Canadian Highlights

- A U.S. court decision to block U.S. IEEPA tariffs could be a win for Canadian manufacturers if it’s upheld. Still, the U.S. has other legal means to impose tariffs on Canada, and sector-specific ones remain in place.

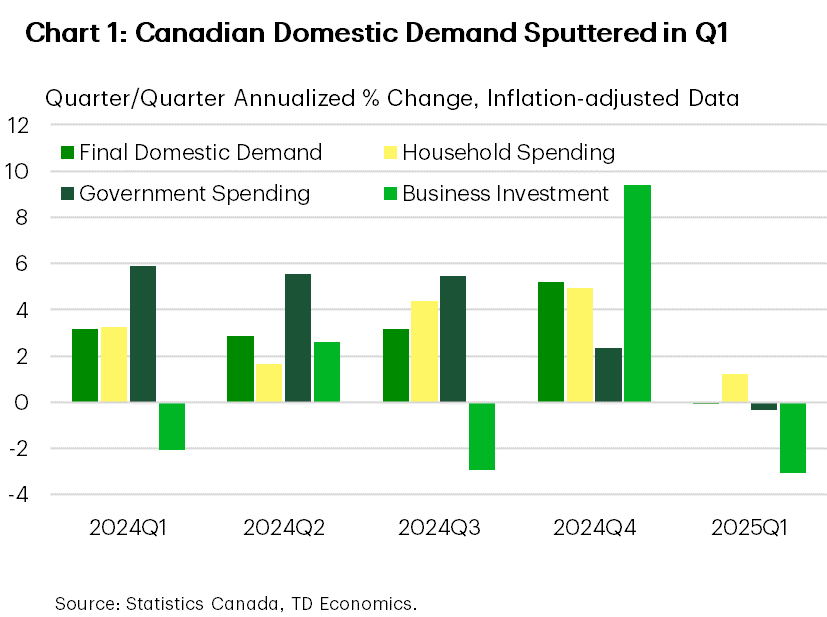

- Canadian GDP advanced at a reasonably firm 2.2% pace in Q1. However, domestic demand flatlined, reinforcing the narrative that Canada’s economy is softening.

- Markets expect Bank of Canada to hold the line on rates next week, although we still see two more cuts taking place this year as evidence of economic weakness mounts.

U.S. Highlights

- The tariff news felt like a tennis match this week. Tariff threats on the EU were paused. Then a court struck down the IEEPA tariffs, only to have an appeal court say they could remain in place.

- The economic data showed that inflation pressures were steady through April, while consumer spending has been very volatile so far in 2025.

- President Trump also voiced his desire for rate cuts directly to the Fed Chair this week. Powell reinforced his message that the Fed will be guided by the data.

Canada – President Trump, the King, and the BoC

Canadian equities were certainly on their best behaviour the week of King Charles’ visit to open Canadian Parliament – a first for a monarch since 1977. The TSX surged, although this had little to do with the royal visit, but rather improved sentiment after President Trump’s announcement that the deadline for punishing tariffs on the European Union would be pushed back to allow more time for negotiations.

Probably more notable for Canada was a U.S. court’s decision to block tariffs imposed by the U.S. through its International Emergency Economic Powers Act (IEEPA). The tariffs are staying on for now as the U.S. government appeals the decision, but if the IEEPA tariffs are indeed struck down, that would mean the end to the reciprocal U.S. import taxes announced in April and the duties applied in response to fentanyl trafficking. In Canada’s case, this means the 25% tariffs on non-CUSMA compliant items (10% on energy and other critical minerals) would be gone. However, product-specific tariffs are unaffected by the decision, leaving Canadian steel, aluminum and autos still tariffed. What’s more, the U.S. can use other means to impose tariffs, so the global trading system is not out of the woods yet.

Pivoting back to the Monarch’s Canadian visit, his throne speech was largely a reiteration of policies we’ve heard from the federal government. However, he did make the notable point that Canada will be involved with the European Union’s plan to significantly bolster its defense spending. As of now, Canada is targeting an increase in its defense spending to 2% of Canada’s GDP. However, this week’s announcement from NATO that this target for member countries is likely to be raised to 5% could ramp up the pressure on Canada to spend a significant degree more.

