Summary

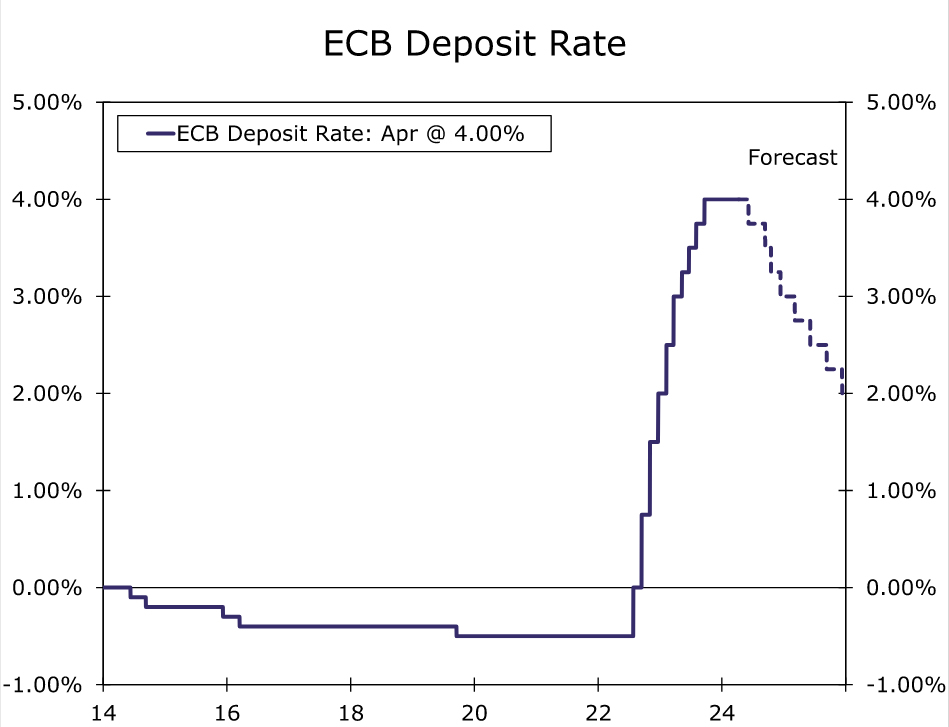

The European Central Bank held monetary policy steady at today’s announcement, though we view the accompanying statement as laying the groundwork for a probable ECB rate cut in June. The ECB cited an easing in underlying inflation and moderating wage growth. In addition, the ECB’s announcement and ECB President Lagarde suggested that so long as updated forecasts confirmed the improving inflation outlook, monetary policy easing would be appropriate at the June 6 meeting.

That said, we believe the ECB will pursue a measured pace of rate cuts during the second half of this year. That reflects some lingering inflation concerns, particularly as it relates to services inflation, and the likelihood of gradual Eurozone economic recovery as this year progresses. We forecast an initial 25 bps ECB policy rate cut in June, but then expect the central bank to forgo monetary policy easing in July. Instead, we expect the ECB to deliver 25 bps rate cuts in September, October and December for a cumulative 100 bps of easing this year. That is a slower pace of rate cuts than our previous forecast, though still more than the cumulative 76 bps of rate cuts currently priced in by market participants for the remainder of this year.

European Central Bank Holds Steady For Now, But Hints at Easing Soon

The European Central Bank (ECB) held its policy rate steady at today’s monetary policy announcement, though we view the accompanying statement as laying the groundwork for a probable ECB rate cut in June. There were, in our view, several elements of the central bank’s assessment of the economy that were dovish in nature. The ECB said:

- most measures of underlying inflation are easing

- wage growth is gradually moderating

- firms are absorbing part of the rise in labor costs in their profits

The ECB did, however, also say that domestic price pressures are strong and are keeping services inflation high. The ECB added that interest rates are at levels that are making a substantial contribution to the ongoing disinflation process (we think the use of the present tense, and dropping the reference to rates remaining at current levels for a sufficiently long duration, are both notable). And for the first time in its formal policy announcement, the ECB signaled the potential for monetary policy easing, even if that was in a contingent manner. The ECB said:

“If the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.”

