Summary

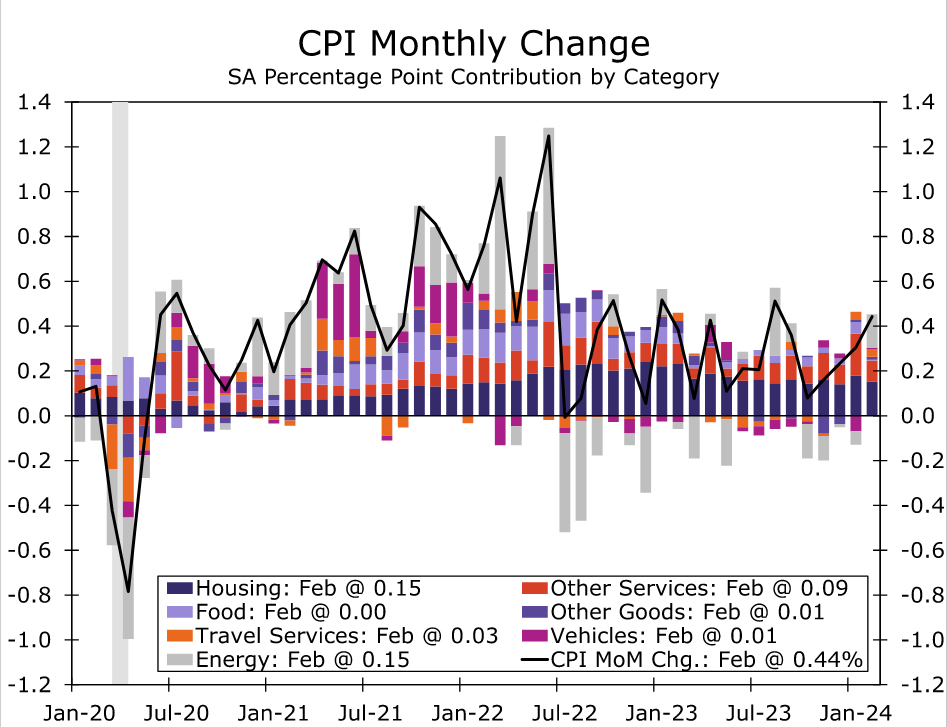

The February consumer price data came in a touch stronger than expected. The headline CPI increased 0.4% in the month, led by higher gasoline prices (+3.8%). Excluding food and energy prices, core inflation also registered 0.4%. However, the unrounded 0.36% bump in core CPI was not too far off our forecast for a 0.30% gain. Furthermore, core price growth was flattered by bigger than expected increases in volatile components such as used autos and airfares. Housing inflation cooled as owners’ equivalent rent increased 0.4%, a step down from the eye-catching 0.6% jump in January.

In our view, the details of today’s CPI report generally were encouraging. We expect core goods deflation to return in the coming months amid improved supply chains and less supportive seasonal factors. The much-anticipated slowdown in primary shelter inflation is ongoing. A cooling jobs market has brought about slower labor cost growth, and the widespread easing in this month’s “super core” suggests services inflation may not be as sticky as some feared following last month’s CPI report

That said, we doubt today’s report fills the FOMC with the confidence it needs to begin cutting rates. The core CPI has risen at 4.2% annualized rate over the past three months, which is a bit higher than the 3.8% increase in core prices over the past 12 months. We expect disinflation progress to resume in the coming months for the reasons listed above, but we think the FOMC will need to see it to believe it. The first rate cut from the FOMC looks increasingly likely to occur this summer. We will be publishing our FOMC preview report and Monthly Economic Outlook in the coming days, and we will update our fed funds rate outlook in those publications.

