- The Fed maintained its monetary policy unchanged as widely expected.

- The updated median ‘dots’ still signal two more 25bp rate cuts by the end of the year. Median rate projection for 2026-27 shifted 25bp higher, but the distribution of views within FOMC remained little changed.

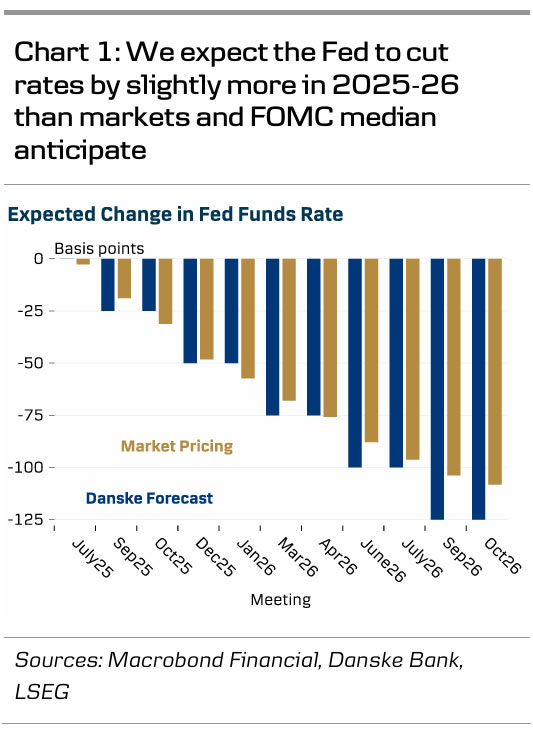

- Market reaction was generally muted. We still expect the Fed to cut in September and December, followed by three more reductions in 2026. We forecast EUR/USD at 1.20 and 10y UST yield at 4.50% in 12M horizon.

FOMC’s June meeting was mostly about stocktaking as tariff uncertainty leaves little room for forward-looking policy views. Powell repeated the familiar message of the Fed remaining ‘in a good place’ with its current policy stance.

The policy statement was little changed, as the Fed only omitted the May addition of “[committee] judges that the risks of higher unemployment and higher inflation have risen”. Powell clarified that the Fed sees peak-trade war uncertainty easing, but that uncertainty in general remains elevated.

In our preview, we speculated if the Fed would take a firmer stance on whether the trade war appeared more concerning from inflation or labour market standpoint. That was not the case, however, as the Fed does not yet appear confident enough to draw strong conclusions from data received since the ‘Liberation Day’.

Median 2025 GDP forecast was revised down to 1.4% (from 1.7%) and 2026 to 1.6% (from 1.8%) – largely in line with expectations. Both inflation and unemployment rate forecasts were revised up modestly. Powell affirmed that incoming data on both labour markets and inflation has been promising, but that the Fed continues to monitor how the tariff costs will be absorbed by consumers and businesses before cutting rates further.

The median ‘dots’ still signal two rate cuts over the rest of the year. The median rate projection was revised up by 25bp for 2026-27, now signalling only one cut each year. However, the central tendency range (which illustrates the distribution of views omitting the three highest and lowest observations) remained completely unchanged throughout the forecast horizon. Participants judged that risks surrounding the GDP estimate remain skewed to the downside, and to the upside for inflation – as was the case in March.

Powell downplayed the risk of persistent inflation pressures stemming from the Israel-Iran conflict, which is well in line with the Fed’s general tendency to look through short-term volatility in financial conditions.

We maintain our Fed call unchanged and still see 25bp rate cuts in September and December this year, followed by three more reductions in 2026. As we gain more clarity around both the level of tariffs and their pass-through to prices, and as economic growth continues to cool both cyclically and structurally, we think the Fed still has plenty of room for cuts ahead. Market reaction was limited, and markets price in around 18bp worth of cumulative cuts by September and 48bp by December.

{kind=link}