Government rebates continue to hold down inflation while personal services inflation did pick up.

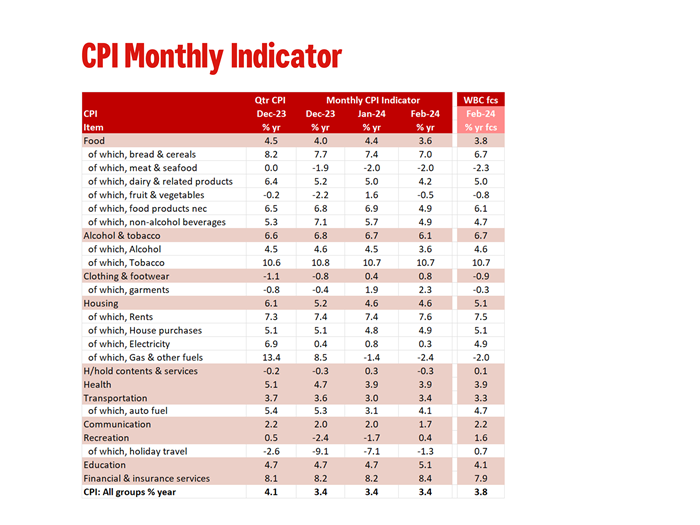

The Monthly CPI Indicator gained 3.4% in the year to February compared to 3.4%yr in both January and December.

The February print was a softer than Westpac’s forecast of 3.8% and the market median forecast of 3.5%yr. Taken at face value, the February Monthly CPI Indicator suggests that if there are any risks to our current March quarter CPI forecast of 0.7%qtr, it is to the downside. However, the quarterly CPI is not a simple average of the Monthly CPI Indicator and history has taught us that a simple ‘face value’ estimate can be misleading.

Highlighting this are the core measures. The Trimmed Mean measure lifted to 3.9%yr from 3.8%yr while the services series jumped to 4.2%yr from 3.7%yr while goods prices continue to moderate down to 2.9%yr from 3.1%yr. All groups excluding volatile items and holiday travel did ease back from 4.0%yr to 3.9%yr, but this is still much higher than the headline pace of 3.4%yr.

As noted in our preview, the mid-month of each quarter provides us with an important update on household services and so February sets the tone for much of this group for the quarter. Overall, quarterly surveyed services came in stronger than expected exemplified by the 5.1%yr increase in education (forecast was 4.1%yr). This presents an upside risk to our current quarterly CPI forecast.

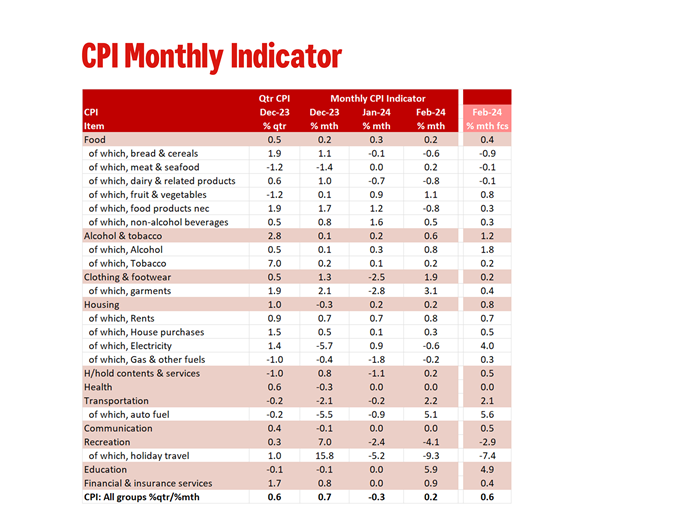

In the month of February, the Monthly CPI Indicator rose 0.2% compared to our forecast for 0.6% increase. The most significant difference to our forecast was electricity, and while this series is a monthly estimate, we have now seen a run of softer than expected electricity prices due to the ongoing impact of government rebates. February included a second round of energy rebates in Victoria. This does have a meaningful impact on our quarterly electricity forecast and presents a downside risk to our Q1 CPI forecast.

Weaker than expected electricity and holiday travel (both monthly series) are being offset by the stronger than expected services (which are quarterly surveys so now locked in for Q1). While we have more work to do on our quarterly forecast, at this stage we find the risk to our Q1 estimate of 0.7% is balanced.

In more detail the difference to our monthly forecast was:

- Food was a touch softer at 0.2% compared to 0.4% forecast.

- Alcohol & tobacco was on the softer side, 0.6% vs. 1.2% forecast, due to a lower-than-expected alcohol price increase.

- Clothing & footwear was stronger at 1.9% vs. 0.2% forecast due to strong price gains for both male and female garments.

- Housing was where the largest discrepancy was, 0.2% vs. 0.8% forecast, due to rebates suppressing electricity prices. In the month the second round of Victoria rebates saw electricity prices fall –0.6% vs. +4.0% forecast. Rents were close to expectations (0.8% vs. 0.7% forecast) while dwellings came in softer lifting just 0.3% vs. 0.5% forecast. It is somewhat surprising we are still yet to see a meaningful lift in dwelling price inflation. Also of note, gas & other household fuels fell –0.2%

- Household contents & services were also on the softer side rising just 0.2% vs 0.5% forecast. However, while monthly non-durables were down –0.5% in the month, domestic & household services (which are surveyed quarterly and so are locked in for Q2) rose 0.9%.

- Recreation was also softer side (–4.1% vs. –2.9% forecast) driven by a 9.3% fall in holiday travel (which is a monthly series).

- An important household service is education, and it is survey only once a year in February. It lifted 5.9% vs 4.9% forecast and as noted earlier, this estimate is locked in for the quarterly estimate.

- Insurance also reported a solid rise of 3.7% which is locked in for Q2. This follows a solid 3.8% gain in the December quarter 2023.

{kind=link}