All eyes will be on U.S. April inflation numbers on Wednesday after a string of upside surprises made earlier expectations for interest rate cuts from the Federal Reserve in the near term unlikely. We expect to see some softening in price growth in April. Headline consumer price index growth is expected to be up 3.5% from a year ago, which is unchanged from March despite an uptick in energy price growth. Core (excluding food and energy) price growth is expected to slow to 3.6% from 3.8% in March.

Some signs of slower price growth (if materialized) would be welcomed by Fed officials, but the details of earlier price increases have been concerning. It will take more than one softer price report to calm inflation fears. The surge in price pressures in Q1 also came with a broadening out in pressures across a wider array of goods and services—particularly in the non-shelter services components that the Fed views as a better indicator of domestically driven price growth. Our view is that inflation pressures will ease over the second half of this year, but that is contingent on economic growth slowing and unemployment edging higher. We expect the Fed will stick to a wait-and-see approach over the summer while watching the data closely. We think the Fed will move to cut interest rates in December if domestic demand and inflation readings gradually move lower over the remainder of this year.

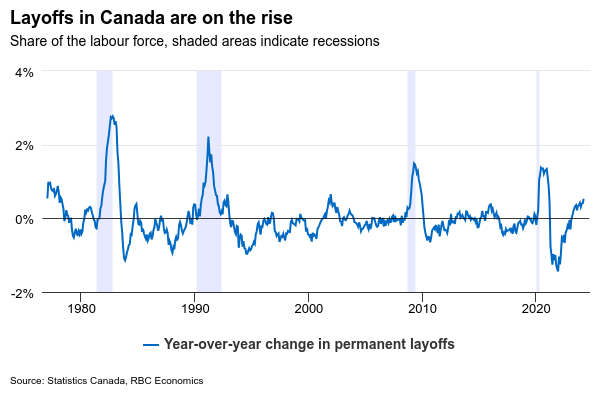

In Canada, data reports should confirm a softer economic backdrop at the end of Q1. Both manufacturing and wholesale sales contracted in March, according to preliminary estimates from Statistics Canada. Retail was little changed, and total hours worked (among private industries) fell by 0.3% from February. That leaves Q1 GDP on track for a seventh consecutive decline on a per-capita basis despite what increasingly looks like a temporary jump in output growth in January. In April, early reports on the housing market showed new listings picking up in major markets. That was, however, not met by an increase in demand, leaving overall resale activities at subdued levels at the start of Q2. The softer Canadian economic backdrop continues to call for earlier and more interest rate cuts from the Bank of Canada than the Fed this year.

Week ahead data watch

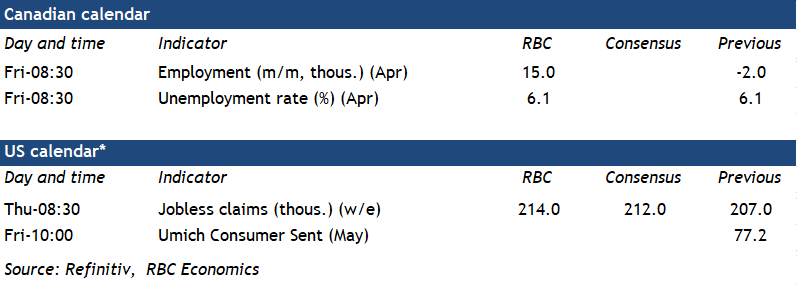

- We expect April Canadian housing starts were little changed at 243,000 units in April from 242,000 units in the prior month. Building permits have been slowing, with an annualized three-month rolling average value of 230,000 in February, down from the 233,000 units in January.

- We expect the April U.S. retail sales to tick up by 0.6%, mainly driven by higher auto sales and the price-related sales increase at gas stations.

- U.S. industrial output likely edged up 0.1% in April, led by an output gain in the utility sector, partially offsetting lower output in the mining sector.

price growth is expected to slow to 3.6% from 3.8% in March.){kind=link}