{kind=link}

Canadian Highlights

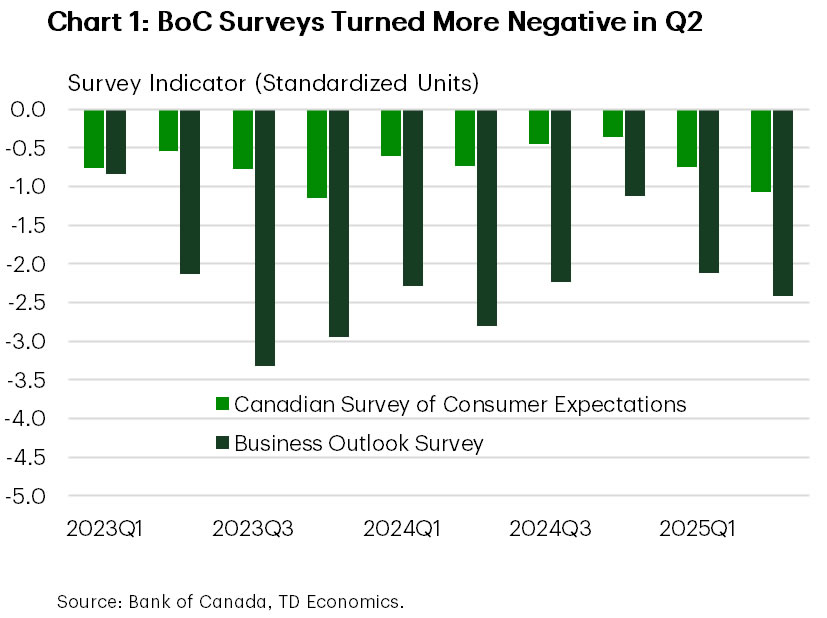

- This week offered a clearer picture of business and consumer sentiment. Both surveys turned more negative in Q2, with domestic demand expected to remain soft and investment outlook flashing a weak signal for Q3.

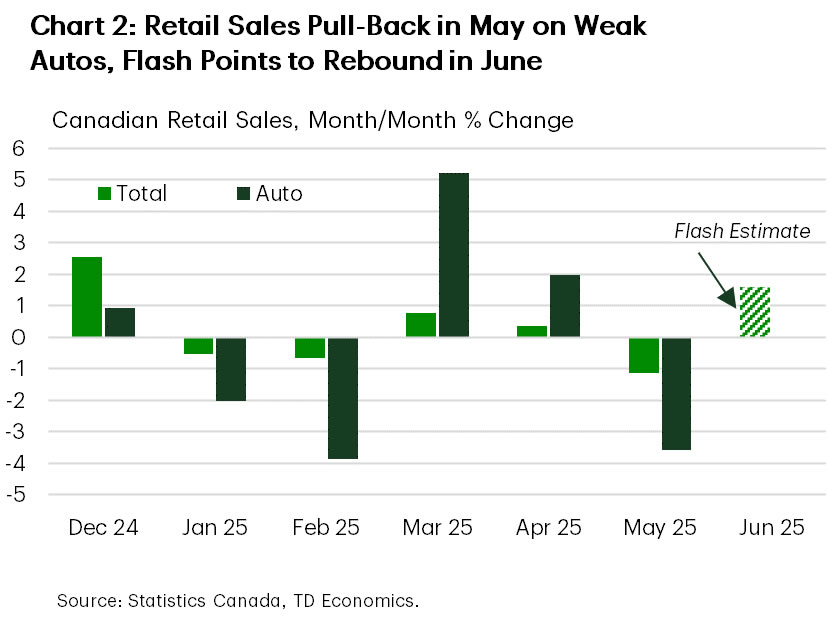

- The retail sales report showed a sharp pull-back in May spending, led by autos. The advance estimate for June suggests a rebound, likely keeping quarterly goods spending steady overall.

- Longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the BoC. July’s rate decision is essentially locked in as a hold – the real question is whether the Bank stays on hold in September and beyond.

