Markets

Both interest rate markets and the dollar held a wait-and-see mode this morning with EMU bonds slightly underperforming the US Treasuries. German ZEW investors sentiment again improved more than expected (expectations index from 42.9 to 47.1, the 10th consecutive improvement). This is not the most important input for the ECB, but it maybe marginally supported EMU yields. The focus of global markets however was on the first set US price data to be published this afternoon with the April producer prices. At 0.5% M/M for the headline figure and the measure excluding food and energy, monthly data were higher than expected, but the rise in the Y/Y-measure was slowed by a downward revision of the March data. Food price inflation was negative (-0.7% M/M), but services inflation (0.6% M/M) reaccelerated. US yields after the release briefly tried to reverse a small intraday decline, but soon relapsed, with markets looking forward to tomorrow’s CPI release. US yields currently decline 3-4 bps across the curve. German Bunds underperform with yields adding between 1-2 bps. ECB’s Wunsch in an interview with Handelsblatt was quoted that wage pressure persists, keeping services inflation high. In this context he wants the ECB to proceed gradually with rate cuts with no room for a back-to-back rate cut in July after a first step June. Equities show no clear trend. The rebound in the EuroStoxx 50 slows (-0.1% today) as the April top is again within reach. US indices also open marginally higher. Oil still struggles after recent losses (Brent $83 b/p).

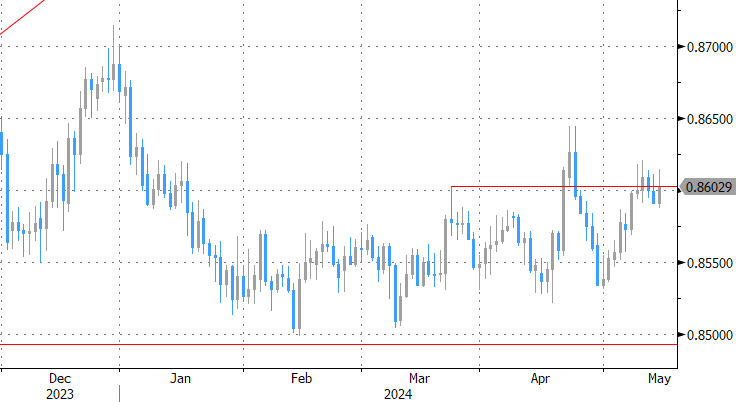

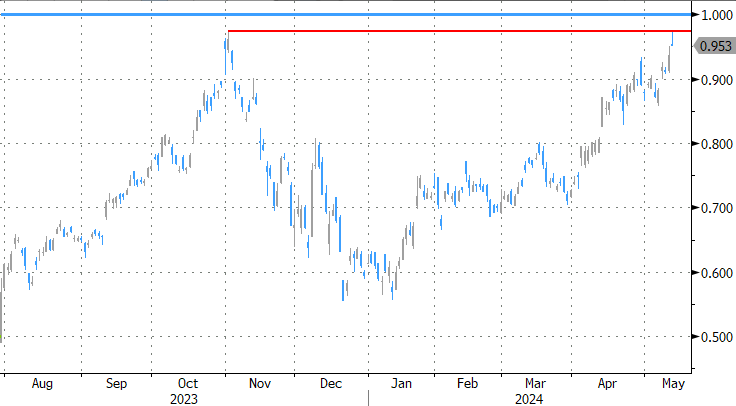

The modest reaction of US interest rate markets to the PPI release is keeping the dollar in the defensive. The DXY trade-weighted index returned to the 105 area. EUR/USD tries a second consecutive attempt to regain the 1.0811 ST top. A gradual, but protracted further rise in Japanese long term yields amid speculation on some further BOJ policy normalization (lower amount of bond buying) isn’t enough to prevent further yen losses (USD/JPY 156.4). Sterling this morning initially didn’t know how to react to mixed UK labour market data (wage growth ex bonus still 6.0% Y/Y, but a further decline in April payrolls of 85k). Later in the session, BoE Chief economist Pill sounded rather soft as he indicated that the BoE can cut rates while staying restrictive as the BOE is making good progress in bringing inflation back to target. UK yields today decline 2-3 bps across the curve. EUR/GBP reversed tentative early weakness and again trades just north of the 0.86 big figure.

News & Views

After hitting the lowest since 2012 in March, US small business optimism unexpectedly recovered from 88.5 to 89.7 in April. It’s the first increase of the year but the headline figure remains well below the 50-yr average of 98, the National Federation of Independent Business said. 22% reported that cost pressures, including historically high levels of employee compensation, was the single most important problem in their business. Key findings of the April report include that 26% plan price hikes in April, down seven points to the lowest reading since April last year. A slightly bigger percentage of firms reported that they plan to hire in the next three months, though the subindex remains near its lowest since 2016 (excluding the pandemic period in 2020). 40% reported job openings they could not fill in the current period, up three points from March, which was then the lowest reading since January 2021. The net percent of owners who expect real sales to be higher rose six points from March to a net negative 12%. General uncertainty crept higher to 78.0 in April.

The Hungarian forint extends its recent strong performance today. EUR/HUF hits a three-month low around 386.4 in the wake of MNB Virag speaking. The deputy governor stressed the need for further efforts to maintain the disinflation trend. He said the current benchmark rate of 7.75% can be cut towards 6.5-7% by the middle of the year but room for further easing in 2024H2 is limited. Virag’s comments come after Hungarian inflation on Friday printed higher in April for the first time in more than a year. Central banks in the region turned more hawkish in general (eg. CNB) over the recent weeks as they reckon that the easy part of easing price pressures is over. Inflation is even expected to grind higher again in the second half of the year, joining the bumpy path that lies ahead for the likes of the ECB and the Fed as well. The latter’s forced delay to cut rates is a key consideration too for CE central banks looking to maintain a sufficiently attractive real rate differential for their respective currencies.

Graphs

EUR/HUF: forint extends rebound as MNB Virag indicates room for further cuts might be limited in H2 of this year

EUR/USD tries to regain 1.0811 short-term top as US yields fail to rise on higher than expected US PPI.

EUR/GBP: sterling losing modestly as BoE Chief economist Pill sounds rather optimistic on rate cuts in the near future.

Japan 10-y yield near 1.0% barrier as markets ponder further BOJ policy normalisation.

. This is not the most important input for the ECB, but it maybe marginally supported EMU yields.){kind=link}