A Little More Inflation Than Expected

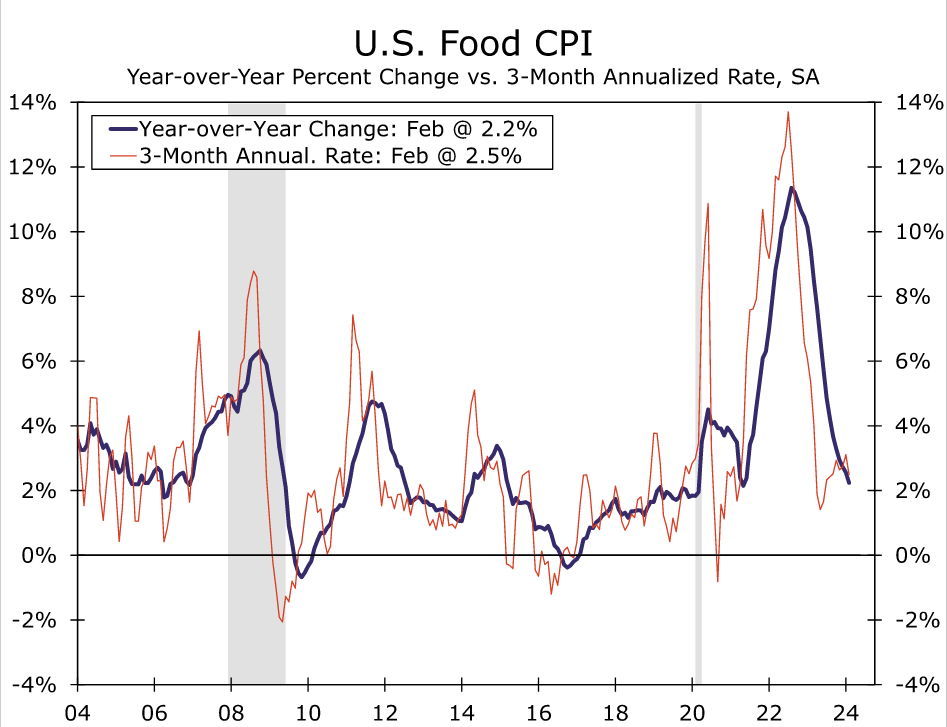

Consumer prices advanced 0.4% in February, in line with consensus expectations. The overall energy index, which accounts for a little under 7% of the CPI, increased 2.3% in February. As expected, the headline CPI was lifted by a jump in gasoline prices (+3.8%). Compared to one year ago, gasoline prices are still down 3.9%. Energy services rose a smaller 0.8%, led by utility gas service (+2.3%). Food inflation was more benign in February, with prices unchanged in the month. Grocery store prices were flat while prices at restaurants and bars increased 0.1%—the smallest monthly increase in three years. Over the past year, food inflation has cooled significantly and is now back in line with pre-pandemic norms (Figure 1).

