Summary

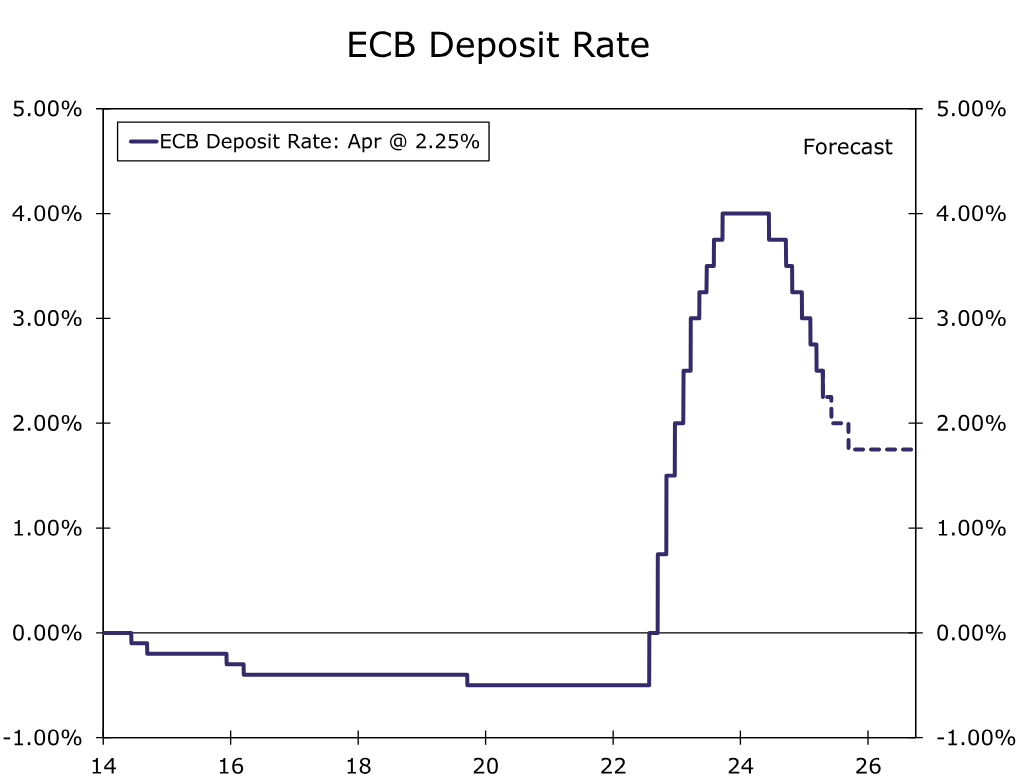

- The European Central Bank (ECB), in a widely expected decision, lowered its Deposit Rate by 25 bps to 2.25% at today’s announcement, while its accompanying statement was dovish overall in tone.

- In one significant change, the ECB no longer described its policy stance as restrictive. At the same time, however, it refrained from explicitly describing its policy stance as neutral, and moreover said the neutral rate concept only works in a “shock-free” world. Overall, we view these comments as providing scope for further easing.

