to cut the Bank Rate by 25bp to 4.00% on Thursday 7 August in line with consensus and market pricing.){kind=link}

- We expect the Bank of England (BoE) to cut the Bank Rate by 25bp to 4.00% on Thursday 7 August in line with consensus and market pricing.

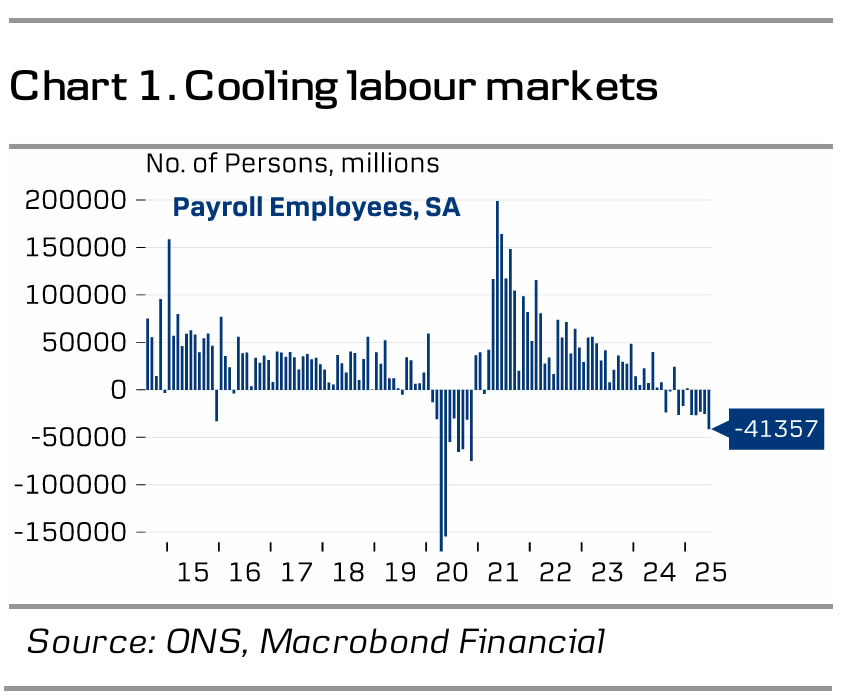

- Data has been a mixed bag since the last meeting with the labour market showing more pronounced signs of cooling, weaker than expected growth but inflation surprising to the topside. We think this supports the notion of further quarterly cuts.

- We expect a muted reaction in EUR/GBP. We stay negative on GBP.

We expect the Bank of England to cut the Bank Rate to 4.00% on Thursday 7 August in line with consensus and market pricing. We expect the vote split to be 6-3 with the majority voting for a 25bp cut and Greene, Mann, Pill voting for an unchanged decision. Note, this meeting includes updated projections and a press conference following the release of the statement.

Overall, we expect the BoE to stick to its previous guidance repeating that a “gradual and careful approach to removing monetary policy restraint remains appropriate“. Since the last meeting in June, data has been a mixed bag. Growth has surprised to the downside with the economy contracting by 0.3% m/m in April and 0.1% m/m in May, on course to undershoot the BoE projections for Q2 2025 of 0.25%. The labour market has shown more pronounced signs of cooling with private sector regular wage growth at 4.9% 3M/YoY in May, lower than the BoE’s projections of 5.2% but remains at elevated levels. Similarly, payrolls have dropped the past months, and the unemployment rate has edged higher to 4.7%. On the other hand, inflation has been stronger than expected and inflation expectations have risen. Headline inflation rose to 3.6% y/y in June with food prices delivering the relative biggest overshoot compared to the MPC’s forecast. On the back of this, we think the MPC is likely to lift the near-term projection for inflation slightly.

BoE call. We expect the BoE to stick to quarterly cuts, leaving the Bank Rate at 3.75% by YE 2025, which is aligned with market pricing. However, we expect the cutting cycle to extend throughout 2026 leaving the Bank Rate at 2.75%. This is more dovish than markets, which prices a bottom of 3.50% a year from now.

Market reaction. We expect a muted market reaction as we expect the BoE to refrain from altering its current guidance. More broadly, we stay negative on GBP. An investment environment characterised by elevated uncertainty and a positive correlation to a USD negative environment, in our view, favours a weaker GBP. Tentative signs of a weaker growth outlook for the UK economy also acts as a headwind for GBP. We therefore expect EUR/GBP to move higher towards 0.89 on a 6-12-month horizon.