U.S. Highlights

- Headline PCE inflation came in flat for the month of May and core PCE inflation eased.

- Personal income posted a strong gain last month, while spending growth was more moderate, leading to an uptick in the savings rate.

- The heat in the economy still looks mainly to be in the service sector, as goods-producing industries contracted last quarter and goods prices continued to retreat in May.

Canadian Highlights

- May’s disappointing inflation report slashed the odds of a follow up rate cut by the BoC in July and is more consistent with our view that the next move down in rates will be in September.

- May’s report notwithstanding, inflation should cool moving forward, consistent with a softening jobs market. Data this week showed a dip in payrolls employment.

- Overall economic growth was firm in April. However, May’s preliminary forecast was soft. An economy currently in excess supply implies further downward pressure on inflation.

U.S. – Services Spending and Prices Starting to Settle

The past week had a relatively light data calendar for the U.S. economy, which continued on relative cruise control to gradually moderating economic growth and inflation. The current state of the economy was well summarized by Federal Reserve Board Governor Bowman in her speech earlier this week, which emphasized that we have seen only modest progress on inflation in 2024, despite moderating economic growth. The message holds true in the week’s data, which included an update on consumer prices and personal spending, as well as the revised reading on first-quarter GDP.

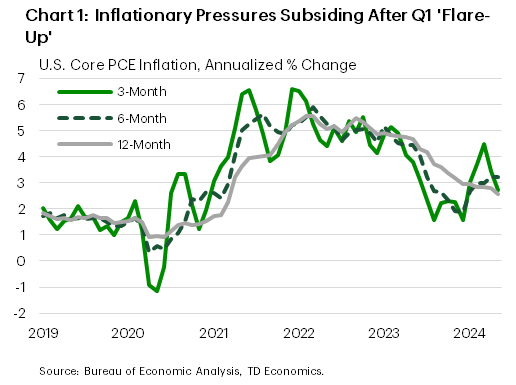

Inflation – as measured by the personal consumption (PCE) deflator – continued to moderate in May, with the core PCE deflator posting a ‘soft’ gain of 0.1% m/m – down sharply from the 0.3% gain registered the month prior. The deceleration in price pressures was entirely driven by another month of declines in goods prices and a further slowing in non-housing services prices. More critically, the three-month trend eased to a five-month low of 2.7% (annualized). Fed Governor Bowman repeated earlier this week that inflation has been slow to come down and more progress towards 2% is needed to support rate cuts this year. This morning’s data showed another (small) step in the right direction, though Fed officials will likely need to see at least another several ‘good’ inflation readings before having enough confidence to start dialing back the policy rate.

On the spending side, the release of May’s data showed some retrenchment in the goods and services split, with goods leading personal spending growth after having recorded declines in three of the four prior months. Overall, the softer gain in services spending implies our Q2 tracking for consumer spending is likely closer to 1.5%, which is a bit lower than what was assumed in our updated forecast published earlier this week.

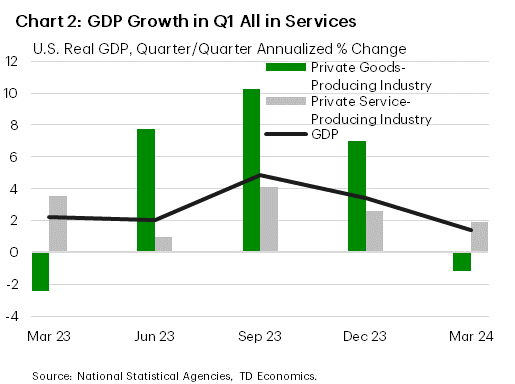

The last big piece of data out this week was the third estimate of first-quarter GDP. Usually, the 3rd estimate is not very exciting – after all, the first estimate was released two months ago, and revised minimally last month, only to be revised minimally again this week. Mostly old news, in that sense, but in the 3rd estimate we do get one new piece of data: the first look at GDP by industry for the quarter. Here, two observations quickly become clear – goods-producing industries contracted in the first quarter following several quarters of high growth in 2023, and services-producing industries, which had been supporting growth for over a year now, posted moderate growth relative to the last two quarters. The moderation of services growth coinciding with the downtrend in services inflation is an encouraging combination.