The likelihood of a June rate cut was also reflected in ECB President Lagarde’s post meeting press conference. Lagarde said the ECB will get a lot more information by June, including a newly updated economic outlook. Lagarde also said a large majority of policymakers wanted to wait for the June announcement, although a few policymakers felt confident enough on inflation to move today. In effect, we view the ECB’s policy announcement as laying the groundwork for a likely rate cut in June. So long as the ECB’s updated economic forecasts confirm the improving inflation outlook, we expect the central bank to lower its Deposit Rate by 25 bps to 3.75% at its June 6 monetary policy meeting.

Expect A Measured Pace Of ECB Rate Cuts

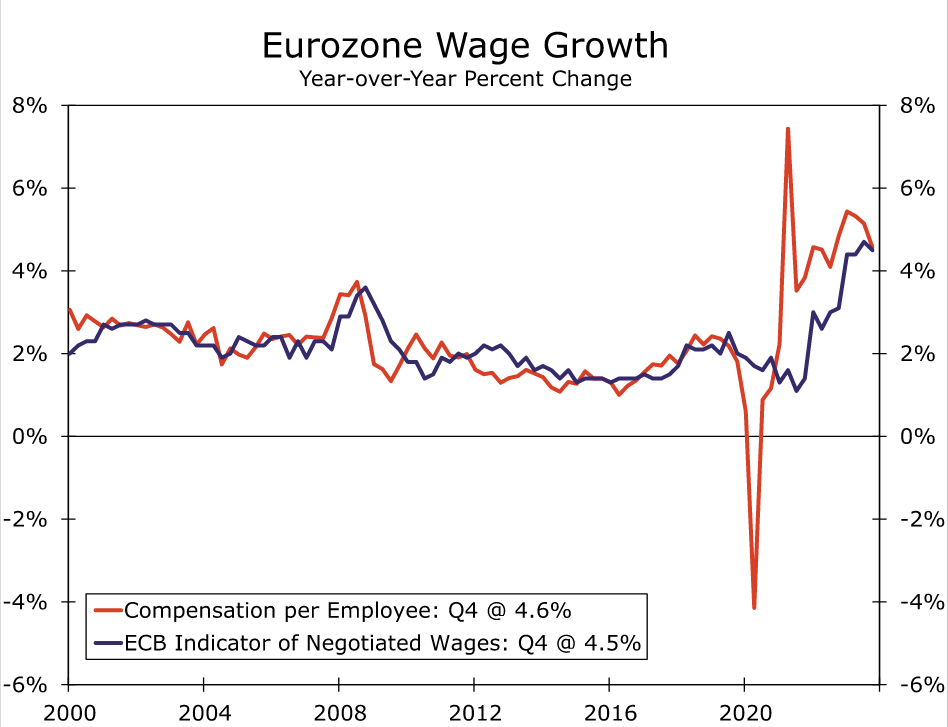

While the ECB hinted at a June rate cut at today’s announcement, we believe it will pursue a measured pace of rate cuts during the second half of this year. In part, our view reflects some residual caution surrounding wage developments in 2024, along with some stickiness in services inflation in particular. To be sure, the comprehensive wage measures available for the Eurozone began to show more encouraging trends late last year. The ECB’s Indicator of Negotiated Wages eased to 4.5% year-over-year, an outcome that was confirmed by Q4 compensation per employee, which also slowed to 4.6%. Eurozone hourly labor costs, admittedly a more volatile series, also slowed sharply in Q4 to 3.4% year-over-year, with the wages & salaries component up just 3.1%. We expect ECB policymakers will want to see details of early 2024 wage outcomes, along with evidence of more sustained wage deceleration, before contemplating a steady ‘every-meeting’ cadence for policy rate cuts.

