The first estimate of U.S. Q1 gross domestic product next Thursday is expected to show another robust increase—extending a long stretch of outperformance in the U.S. economy versus advanced economy peers.

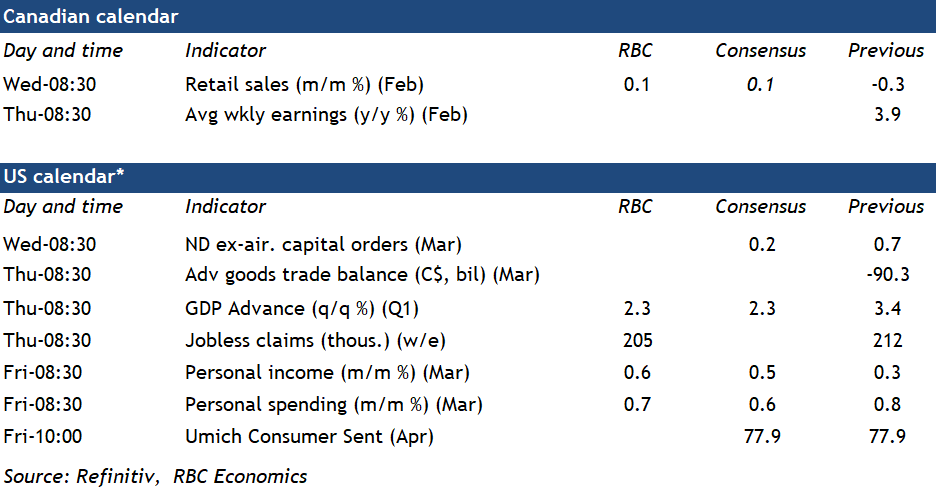

We expect U.S. output to have grown by an annualized 2.3% from Q4 last year, powered by stronger consumer spending and a tick-up in residential investment. But not all sectors of the economy have been faring equally well. Manufacturing production declined for a third straight quarter in Q1. And a pullback in non-residential construction will likely put an end to a string of five consecutive large quarterly increases in structures investment. But U.S. consumers continue to power through headwinds from higher interest rates as they hold onto ultra-long-term mortgages and spend out of savings accumulated during the pandemic. Core retail sales (excluding auto and gasoline stations) contracted mildly in January but rebounded in February and rose by almost 1 percent in March.

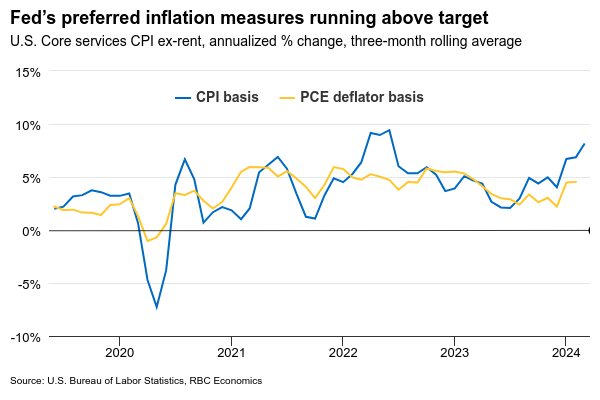

The strong U.S. economy is not as much of a concern for the Fed as is the re-emergence of inflation pressures. The tick higher in price growth—after having moderated sharply in 2023—alongside resilient consumer spending has revived likelihood that the economy will need to slow more significantly to get inflation pressures back fully in check. At a forum in Washington D.C. on Tuesday, Fed chair Jerome Powell highlighted a “lack of further progress” with inflation this year and how “it’s appropriate to allow restrictive policy further time to work.” Already, we’ve dialed back our expectation for rate cuts from the Fed this year, and now expect one 25 basis point rate cut in December. That’s also less than the 75 bps of cuts expected this year by the median FOMC policymaker in March. Moving forward, we continue to anticipate that the U.S. economy will start to lose its current momentum over the second half of 2024. But each additional upside surprise on economic growth and labour markets makes it less likely that inflation will resume a downward trend, and raises the risk that interest rates will need to remain higher for longer.

Week ahead data watch

Statistics Canada’s advance indicator showed retail sales edged up 0.1% in February mostly thanks to higher gasoline prices. A rise in unit auto sales (7% seasonally adjusted) points to some upside risk to the early February estimate but would still leave core retail sales (excluding gasoline stations and vehicles) down in February. Early indications for March are soft—auto sales retraced most of their February increase. Our tracking of card transactions also points to a broader pullback in spending in March.

We expect U.S. personal consumption to increase by 0.7% in March, given a robust retail sales increase. Personal income likely grew by 0.6%, echoing an uptick in March’s hourly wages (0.3%) and a 303,000 surge in employment.

February SEPH data will be watched closely for more signs of cooling in the Canadian labour market. Wage growth data will be closed watched, as it has been underperforming the timelier labour force survey data but is more in line with falling job openings, as hiring demand slows.

{kind=link}