Next week, we will be closely following Chairman Powell’s words at the European Central Bank’s policy extravaganza at Sintra for a better view of how the central bank is digesting the latest data. Markets and other observers will also be focused on next week’s jobs data for any signs that the cooling we have seen in spending and prices is spilling over to the labour market.

Canada – Disappointing Inflation Print Affords Patience for the BoC

Market action this week was dictated by inflation reports from both north and south of the border. A disappointing Canadian report caused markets to push back strongly on the notion of a follow-up rate cut by the Bank of Canada in July. It also supports our call that the Bank can afford to wait until September until trimming its policy rate again. Bonds sold off in the wake of the report, pushing Canadian yields higher across the curve, although they gave up some of these gains on Friday amid a soft U.S. inflation print that showed some welcome cooling in price pressures. For its part, the loonie was down slightly on the week and remains in the lower end of the $0.72 – $0.76 USD range that’s been in place for the better part of two years.

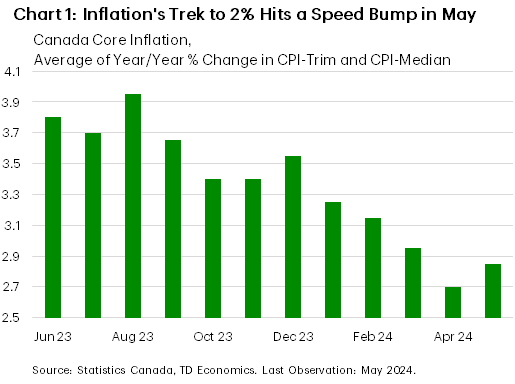

Canadian inflation had been on an improving trend for the first four months of 2024, increasing the Bank of Canada’s confidence that it was on a sustainable path back to 2% and paving the way for an early June rate cut – the first in four years. Against this promising backdrop, the May report landed with a thud, as both headline inflation and the Bank of Canada’s preferred core measures surprised to the upside. Indeed, both overall inflation and the average of the Bank’s core metrics ticked 0.2 percentage points higher to 2.9% year-on-year in May, boosted by shelter prices. However, nowhere is it written that inflation must take a straight line down to the 2% target, and there were bound to be some bumps along the way (Chart 1). An obvious example of this is in the U.S., where inflation heated up in the first quarter, before giving back some ground in recent months.

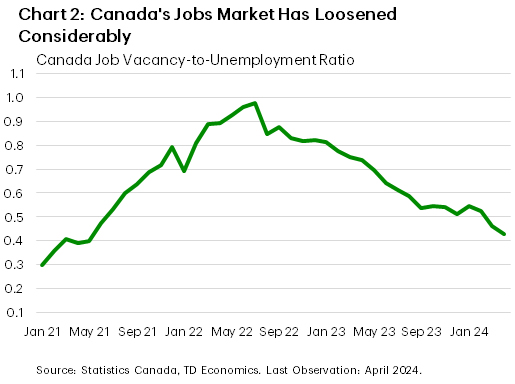

A potential concern coming out of Canada’s May CPI print is whether it’s a harbinger of some potential stickiness in inflation, raising the potential for higher for longer interest rates. While it’s too early to tell, our latest forecast anticipates a gradual easing in inflation pressures over the rest of 2024. A softening jobs market is a key reason that we expect inflation to ease further, with data this week showing that payroll employment declined in April. Meanwhile, both the job vacancy rate and the ratio of vacancies to the number of unemployed people (indicators of job market tightness) continued to decline from the highs observed a few years ago (Chart 2).Also encouraging was progress on wage growth, with average weekly earnings and the fixed-weight index of average hourly earnings both decelerating in April.

The likelihood that overall economic growth will be subdued moving forward is another good reason to expect inflation to be brought to heel. While this morning’s data showed that the economy expanded at an above-trend 0.3% month-on-month (m/m) in April, supported by monthly gains in 15 of 20 industries, May’s preliminary number was considerably weaker, showing a 0.1% m/m advance. All told, the second quarter is shaping up to be a decent one for growth. However, even with this performance the economy was likely in an “excess supply” position, meaning that the economy’s performance should be pressuring inflation lower, not higher, going forward.

{kind=link}