting labour market is keeping the RBNZ on their toes.

Governor Orr indicated that the MPC continues to maintain a “comfortable” consensus regarding the level of the OCR. While the possibility of a hike was discussed at the meeting, no vote was required.

As noted in our MPS preview and subsequent note, we didn’t expect an increase in the OCR, with a straight interpretation of the data suggesting that the track could even be lowered. But we saw material risks of either an OCR increase or upgraded risks of one in the future, if the RBNZ were to focus on some of the more worrying aspects of the data (e.g., the stickiness of non-tradable inflation). These risks were not realised.

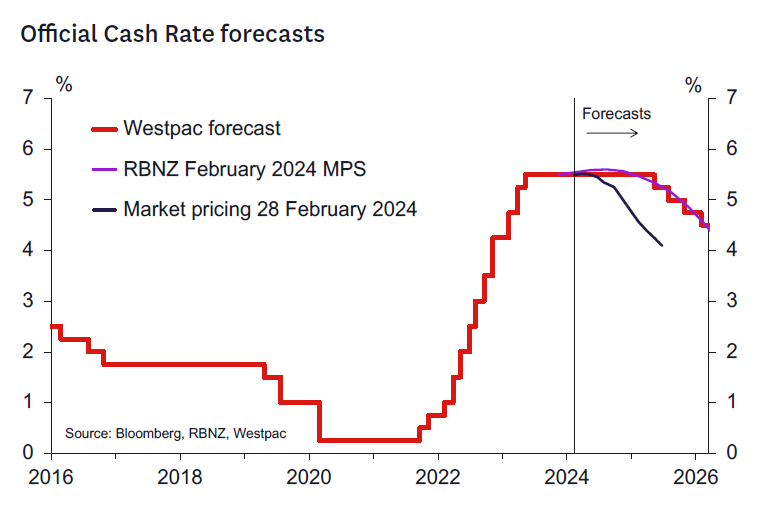

We remain comfortable with our view that the OCR remains on hold at 5.5% over 2024, before a gradual easing cycle begins in early 2025. We see a more gradual than expected easing in domestic inflation pressures than the RBNZ. Given today’s Statement noting “there was limited tolerance to increase the time to the target midpoint” this underpins our expectation that the RBNZ won’t be easing this year.

Key points to note from the Monetary Policy Statement.

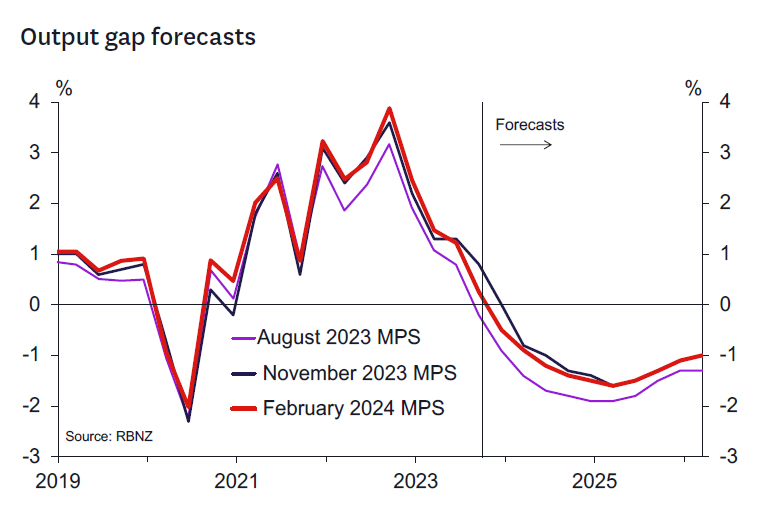

The RBNZ has responded to the weak Q3 GDP report and associated GDP revisions by lowering its estimate of trend growth but also lowering its estimate of the positive output gap in Q3 2023 to 0.3% from 0.8%.

In common with other central banks, notably the RBA, the RBNZ remains focused on downside risks to the Chinese economy, with potential impacts on both New Zealand’s export and import prices. The RBNZ also notes a general risk to global growth is that central banks may need to keep policy interest rates at restrictive levels for longer than currently reflected in financial market pricing.

Regarding fiscal policy, the RBNZ notes that the central projection in today’s MPS is based on the forecast for government spending in the HYEFU 2023. The RBNZ will take any new fiscal initiatives into account when Budget 2024 is released on 30 May. The Budget will be released after the May MPS meeting, but the RBNZ will have seen the underlying data before the MPS.

No change in the neutral OCR was made and the Chief Economist indicated that the RBNZ was comfortable with their 2.5% estimate “for this forecast”.

There is no adjustment in the horizon over which the RBNZ needs to see inflation return to 2%. This is still expected to be reached in H2 2025.