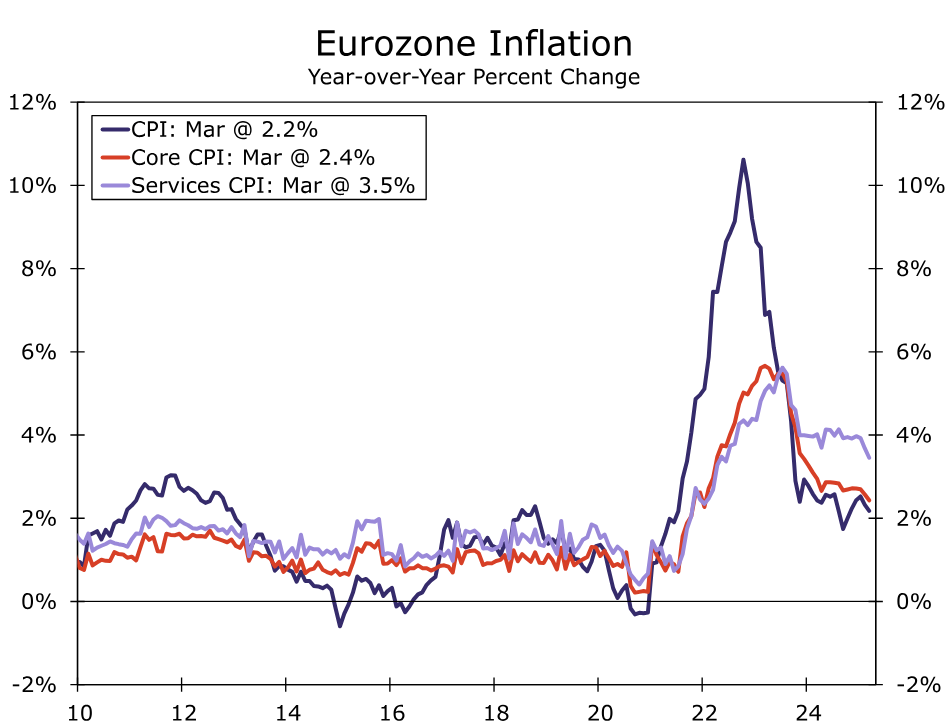

- Among the more dovish elements of the announcement, the ECB said the growth outlook had deteriorated, and noted slowing in headline and underlying inflation measures in March.

- Given the dovish overall tone, we remain comfortable with our view for the next 25 bps rate cut coming in June, and a final 25 bps rate cut in September, for a policy rate low of 1.75%. That said, we see the risks around this outlook as tilted toward faster and more pronounced easing. A rate cut at each and every meeting through September, for a policy rate low of 1.50%, is certainly a plausible scenario.

European Central Bank Cuts Rates, Maintains Dovish Outlook

The European Central Bank (ECB) cut its Deposit Rate by 25 bps to 2.25% at today’s monetary policy announcement in a widely expected decision, bringing the cumulative easing during the current cycle to 175 bps. Meanwhile, the accompanying announcement and post-meeting press conference leaned dovish on balance, keeping the path open for further rate cuts at upcoming meetings.

In one significant change, the ECB no longer described its monetary policy stance as “restrictive,” an adjustment that in isolation would be on the less-dovish end of the spectrum. In the same breath, however, the central bank did not explicitly describe the policy stance as “neutral,” and in the post-meeting press conference, ECB President Lagarde said the neutral rate concept only works in a “shock-free” world. We believe the central bank’s approach to characterizing its policy stance provides leeway for further rate cuts.

Among the more dovish elements of the announcement, the ECB downgraded its growth assessment, with ECB President Lagarde saying downside risks to growth had increased. More broadly in its assessment of the economy, the ECB’s announcement said:

“The euro area economy has been building up some resilience against global shocks, but the outlook for growth has deteriorated owing to rising trade tensions. Increased uncertainty is likely to reduce confidence among households and firms, and the adverse and volatile market response to the trade tensions is likely to have a tightening impact on financing conditions. These factors may further weigh on the economic outlook for the euro area.”