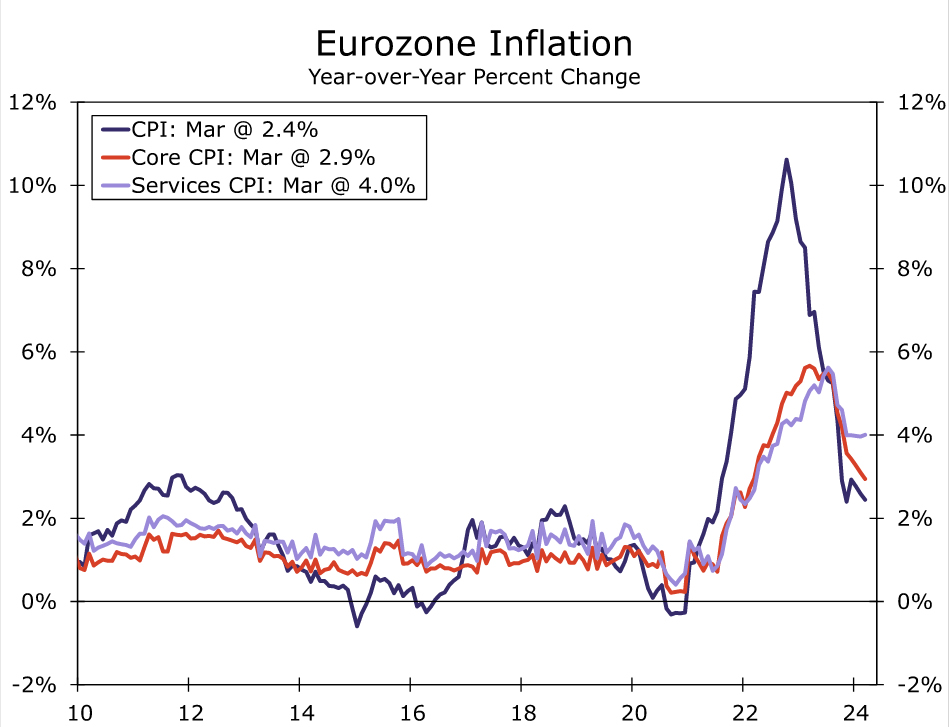

In a similar vein, we believe the stickiness in services inflation will prompt some caution on the part of ECB policymakers about an overly-aggressive pace of rate cuts. While year-over-year Eurozone March headline and core inflation surprised to the downside at 2.4% and 2.9% respectively, services inflation remained stuck at 4.0% for a fifth straight month. In fact, over a shorter timeframe, services inflation appears to have rebounded in the most recent months, with services prices advancing at a 5.4% annualized pace during the first quarter of this year. In addition to slowing wage growth, ECB policymakers may also want to see subsiding services inflation before adopting a steady ‘every-meeting’ approach to policy interest rate cuts.

