{kind=link}

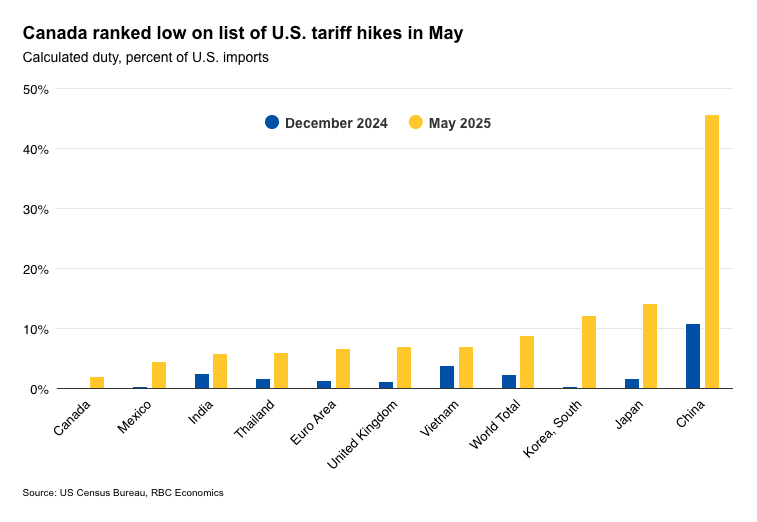

Tariffs on Canadian goods announced by the U.S. on July 31 do not significantly alter Canada’s economic outlook.

The International Emergency Economic Powers Act (IEEPA) tariff increased from 25% to 35%, but still only applies to the portion of trade that is not compliant with the free trade CUSMA/USMCA. That exemption is maintaining duty free access to the U.S. market for the majority of Canadian exports by our calculations, and remains in place.

Overnight tariffs hikes on other countries will still push the effective U.S. tariff rate higher to the top end of the 10-15% range that we have been assuming for our base case outlook.

This outcome, while impactful, remains less severe than the more negative scenarios that appeared more possible earlier this year. Canada should maintain among the lowest (if not the lowest) effective tariff rate of any major U.S. trade partner under the updated rules.

