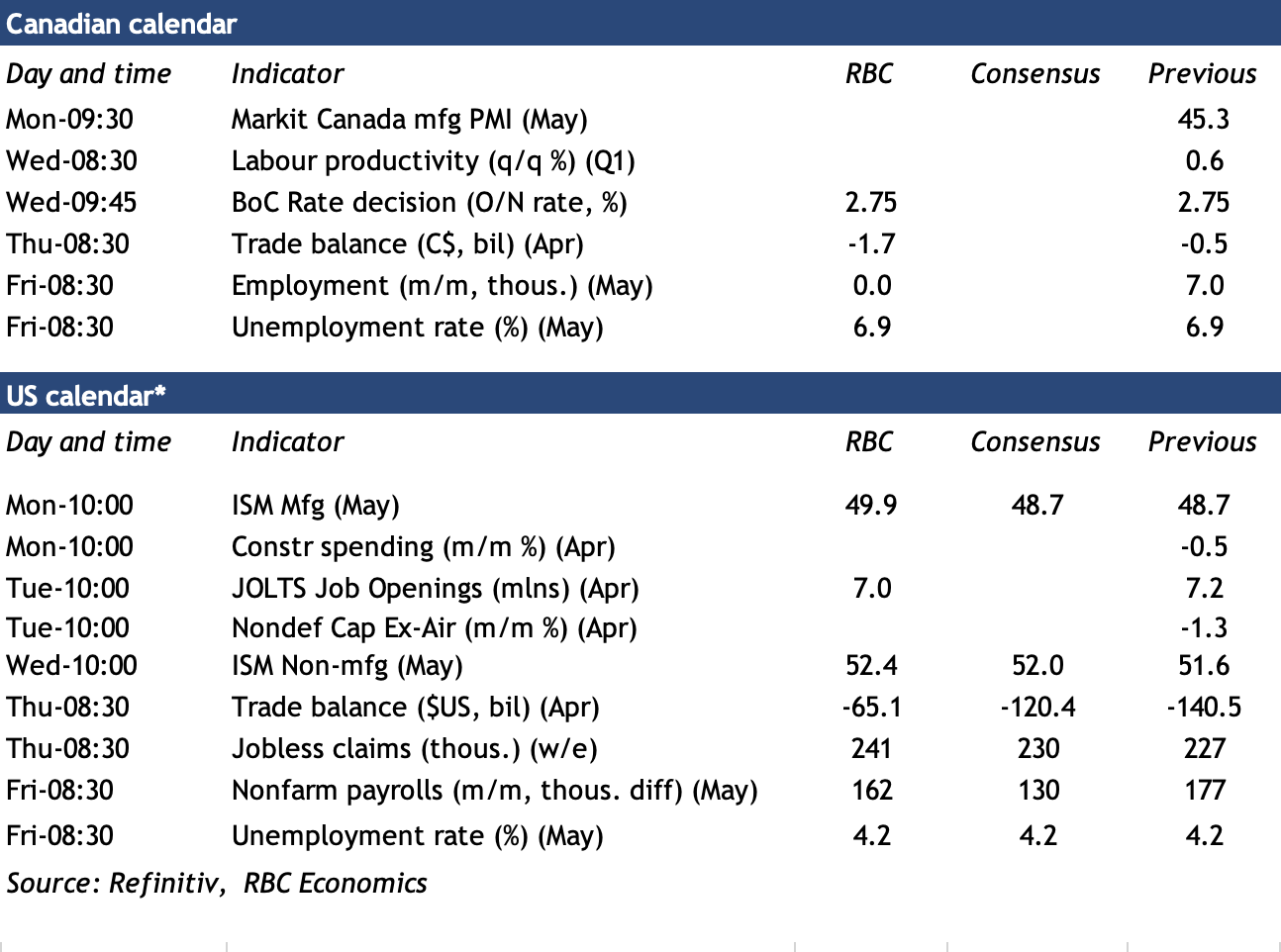

We expect the Bank of Canada will forego an interest rate cut on Wednesday in another close call following April’s pause after seven consecutive cuts.

Arguments for a rate cut still remain. Labour markets have weakened, particularly in manufacturing where jobs dropped by 30,600 in April—the largest one-month decline since the pandemic—pushing unemployment to 6.9% from 6.6% in Q1. Housing markets have cooled, reducing the risk that lower rates would reignite surging prices. Gross domestic product growth has remained positive, but the monthly pace slowed sharply after a surge in production in January.

However, the limited data since the BoC’s last decision in April hasn’t been entirely negative. Our RBC cardholder tracking shows consumer spending held up better than expected in March and April despite lower survey-based confidence measures.

Friday’s Canadian employment report for May (following the BoC decision) will likely show continued weakness in the industrial sector, but recent job postings on Indeed.com suggests hiring demand may be stabilizing. We expect employment to hold steady in May with the unemployment rate remaining at 6.9%.

April’s inflation data also surprised to the upside after accounting for the eliminated consumer carbon tax, driven more by domestic services growth than the impact of tariffs on imports.

Meanwhile, Thursday’s international trade data will likely show a widening Canadian trade deficit with exports falling more than imports. U.S. imports plunged 19.8% in April as the U.S. administration imposed reciprocal tariffs on most U.S. trade partners.

Significant U.S. tariffs remain in place. A U.S. court ruling blocking some of the Trump administration’s tariffs (including blanket tariffs on most U.S. trade partners in April) is under appeal, and the tariffs are still in effect for now. But CUSMA-compliant Canadian exports were already exempt from those measures. Sector-specific U.S. tariffs on steel, aluminum and vehicles remain as well, but we estimate more than 86% of Canadian exports still receive duty-free U.S. market access under the current rules.

The BoC has already cut rates by 225 basis points over the past year—more than other central banks. It still has room for further cuts if economic conditions weaken, but will need to consider any government spending support measures, which are better suited to provide targeted, timely, and temporary assistance to affected sectors than interest rate cuts.

Week ahead data watch

We expect U.S. payrolls likely grew by 162,000 in May, slightly down from the 177,000 in April. We also believe the unemployment rate held steady at 4.2%. The details will be closely watched for signs of softening in trade-sensitive sectors like manufacturing, but weekly initial jobless claims have remained low.

The U.S. trade deficit narrowed sharply in April in advance estimates with goods imports plunging 19.8% to retrace a pre-tariff run up, and exports rose slightly by 3.4%. The drop in imports likely partially reflected a reversal of a pre-tariff surge in gold imports, which won’t pass through to GDP measures for Q2. But, imports of autos and (non-auto) consumer goods declined by 19.1% and 32.3%, respectively.

{kind=link}