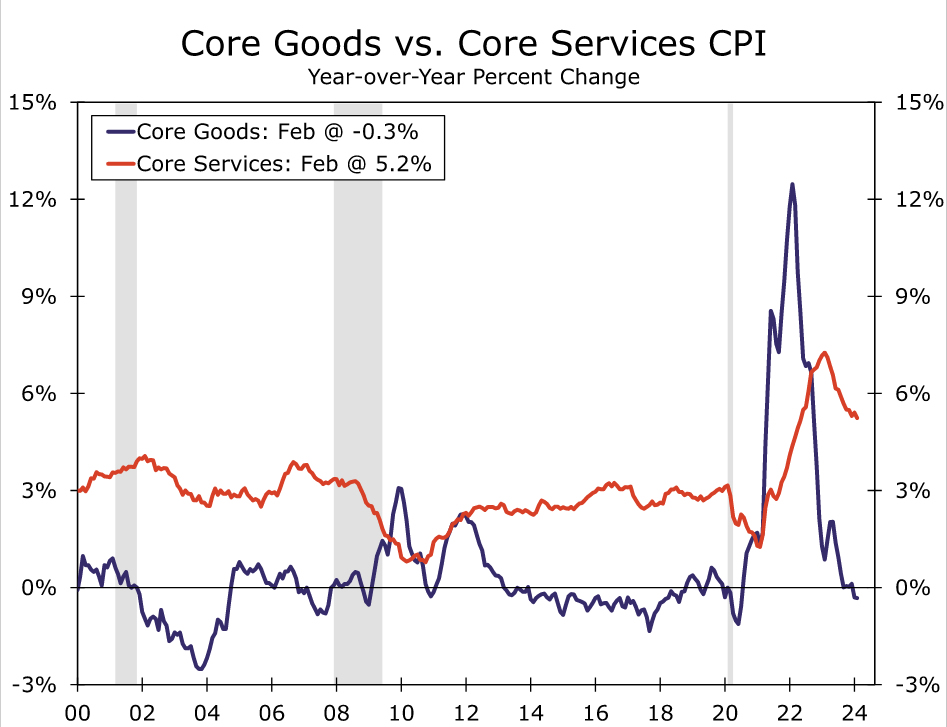

Excluding food and energy, the gain in CPI was a touch stronger than expected. The core index advanced 0.36%, a bit above the Bloomberg consensus and our own expectation for a 0.30% gain. The somewhat firmer reading stemmed from core goods, which rose for the first time in eight months (+0.1%). As we flagged in our CPI preview, however, core goods prices looked susceptible to being bolstered by some residual seasonality in February after price increases were more dispersed throughout the calendar year the past few years. Contributing to the rise was a small rebound in prices for used vehicles, apparel and education and communication goods, which offset declines in new vehicles, motor vehicle equipment, household and recreational goods. We expect to see core goods return to deflationary territory over the next few months amid the broad improvement in supply chains and less supportive seasonal factors.

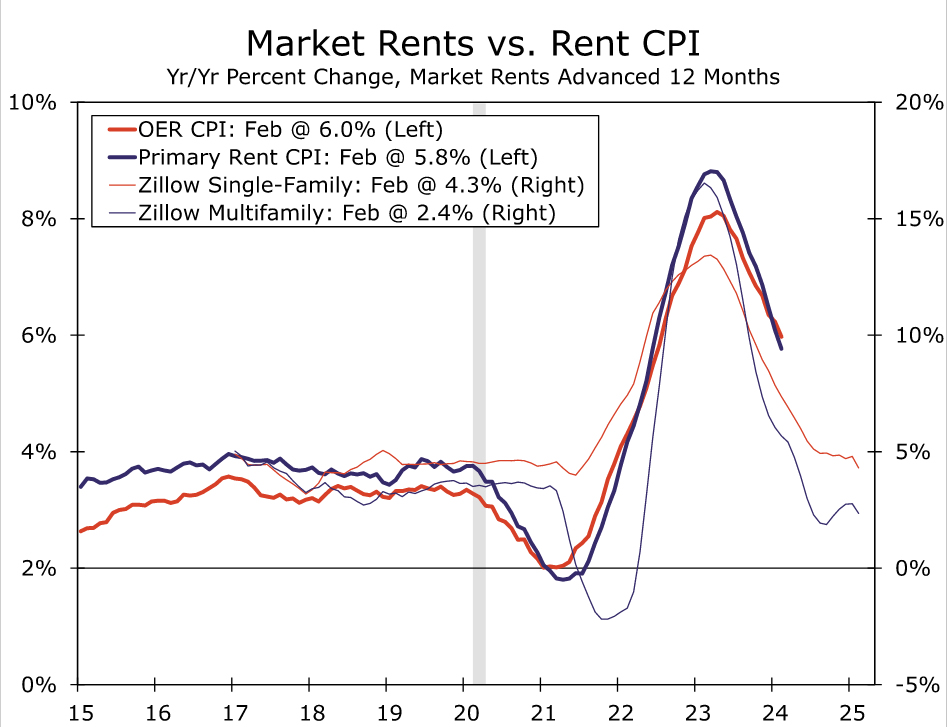

Core services, on the other hand, cooled largely as expected (Figure 3). A 0.7% jump in core services in January drove inflation’s unexpected pop to start the year. In February, core services prices advanced “just” 0.5% (0.46% before rounding). After making waves in January, owners’ equivalent rent growth eased in February (+0.4%). With rent of primary residences picking up in February (+0.5%), last month’s eye-catching gap between the two largest components of the CPI collapsed. Through the recent monthly volatility, the trend in housing inflation remains downward. Both the year-over-year rate of OER and rent of primary residences registered the smallest increases since the summer of 2022, and a further slide appears in store with private-sector measures of rent growth having largely returned to their pre-pandemic rates (Figure 2).