Even getting Canada’s defense expenditures from 2.0% to 3.5% of GDP would require about $45 billion per year in additional spending, so this effort could lift economic growth over time. In the here and now, however, the domestic side of Canada’s economy is flagging. This morning’s GDP report showed that while topline economic growth exceeded expectations (driven by tariff-front running) domestic demand was flat (Chart 1). It wasn’t all bad news however, as Statcan’s preliminary estimate pointed to a 0.1% monthly gain in April’s GDP, offering some upside risk to our forecast for a Q2 contraction.

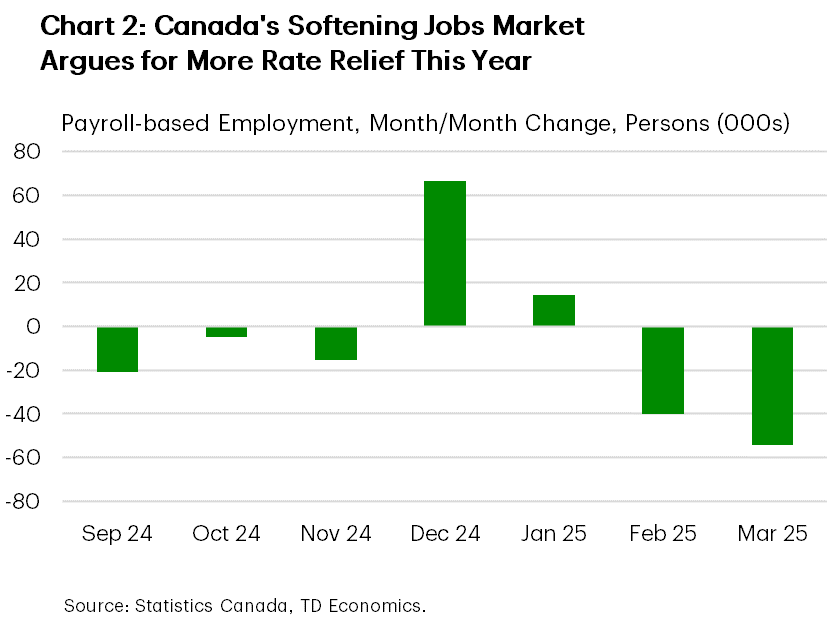

Next week, all eyes will be on the Bank of Canada’s interest rate decision. As it stands, markets expect policymakers to hold the line on rates, especially with a hot core inflation print in April, the federal election bringing the possibility of stimulus, and some global de-escalation in the trade war since the Bank’s last decision in April. On the other hand, Canada’s jobs market is weakening – a narrative reinforced by this week’s payroll data (Chart 2), and domestic activity flatlined in the first quarter. As Canada is likely entering a weak growth period, two more cuts are likely on tap for this year, even if the Bank stands pat next week.

U.S. – Tariff News Tennis Match Continues

Equity markets looked to end the week in the black as the tariff news tennis match seemed to net out on the good news side. The week started with a pause on Trump’s 50% tariff threat against the European Union, then a court struck down some of the Trump administrations’ tariffs before the appellate court deemed they could remain in place for now.

A U.S. trade court invalidated the Trump administration’s use of the International Emergency Economic Powers Act (IEEPA) to levy tariffs. These tariffs include the Canada/Mexico/China “fentanyl” tariffs and the 10% “reciprocal” tariffs. The court ruling has no impact on sectoral tariffs, including those on steel & aluminum and autos. These court battles don’t make it any clearer what will happen with tariffs in the near-term. The administration has other tools they could use to implement tariffs, so this may just be a bump in the road.

The revisions to first quarter economic growth didn’t really change the narrative. The slight contraction in the economy was due to a huge surge in imports, while the domestic economy was still running at a solid 2.5% pace. However, some of that growth was likely due to tariff front-running. These distortions make it harder to get a read on underlying momentum in the economy.

One potential warning sign in the first quarter data was a decline in corporate profits. The drop was seen in nonfinancial firms, which may be a signal that they are coming under pressure. However, April’s personal income data showed that income gains on the household side have been resilient. Incomes were boosted by the implementation of the Social Security Fairness Act, which provided a one-time lift. But even so, wages and salaries continue to grow at a healthy clip. Combined with softer spending growth, the personal savings rate ticked up to its highest level in a year, suggesting consumers have some gas in the tank.