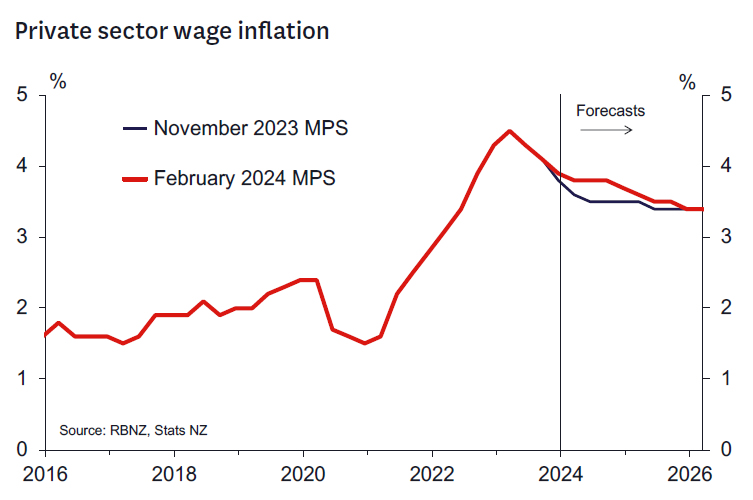

The RBNZ “marked to market” their unemployment rate forecasts and now see the unemployment rate rising more slowly to a similar level of 5.1% in mid- 2025. Their private sector wage forecasts were revised up, again reflecting the latest higher than expected outcome. The RBNZ seemed comfortable that this pace of adjustment was consistent with meeting their inflation objectives. Indeed, Governor Orr indicated that New Zealand seemed to be on track for a “soft landing” despite a material rise in unemployment.

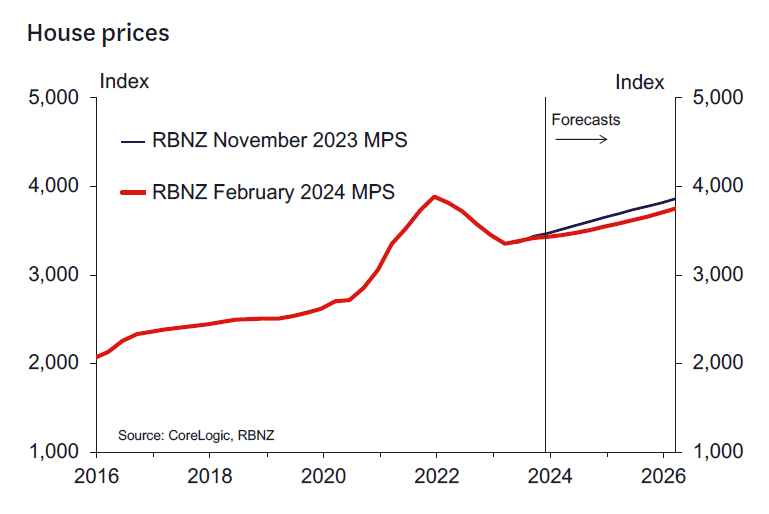

The RBNZ’s housing market forecasts were revised down reflecting recent flat data. This is in line with the RBNZ’s generally more relaxed tone regarding the impact of net migration pressures on inflation (although concern was raised on the level of rent inflation).

On inflation, we generally agree with the direction of changes to the RBNZ’s forecasts. They’ve accounted for recent weaker import prices and reduced their forecasts for tradables inflation. The RBNZ expects further sharp declines in tradables inflation consistent with the swings seen in the prices of volatile items like international airfares.

The outlook for non-tradables inflation remains elevated, reflecting ongoing strong wage growth and strong increases in the prices for services such as utilities and local council rates.

We think domestic inflation pressures will ease more gradually than the RBNZ is expecting, and we think that the challenge to their forecast could come in the March quarter inflation report (out 17 April). While the RBNZ expects domestic inflation pressures will be up 1.1% in the March quarter, we expect they will rise by 1.4%. That reflects factors such as the ongoing pressure on rents, and strong increases in costs such as insurance premiums and tobacco taxes.

Key things to watch over the weeks ahead.

Looking out over the next month or so, key economic data points to watch ahead of the next OCR review on 10 April will be:

- The Q4 GDP report (21 March). We presently estimate that the economy grew just 0.1% – not materially different to the flat outcome estimated by the RBNZ in today’s MPS.

- The selected price indexes released on 13 March, which will provide some further information about the outlook for the Q1 CPI report released on 17 April.

- Incoming migration and housing-related data, as well as indicators of consumer spending.

- Inflation indicators from the ANZ Business Outlook Survey (tomorrow and again on 27 March) and the NZIER’s QSBO survey (9 April) will also be scrutinised.

and is in line with our own assessment.){kind=link}