U.S. Highlights

- U.S. headline retail sales beat expectations in March, advancing for a second consecutive month. The strong showing bolstered the case for a delayed start to the Fed’s interest rate cutting cycle.

- Comments from senior Federal Reserve officials has the timing of possible interest rate cuts in question amid signs of persistent strength in the U.S. economy and higher-than-anticipated inflation.

- In contrast, the housing market continues to feel the weight of higher interest rates as housing starts and home sales dipped in March.

Canadian Highlights

- The federal government took the stage this week as it presented a beefed-up budget, with a focus on addressing housing affordability.

- Canadian CPI inflation also made headlines with an encouraging print, which saw core inflation rates move further towards the Bank of Canada’s (BoC) target.

- Market expectations for the first BoC interest rate cut continued to solidify around June or July, increasing the probability that it will move ahead of the Fed.

U.S. – Dialing Back Expectations

This week featured releases on retail sales and the housing market in March. Also high on the market’s radar were comments made by the Federal Reserve Chair, which suggested the central bank may be changing its tune on the path and timing of interest rate cuts. Overall, markets responded strongly to the new information with stocks heading lower and treasury yields rising (10 year yields were up 9 basis points at time of writing) as investors recalibrated their expectations for rate cuts this year.

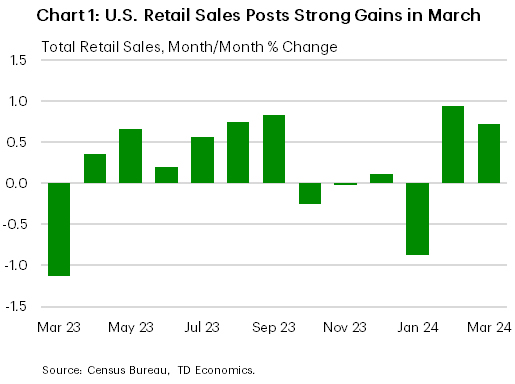

A stronger-than-expected gain in retail sales in March reinforced that the U.S. economy is still strong, and is expected to lead growth among developed countries this year, according to recent IMF projections. Headline retail sales rose for a second consecutive month in March, after a string of monthly declines, with sales in the key control group acting as a driver (Chart 1). Given the soft start to the year, March’s increase just managed to lift the quarter into positive territory (up 0.2% q/q annualized). The notable uptick also represents an upside risk to our own forecast for 2024 Q1 consumer spending, and doesn’t help the Fed in its goal of taming price growth.

On Tuesday, the Federal Reserve Chairman and the Vice Chair at two separate events both signaled that the central bank may be changing its tune. While policymakers started the year anticipating that they would commence the rate cutting cycle soon, hotter-than-expected inflation has shifted that calculus. In a prepared remark, Vice Chair Jefferson noted that interest rates could remain at their current restrictive level for longer if inflation persisted. Later, Fed Chair Powell echoed that sentiment. He noted that excluding a sudden economic slowdown, interest rates would need to stay restrictive for longer. The Fed Chair’s new tone is essentially one of dialing back expectations as markets had aggressively priced in numerous cuts this year. Investors on average are now expecting one and two cuts.

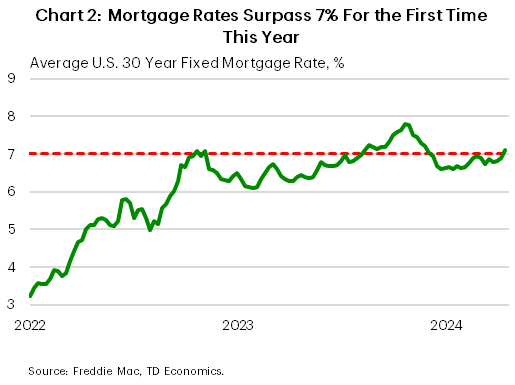

Higher rates are having a measurable effect on the housing market as data on existing home sales and housing starts and permits all declined in March. Both housing starts and building permits retrenched in March. In another release, existing home sales fell 4.3% m/m in March – the largest decline in over a year. While the measure managed to post a gain for the first quarter as a whole, relative to the subdued levels in 2023 Q4, the prospect of higher for longer interest rates are likely to see these gains pared back in the future. In fact, this week, the average rate on a 30-year fixed rate mortgage climbed above 7% for the first time this year and is likely to weigh on housing activity going forward (Chart 2).