Excluding primary shelter, core services also advanced at a less concerning rate in February. The CPI version of the “super core”, watched by Fed officials to better gauge services inflation given the long lag in shelter inflation, advanced 0.4% after a 0.9% gain in January. The more moderate reading was helped along by a partial reversal of last month’s jump in medical and personal care services, as well as smaller monthly gains in lodging away from home, motor vehicle insurance and maintenance services. The broad cooling in the CPI “super core” in February suggests services inflation is not as sticky as initially feared following January’s sharp upside surprise.

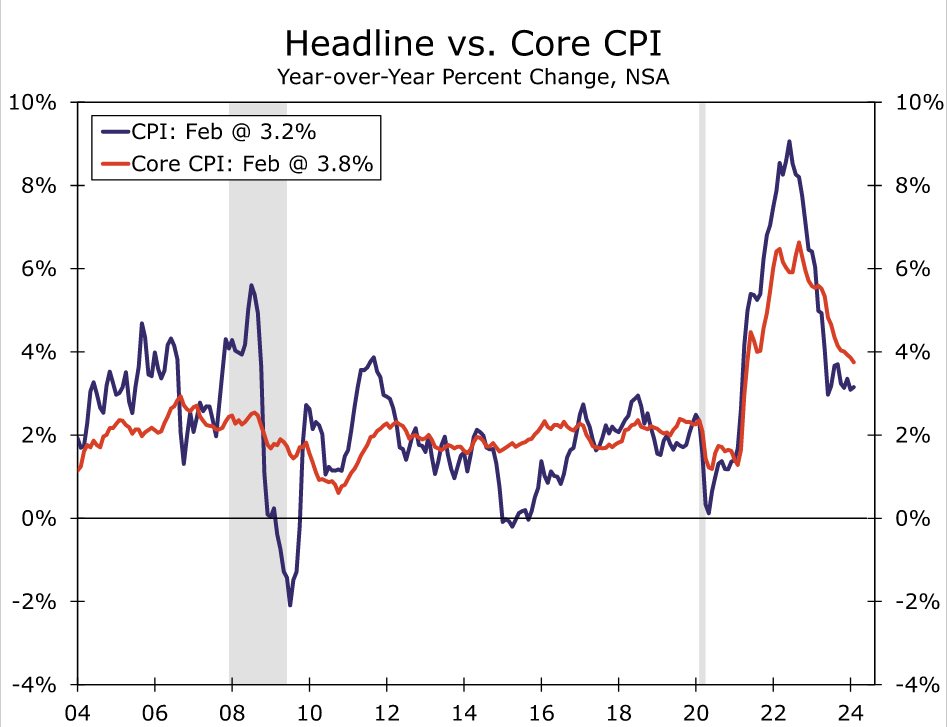

On a year-ago basis, consumer prices are up 3.2%, a more palatable increase than the 6.0% increase registered this time last year but little different from the past few months (Figure 4). The recent pace of core inflation, having registered a 4.2% annualized rate over the past three months, also points to some near-term stalling in inflation’s descent. However, we expect the lack of recent progress to be temporary. Price pressures across the economy continue to broadly abate. Labor costs are cooling as the jobs market softens. Consumers, while still spending, are not the price-takers they were a year or two ago as revenge spending dissipates and delinquencies creep higher. The supply chain kinks that helped drive core goods inflation to 47-year high largely have unwound, making it easier for businesses to secure product. In a separate report this morning, the February NFIB Small Business Optimism Index showed the smallest share of businesses raising prices in three years.

While a downward trend in inflation remains in place in our view, the slow progress seen over the past few months is likely to keep the Fed searching for a bit more confidence that inflation is on a sustained path back to its 2% target. The first rate cut from the FOMC looks increasingly likely to occur this summer. We will be publishing our FOMC preview report and Monthly Economic Outlook in the coming days, and we will update our fed funds rate outlook in those publications.

. Excluding food and energy prices, core inflation also registered 0.4%. However, the unrounded 0.36% bump in core CPI was not too far off our forecast for a 0.30% gain. Furthermore, core price growth was flattered by bigger than expected increases in volatile components such as used autos and airfares. Housing inflation cooled as owners' equivalent rent increased 0.4%, a step down from the eye-catching 0.6% jump in January.){kind=link}