U.S. Highlights

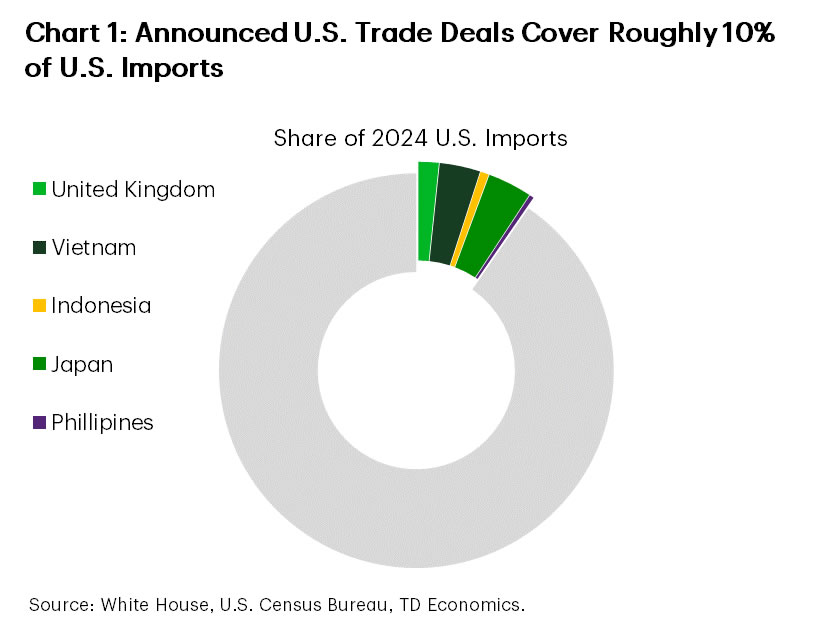

- President Trump announced a few trade deals this week, most importantly with Japan. Under this “deal” Japanese imports will still face a 15% “reciprocal” tariff, which is lower than the 25% threatened in the past. The deal included a $550 billion Japanese investment package, but the details remain scarce.

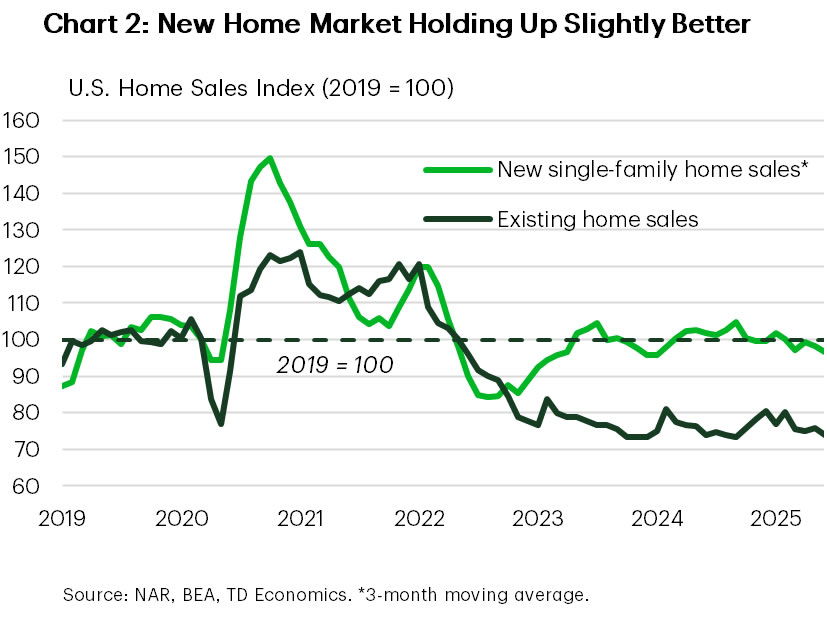

- Existing home sales weakened more than expected in June, with the level of sales holding near GFC lows. However, median home prices rose 2.0% y/y, a slight improvement from the month prior.

Canada – Not Strong Enough to Cheer, Not Weak Enough to Cut

This week’s economic calendar wasn’t expected to move markets. Equity markets drifted higher on optimism around U.S. trade deals, while bond yields edged up modestly after falling for most of the week.

Instead, the data offered a clearer picture of business and consumer sentiment, along with a detailed look at May’s retail spending. Both the business and consumer surveys turned more negative in Q2, reversing the cautious optimism that had emerged late last year (Chart 1). However, the interviews, conducted from late April through May, came after the temporary relief was granted to CUSMA-compliant trade, which helped ease some pressure. Recession fears among firms and households ticked lower, and businesses reported modest improvement in some areas affected by trade.

