- Market scales back rate cut expectations

- Inflation is not cooling as fast as expected

- Powell testifies before Congress on Wednesday and Thursday

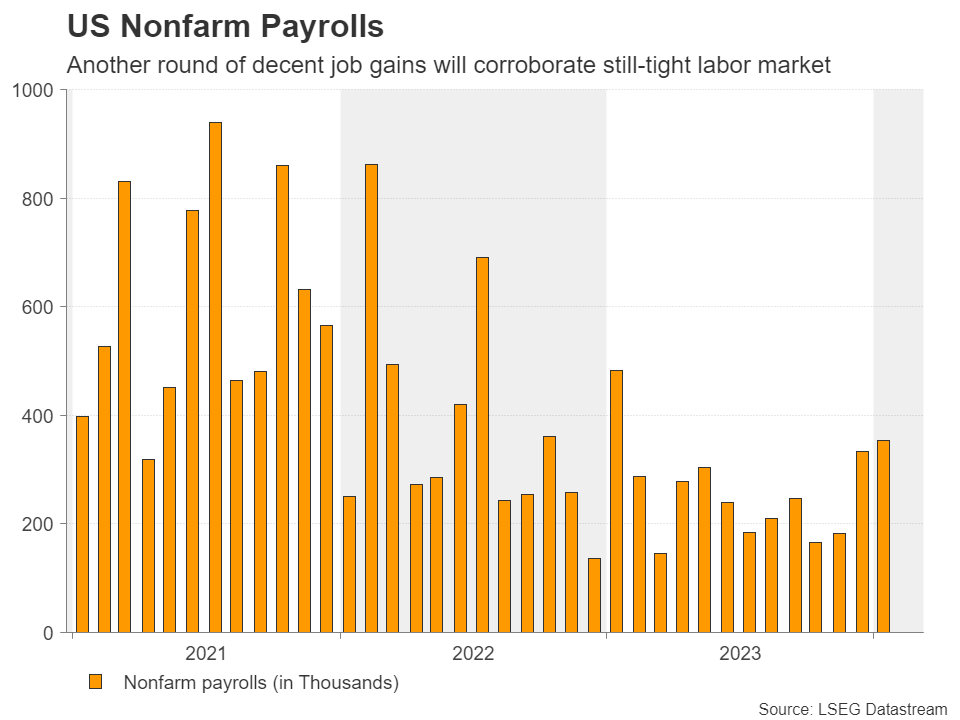

- Spotlight to turn to NFP report on Friday at 13:30 GMT

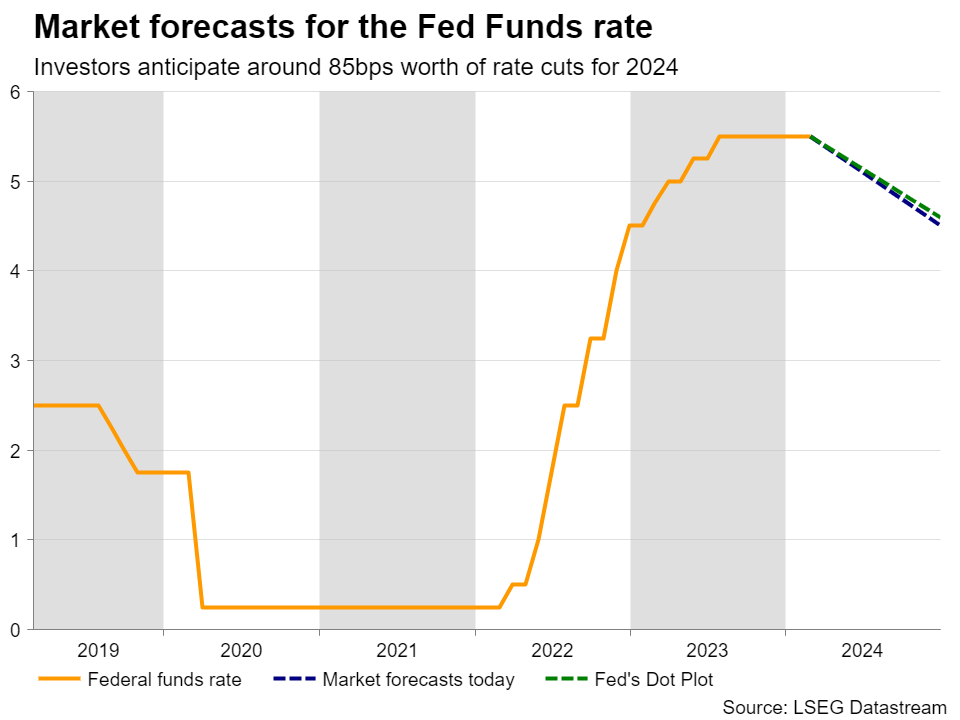

Investors get closer to the Fed’s dot plot

At its latest gathering, the FOMC appeared less dovish than expected. Policymakers decided to left interest rates untouched and dropped a longstanding reference to the possibility of further hikes. Nonetheless, they noted that it may not be appropriate to lower interest rates until they gain confidence that inflation is moving sustainably towards the 2% target. At the press conference, Fed Chair Powell was more specific, noting that a March rate cut was not the Fed’s “base case.”