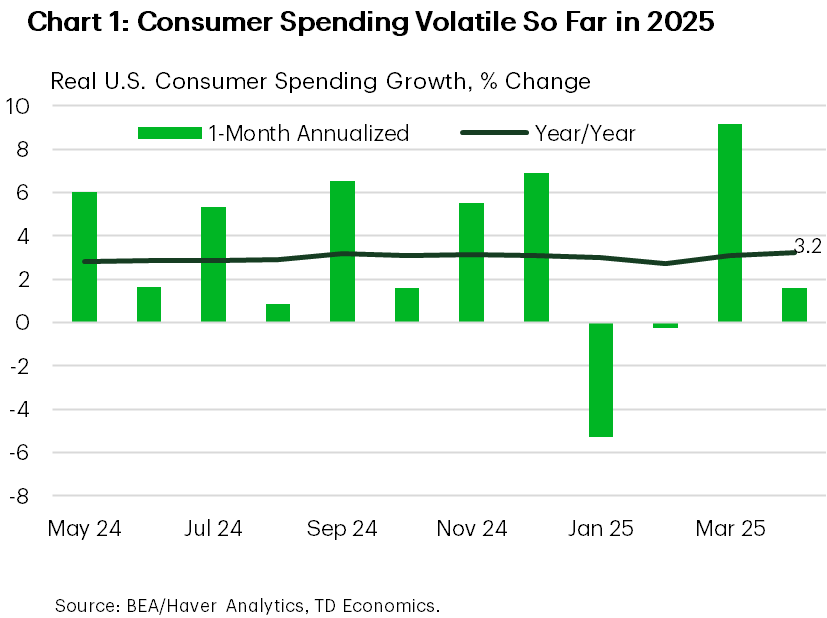

Consumers did take a bit of a breather in April after a solid increase in outlays in March (Chart 1). Consumer spending has been quite volatile so far in 2025, whipsawed by natural disasters and swings in durable goods purchases on things like autos as they try to front run tariffs. This makes it difficult to discern a trend in consumer spending. Even so, we expect that weaker sentiment and a softer labor market ahead will cool the pace of spending in the coming quarters.

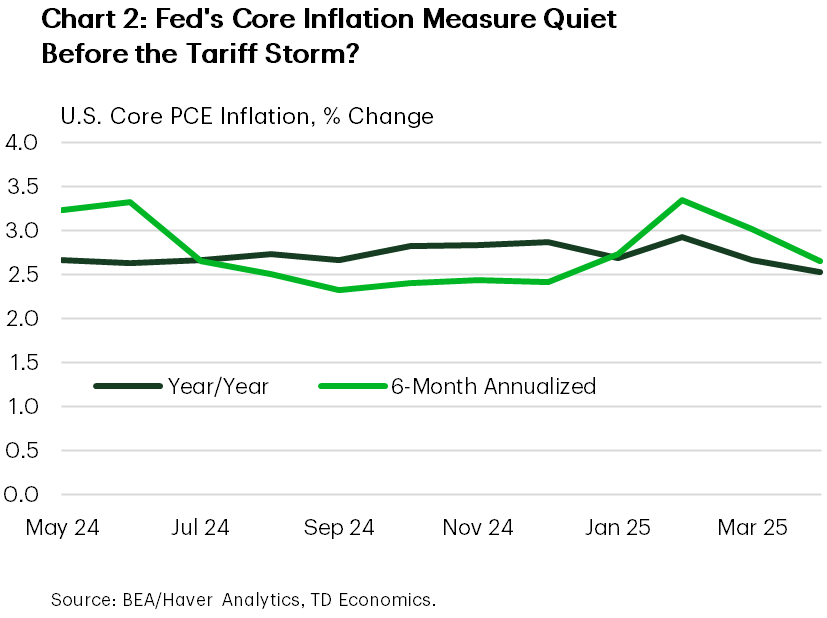

The inflation news was steady-as-she goes in April (Chart 2). However, it is a bit early yet to see much inflation pressure from tariffs. We expect inflation will be lifted above 3% later this year as companies pass along higher tariffs to consumers.

President Trump met with Fed Chair Powell for the first time in his second term, reiterating his view that the Fed is making a mistake by not lowering interest rates. Powell stressed that policy decisions would be dependent on the economic data. The Fed minutes from their decision in early May suggested that they are in no hurry to cut rates as they wait for more clarity on the tariff front. Volatility is making it difficult to get clarity on the economic data these days. Add it all up, and the Fed’s wait and see approach is warranted for now.

{kind=link}