Given recent readings on inflation and retail spending, and FOMC members comments acknowledging that rates will likely need to remain restrictive for longer, next week’s consumer spending and income data for March are highly anticipated. In particular, the Fed’s preferred inflation metric – the core PCE deflator – will be very closely watched to see how much of the recent hot CPI inflation carries over to PCE.

Canada – Another Big Budget for the Liberals

The federal government took the stage this week as it presented a beefed-up budget full of new spending promises. The government was applauded for making strides to address the country’s housing shortage but is also taking heat for hiking taxes via a new capital gains inclusion rate. Canadian CPI inflation made headlines too, with an encouraging print that reinforced bets the Bank of Canada (BoC) would initiate its first cut in June or July.

The Liberal government spent the better part of the last few weeks touring the country marketing its housing plan, which was fully unveiled in Budget 2024. This is one of the biggest pieces of housing policy Canada has ever seen, which aims to build nearly 4 million new homes by 2031. Encouragingly, there are also a host of policies to ramp-up rental supply, which has been stretched thin due to the government’s failure to control the rapid growth of Canada’s population. While the government is moving in the right direction, achieving its ambitious goals will be a challenge. Canada is currently on track to build just under 2 million homes over the next eight years, so doubling that will be a tall order for a construction sector that is already bumping up against capacity constraints.

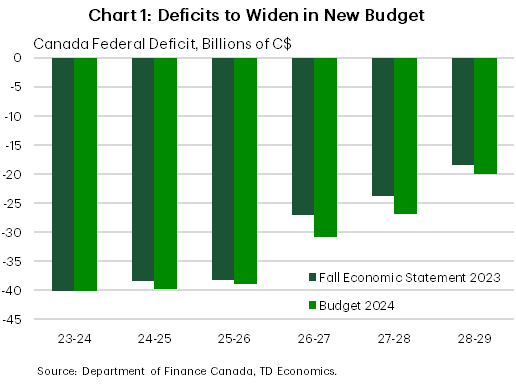

The budget wasn’t just about building new homes. The government announced $53 billion in new spending, with just 16% of that dedicated to housing. Indeed, there were over two hundred new policy items in the budget. There was spending on defence, pharmacare, a disability benefit, money for AI investment, an EV supply chain investment credit, and money aimed towards indigenous reconciliation. This continues a trend where the Liberal government attempts to fill as many gaps as it can through increased spending. Recall that the BoC has previously called out the government’s spending ways for contributing to Canadian inflation.

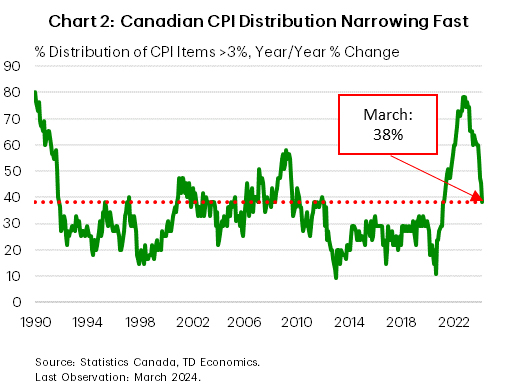

Speaking of inflation, it is not often that a Canadian CPI inflation report takes a backseat, but that’s what happened this week. Importantly, the average of the BoC’s core inflation measures came in at 3.0% year-on-year (down a tenth). On a three-month basis these are averaging just above one percent – a signal that the annual numbers will continue to decelerate in the coming months. This goes to the argument that we have been making for quite some time. That the slowdown in the Canadian economy has set the foundation for lower inflation. We are seeing this play out.

Has the BoC seen enough to cut rates? While we think the inflation evidence is clear, the central bank is taking a patient approach. While economic growth has been weak, the bottom hasn’t fallen out of the economy. This has afforded the Bank extra time to wait-out inflation, ensuring that the recent move is more durable. Notably, markets believe the moment is quickly approaching, with bets narrowing in on the June/July announcement dates. Interestingly, this also means that the BoC is expected to make its move well ahead of the Fed. The loonie has consequently reached it’s lowest level since late 2023 against the greenback.

as investors recalibrated their expectations for rate cuts this year.){kind=link}