Immediately after the decision, market participants pushed their bets of a first 25bps to May, while incoming data after the decision prompted them to scale back their expectations even further. Currently, the probability of a May reduction stands at around 25%, while a quarter-point cut is not fully priced in for June either. What’s more, the total number of basis points worth of rate cuts expected by the end of the year is at around 85, slightly more than the Fed’s own projection of 75. This suggests that there is still some room left for upside adjustment in the market’s implied interest rate path.

Powell testifies, NFPs the highlight

With that in mind, investors are now likely to turn their gaze to Powell’s testimony on monetary policy before Congress on Wednesday and Thursday, and Friday’s employment report for February.

With data since the latest Fed gathering pointing to stellar employment gains, a robust economic performance, and inflation not cooling as fast as anticipated, Powell is unlikely to deviate from the view that lowering interest rates is not an urgency.

As for Friday’s jobs data, the forecasts suggest that the unemployment rate held steady at 3.7%, while nonfarm payrolls are expected to have increased by 200k. According to the S&P Global composite PMI for the month, job creation was broad based, but the overall pace eased to the slowest in three months, corroborating the expectations of a slowdown in payrolls growth.

That said, after January’s stellar NFP print, another month of decent employment gains would confirm that the labor market remains tight and corroborate the view that the US economy is firing on all cylinders.

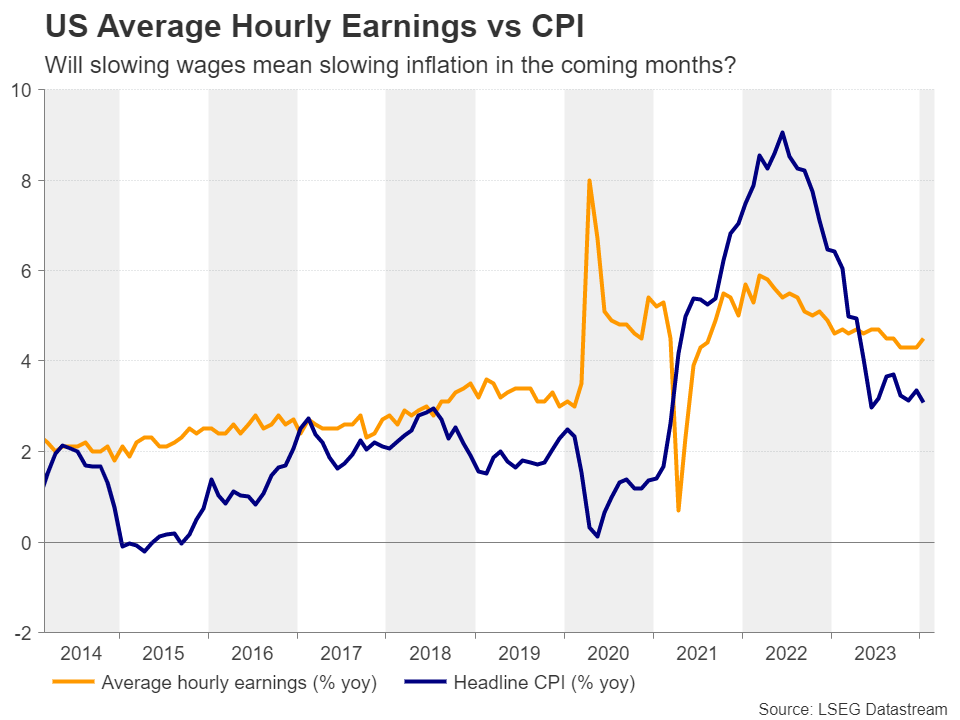

Wages also in focus amid stickier inflation

Investors may pay extra attention to the wage growth data too, as they try to estimate where inflation may be headed after the CPI and PPI data pointed to stickier than expected price pressures during January. Expectations are for average hourly earnings to have slowed to 0.2% m/m from 0.6%, with the y/y rate ticking down to 4.4% from 4.5%. This could imply that price pressures may continue easing in the months to come.

However, with the S&P Global PMIs suggesting that selling prices for goods and services accelerated somewhat in February, a minor slowdown in yearly earnings is unlikely to prompt market participants to bring forward their rate cut bets. They may even scale them further back if indeed the report points to decent job gains, conditional of course upon Powell sticking to his “higher for longer” view in the previous days.

