- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 9 May, which is in line with consensus and current market pricing.

- Overall, we expect the MPC to soften its communication, priming the markets for imminent start to a cutting cycle. We expect the first 25bp cut in June.

- We expect EUR/GBP to end the day higher on a dovish vote split and remarks as well as a downward revision to the inflation forecast in the medium term.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 9 May, which is in line with consensus and current market pricing. We expect the vote split to be 7-2, with the majority voting for an unchanged decision and Ramsden joining Dhingra in voting for a cut. Note, this meeting will include both updated projections and a press conference following the release of the statement.

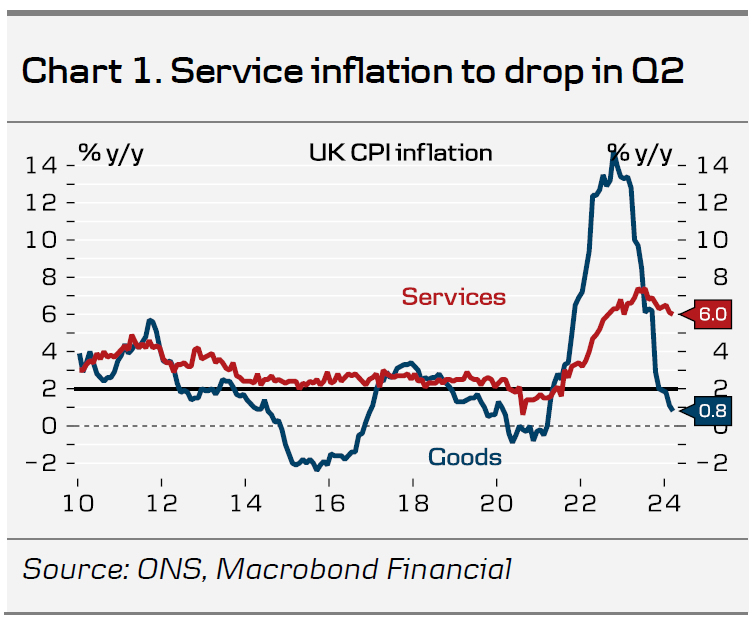

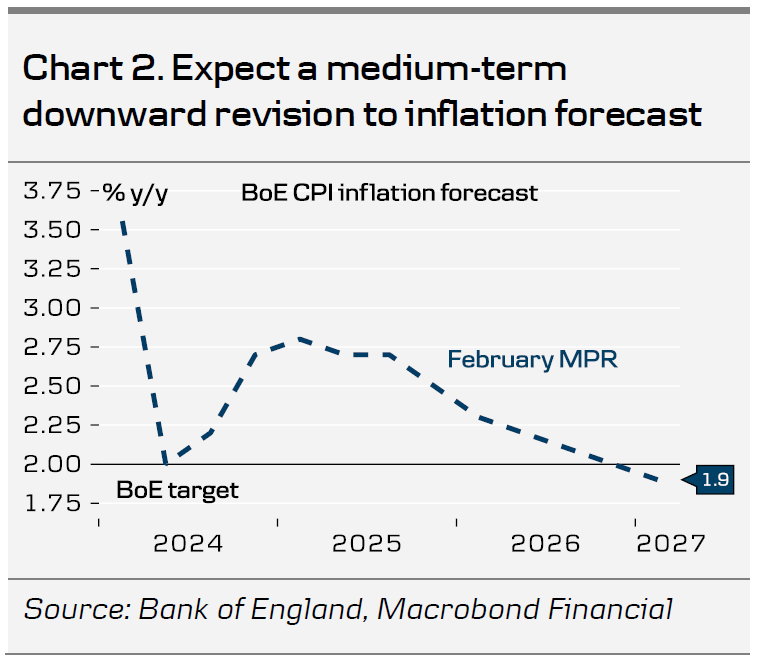

Overall, we expect the MPC to soften its communication, priming the markets for an imminent start to a cutting cycle. We expect them to retain much of its wording in terms of forward guidance, repeating that “monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level” and “the Committee will keep under review for how long Bank Rate should be maintained at its current level“. Since the last monetary policy decision in March, data has overall been slightly stronger than expected. Both headline and service inflation are slightly above the MPC’s forecast from February and wage growth is likely to overshoot the Q1 forecast of 5.7%. The growth backdrop remains a challenge for the MPC with the outlook of a growth rebound in 2024. We expect a downward revision of the inflation forecast in the medium-term as the implied Bank Rate conditioning path will be decisively higher with currently close to 45bp worth of cuts priced in for the year (vs 100bp in February MPR).

The MPC continues to be divided and increasingly within the internal members as well. Ramsden, who early in the hiking cycle was a hawkish dissenter, recently struck a dovish tone noting that “the balance of domestic risks to the outlook for UK inflation … is now tilted to the downside” and that he saw “promising developments in service inflation“. Likewise, Governor Bailey is leaning to the dovish side. On the other hand, Pill, who has voted with the majority for the entire hiking cycle, noted that a cut “remains some way off” and there is still “some way to go” before he is convinced of a sustainable return to the inflation target. We expect the majority to vote for a cut in June.

BoE call. We expect the BoE to prime markets for a rate cut at the meeting next week delivering the first cut of 25bp in June. We expect a 25bp cut in each of the subsequent quarters, totalling 75bp of rate cuts for 2024. Markets are pricing 45bp for the remainder of the year with the first 25bp cut only priced by August.

FX. In our base case we expect EUR/GBP to end the day higher on the back of a dovish vote split and remarks as well as a downward revision to the inflation forecast in the medium term. We expect this to be cautiously reemphasised during the press conference. Overall, we see relative rates as a negative for GBP and see current levels as attractive levels to sell GBP. We forecast EUR/GBP towards 0.89 in 6-12 months.

to keep the Bank Rate unchanged at 5.25% on 9 May, which is in line with consensus and current market pricing. We expect the vote split to be 7-2, with the majority voting for an unchanged decision and Ramsden joining Dhingra in voting for a cut. Note, this meeting will include both updated projections and a press conference following the release of the statement.){kind=link}