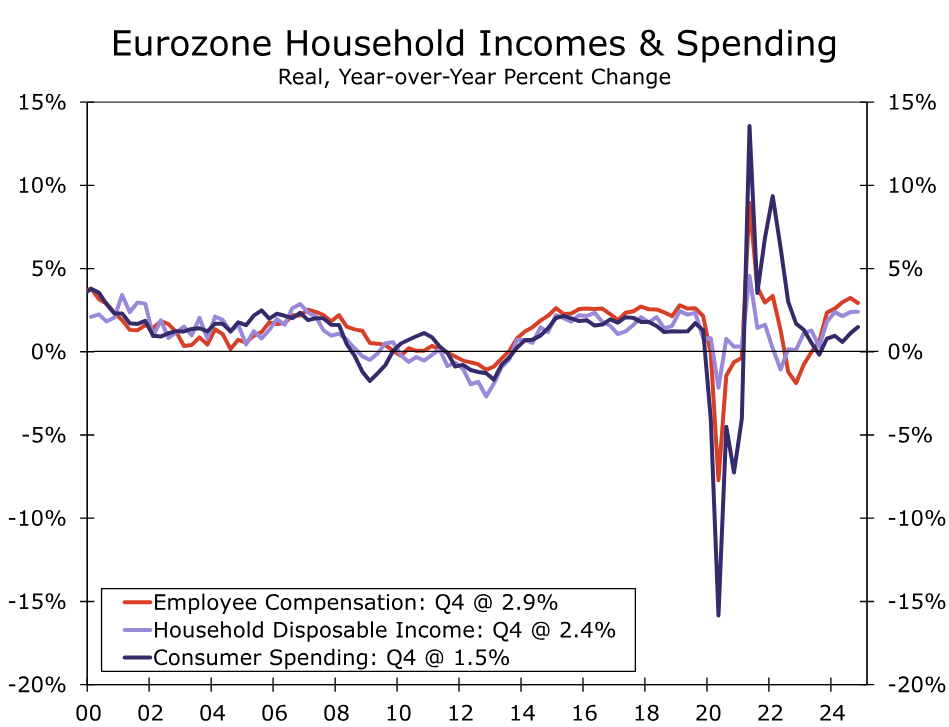

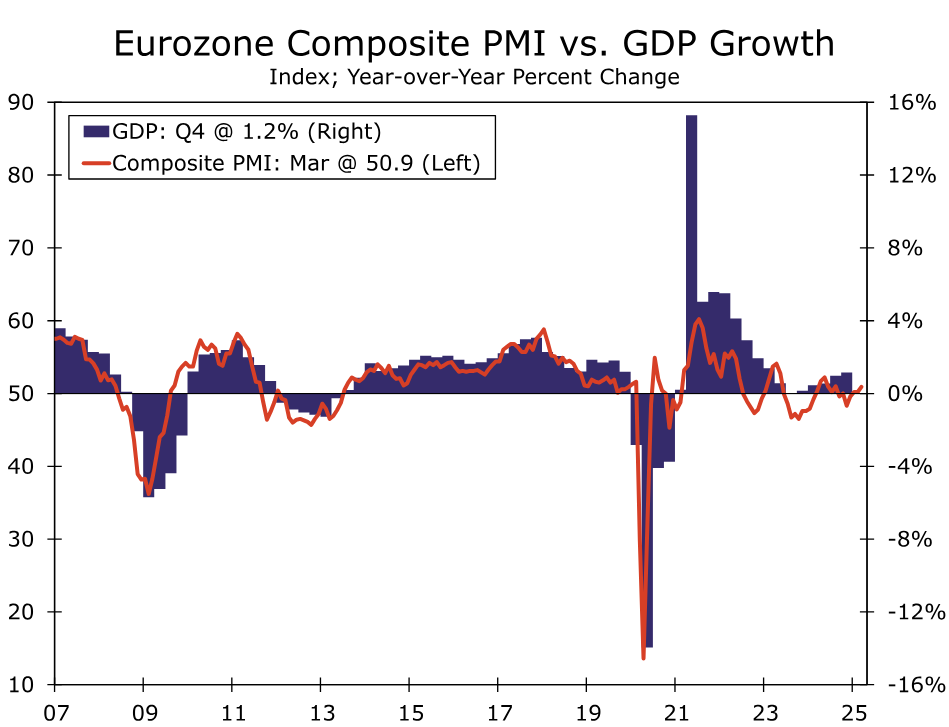

In terms of resilience, growth in real household disposable incomes continues to outpace consumer spending, while the housing saving rate remains elevated at 15.3%. However, today’s announcement suggests the central bank is placing limited weight on those factors and focusing instead on cyclical trends. On that front, sentiment surveys remain subdued. The Eurozone manufacturing and service sector PMIs were barely in growth territory in March, and the consensus forecast is for some further softening in April. That is consistent with our own outlook, as we recently revised our Eurozone GDP growth outlook lower to 0.6% for 2025 and 1.3% for 2026. The underwhelming Eurozone growth outlook and continued downside risks firmly argue for further easing.

Meanwhile, the ECB’s view on inflation was relatively sanguine. The central bank noted a slowing in headline and core inflation in March, and said services inflation has eased markedly over recent months. The ECB said wage growth is moderating, and Lagarde once again said that the ECB’s Wage Tracker pointed to slower wage growth ahead. To be sure, higher tariffs imposed by European governments could add to prices, although Lagarde said the impact on inflation was not clear yet.

Looking forward, the ECB was careful to offer limited guidance, saying “especially in current conditions of exceptional uncertainty, it will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance.” However, in the context of overall dovish comments we remain comfortable with our view of the next 25 bps ECB policy rate cut, to 2.00%, occurring at the June meeting. Beyond that we currently expect a pause in July and a final 25 bps rate cut to 1.75% in September. We acknowledge, however, that growth and inflation trends also mean the risks to our ECB rate outlook are tilted to the downside. Should Eurozone growth begin to show a much weaker trend and inflation remain benign, one can certainly envisage rate reductions at each and every meeting through September, for a policy rate low of 1.50%.

, in a widely expected decision, lowered its Deposit Rate by 25 bps to 2.25% at today's announcement, while its accompanying statement was dovish overall in tone.){kind=link}