A decent report could fuel the dollar’s engines

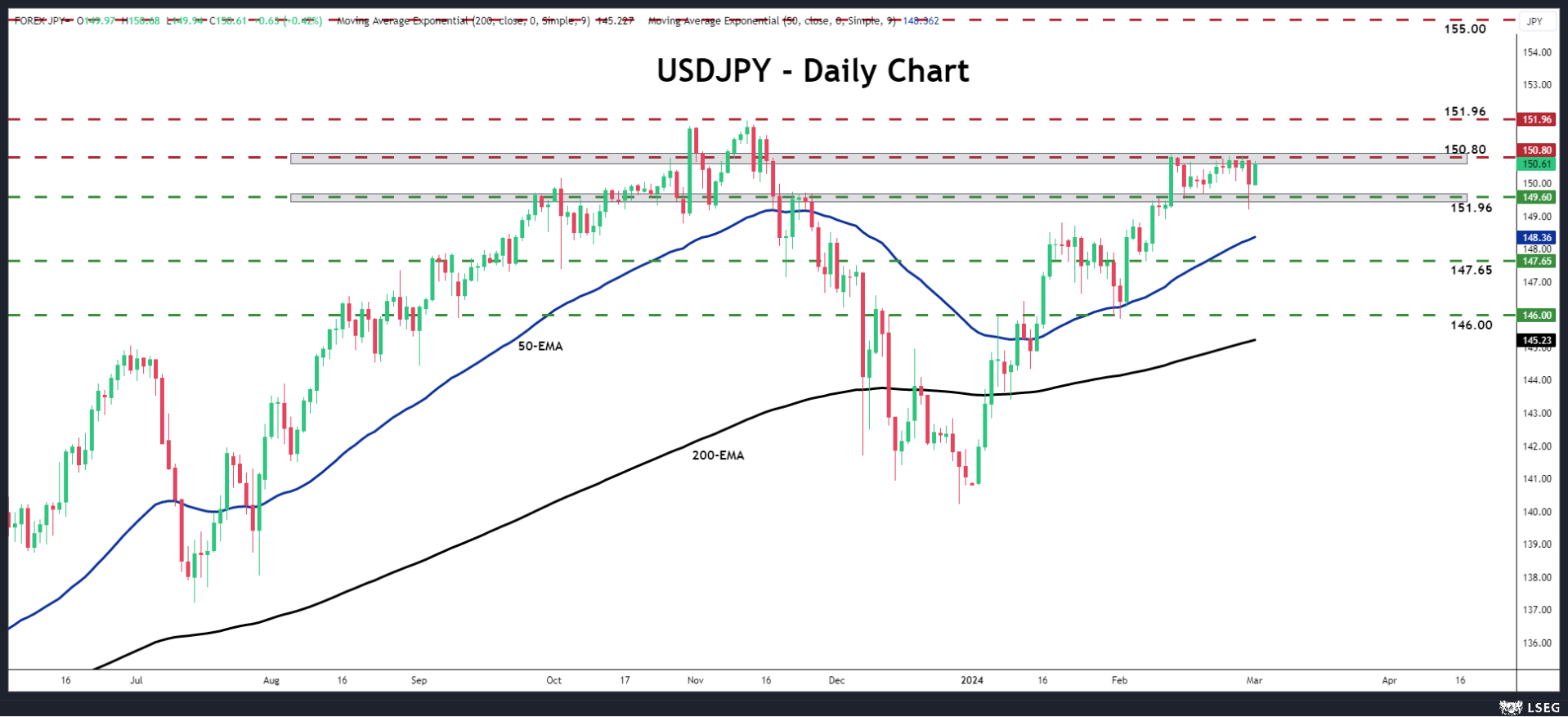

The US dollar could strengthen should this be the case, especially against the yen which resumed its fall after BoJ Governor Ueda contradicted Takata’s view that the 2% inflation goal is within sight, adding to speculation that even if a hike is delivered just after the spring wage negotiations, the pace of subsequent hikes in Japan will be very gradual.

Dollar/yen rebounded on Friday, after hitting support slightly below the key support zone of 149.60. That said, although the prevailing uptrend remains to the upside, the pair may need to break above the key resistance of 150.80 for a continuation to be confirmed.

Such a break could pave the way towards the 151.94 zone, hit back in October 2022 before the BoJ intervened to support the yen. The pair stopped slightly below that zone in November 2023 too. If buyers are willing to remain in the driver’s seat and decide to push the pair above that ceiling this time around, the pair may travel towards the psychological figure of 155.00.

However, it is worth mentioning that the higher the pair goes the higher the risk of another intervention episode by Japanese authorities. But for the broader outlook of this pair to change, declines all the way below the 146.00 zone may be needed. That zone acted as support on January 31 and February 1.

{kind=link}