Despite easing recession fears, the tone from businesses was far from upbeat. Domestic demand is expected to stay soft. Firms’ future sales expectations turned negative for the first time in a year. The outlook for exports sales improved for all but the manufacturing and auto-related sectors. The investment outlook, while slightly better than last quarter, remains well below average and just a quarter of where it stood in late 2024. Even then, most firms are sticking to routine maintenance rather than expanding capacity or improving productivity – a weak signal for the third quarter investment outlook.

On the consumer side, the Bank’s new sentiment index showed a second straight quarterly decline, reflecting slowing spending growth. That was confirmed by May’s retail sales report, which showed nominal spending down 1.1% and inflation-adjusted spending down 1.4% month-on-month. The sharp pull-back was led by auto sales, as the tariff-driven front-loading in March and April reversed course (Chart 2). Core sales, which excludes auto sales and receipts at gas stations, were flat in nominal and real terms. The flash estimate for June sales points to a rebound, which could keep quarterly goods spending steady overall. But services will determine the broader trajectory of personal consumption – and if consumers act on what they are saying in the survey, it will likely remain subdued.

Meanwhile, longer-term consumer inflation expectations ticked slightly higher, though are unlikely to cause much concern for the Bank of Canada. Firms also expect somewhat stronger input costs due to tariffs, though most say that they’ll absorb them through profit margins given weak demand. Services inflation remains the sticking point. According to CMHC, new rents are falling thanks to increased supply. However, existing rent inflation remains elevated, even as it has slowed relative to last year.

In short, the data doesn’t signal a collapse, but it doesn’t suggest strength either. This week’s releases don’t shift the dial for the Bank with July’s rate decision now essentially locked in – the employment report sealed a hold. The real question now is whether it stays on hold in September and beyond. For now, markets are only pricing in half a cut by year-end.

U.S. – Trade Deals Trickle in Ahead of August 1st

This fourth week of July was light on the data front, with only housing data on the docket. Trade developments continued to dominate the limelight, with trade “deals” announced with Japan, the Philippines and Indonesia. Progress on the trade front appeared to prop up financial markets, with the S&P 500 up 1.3% on the week.

U.S.-Japan goods trade is worth about $227 billion, so a trade deal is certainly a welcome development. Imports from Japan ($148.4 billion last year) will now face a 15% so-called reciprocal tariff, which is lower than the 25% that had been threatened in the past. The deal also reportedly included a $550 billion Japanese investment package, but the fine details on it remain scarce. Shares of Japanese carmakers rose on the news, but the largest American carmakers expressed concern that the deal could put them at a disadvantage. The trade deal with the Philippines received less attention. Imports from the Philippines will face a slightly higher tariff of 19%, slightly higher than the 17% announced on Liberation Day. This adds to a string of recent agreements, including those with the U.K., Vietnam and Indonesia (Chart 1). But the more important ones, such as those with China, Canada, Mexico and the EU, have yet to be reached.

On the data front, the housing market continues to struggle under the weight of high mortgage rates. Existing home sales fell 2.7% m/m in June, coming in well-below expectations for a lighter pullback. Sales were down 8% from the end of last year and at a level of 3.93 million (seasonally adjusted annual rate) continued to hover near GFC lows. The months’ supply of inventory improved slightly, coming in at a seasonally adjusted 4.4 months from 4.3 in May. Amidst this backdrop, home price growth remained in the slow lane, but did see a modest improvement, rising to 2.0% year-on-year (y/y) from 1.6% in the month prior. With mortgage rates holding stubbornly near 7%, we’re unlikely to see a sustained turnaround in resale activity over the near-term. An improved interest rate backdrop expected later this year should help at the margin. High mortgage rates also continue to take a toll on the new home market, even as activity in this small corner of housing is holding up slightly better, with builder incentives likely providing some modest support (Chart 2).

Next week is sure to be more action packed. Aside from the potential for more trade deals to emerge ahead of Trump’s August 1st deadline, a host of important data reports are slated to be released next week. This includes second-quarter GDP, June’s PCE inflation, the July jobs report, and an FOMC rate-setting meeting. Market odds suggest the Fed is all but certain to keep the policy rate unchanged next week. That said, it appears that there will be at least one dissenter among the voters with Fed Gov. Waller recently urging for a July cut, while Fed Gov. Bowman has also expressed her openness to this. Signs of a growing divide within the Fed could lead to more volatility. In this vein, next week’s FOMC decision will be parsed over thoroughly for any of these signs and any potential clues as to how soon the committee could begin cutting rates, with September our current base case.