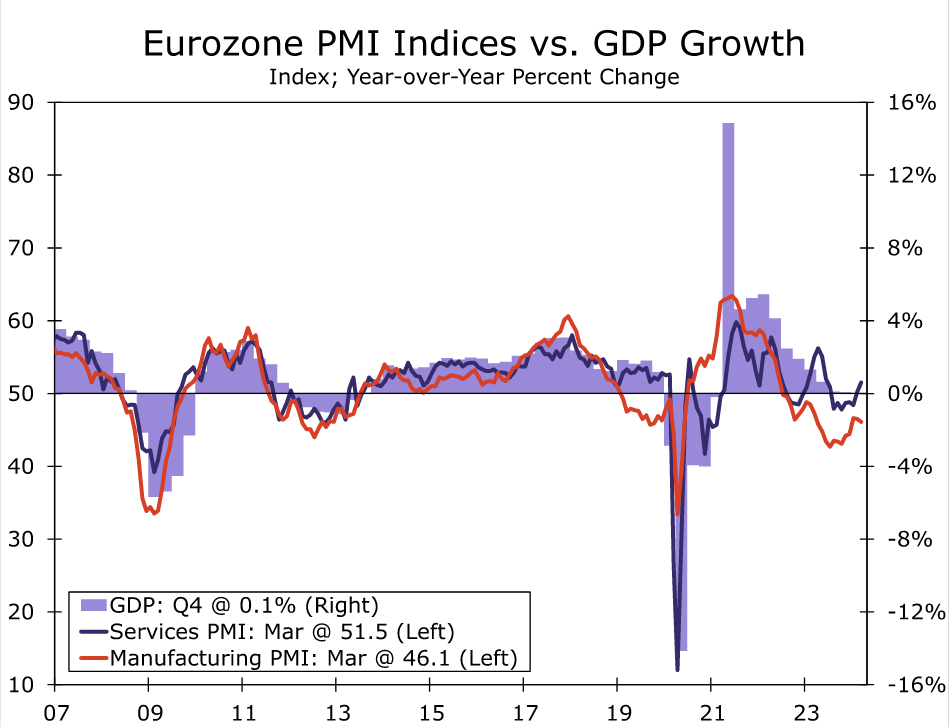

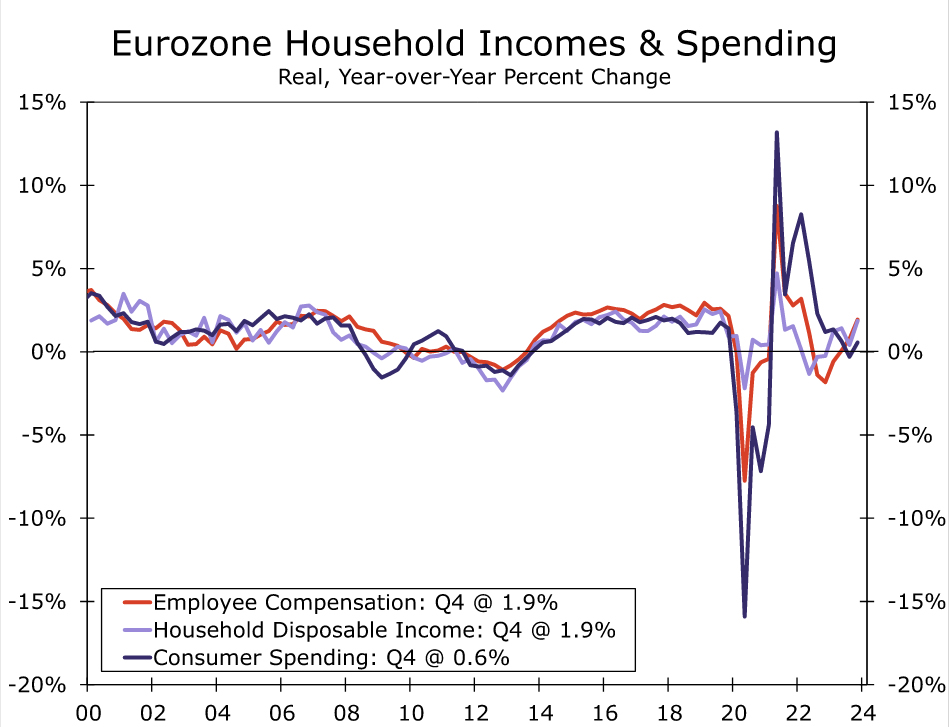

In terms of the outlook for economic activity, there are also arguments in support of an initially measured approach to European Central Bank monetary policy easing. For one, sentiment surveys have generally improved over the past several months. The March services PMI printed at 51.5 and the manufacturing PMI printed at 46.1, meaning that the composite (or economy-wide) PMI rose to 50.3 in March—the first reading above the breakeven 50 level since May of last year. The first release of the economic sector accounts for Q4 also highlight improving trends in real household incomes as inflation has receded. We estimate that growth in real household disposable income firmed to 1.9% year-over-year in Q4-2023 which, outside a pandemic-related spike, is the fastest growth in real household incomes since Q3-2019. The improvement in sentiment and consumer fundamentals suggests a gradual rebound in Eurozone economic growth as the year progresses, suggesting ECB can lower interest rates at a measured pace.

After today’s announcement and in the context of the ECB’s policy hints, we anticipate an initial 25 bps policy rate cut in June. However, we then expect the ECB to forgo monetary policy easing in July, and instead deliver 25 bps rate cuts in September, October and December for a cumulative 100 bps of easing this year. That is a slower pace of rate cuts than our previous forecast, though still more than the cumulative 76 bps of rate cuts currently priced in by market participants for the remainder of this year.

{kind=link}