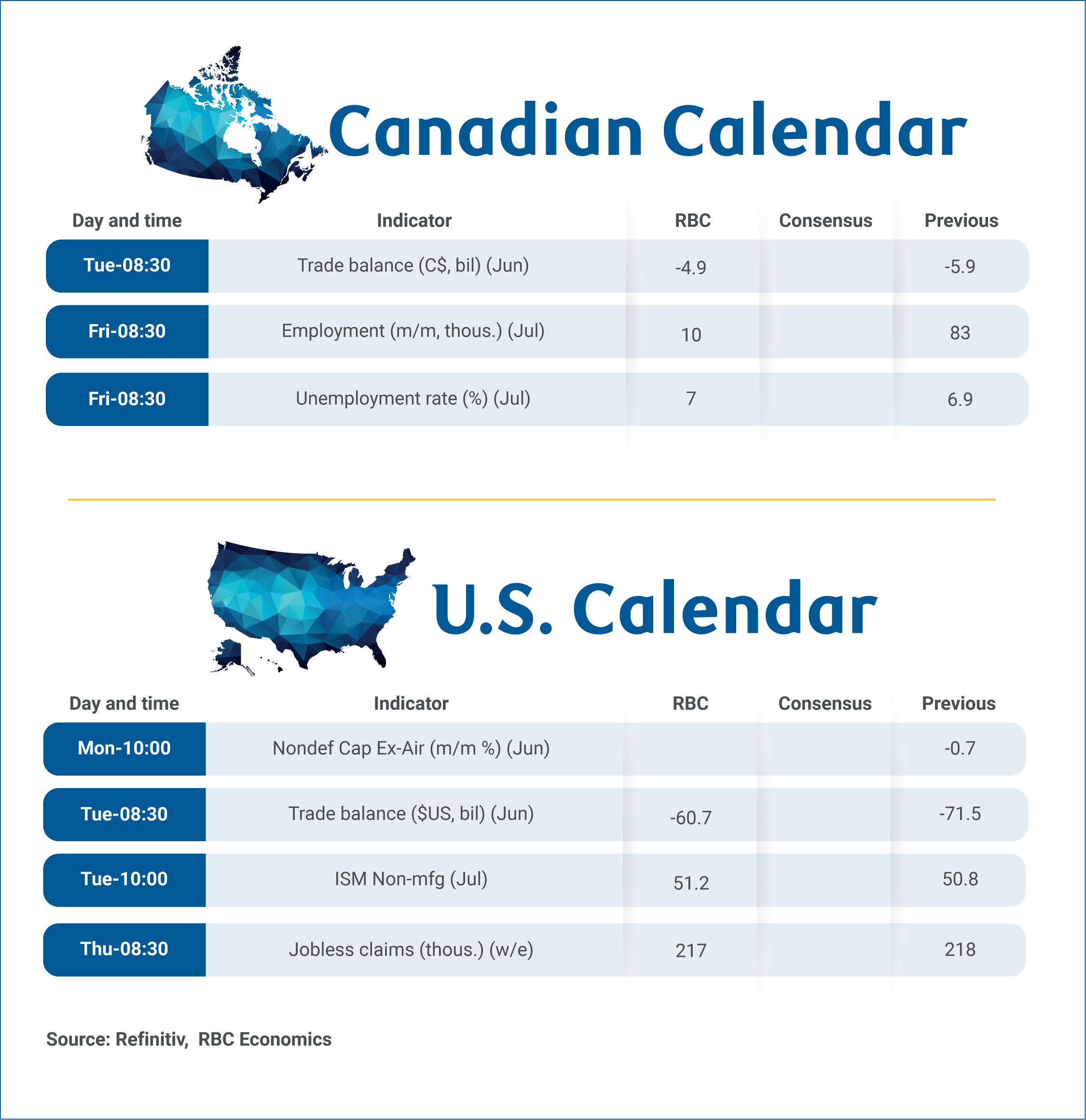

Canadian labour markets to show further signs of resilience

We expect employment and the unemployment rate ticked higher in July after an outsized 83,100 jobs’ gain in June pushed the unemployment rate unexpectedly lower.

One upside surprise in employment doesn’t negate months of prior softening, and the 6.9% unemployment rate in June was still up half a percent from a year ago, and is historically elevated.

The nuance is that much of the deterioration in the labour market had been concentrated in goods-producing industries, particularly manufacturing, which has lost jobs from international trade headwinds. Meanwhile, services sectors have been broadly resilient, accounting for nearly all of the job growth in Canada since last summer.

We expect this bifurcation to continue, resulting in modest job growth in July with the unemployment rate edging slightly higher to 7%. Education is a sector to keep an eye on as seasonal patterns around summer can create volatility. Beyond July, we believe deterioration in the labour market is likely approaching a bottom if it hasn’t already.

That outlook is contingent on the assumption of limited additional erosion in trade relations between Canada and the U.S. Evidence has been mounting, including from Statistics Canada’s early Q2 gross domestic product estimates, that existing U.S. tariffs on Canada are having a less severe impact than initially feared.

Exports to tick higher on oil price surge

But, that doesn’t mean tariffs aren’t damaging trade. June’s international trade data on Tuesday is expected to show Canadian exports ticked higher, but only due to a 10% jump in oil prices.

Export volumes likely declined again after accounting for the price changes, consistent with another significant drop in U.S. imports. Nevertheless, we expect those exports were still subject to lower average U.S. tariffs compared to exports from other major U.S. trade partners.

Negotiation between Canada and the U.S. on a trade deal is ongoing and the outcome is uncertain. But we expect growth in the economy will stay soft, but positive, and the Bank of Canada is not expected to cut interest rates again.

Week ahead data watch:

In Canada, we anticipate the trade deficit narrowed to $4.9 billion in June. Export growth was likely supported by higher oil prices. Meanwhile, a decline in motor vehicle unit production likely restrained import growth once again.

In the U.S., the trade deficit is expected to be about US$60.7 billion in June. Based on advance economic indicators, the goods trade deficit narrowed by 10.8% with both goods exports and imports declining by 0.6% and 4.2%, respectively.