{kind=link}

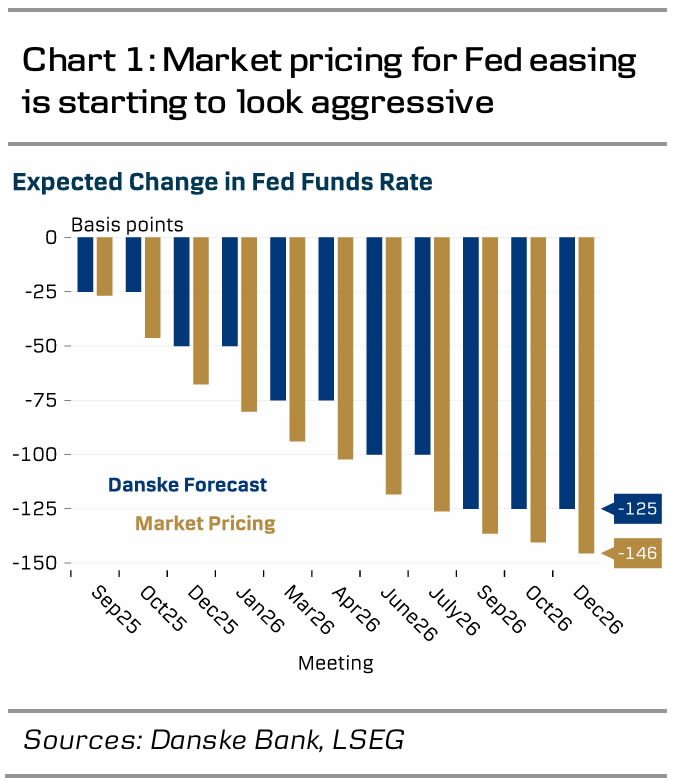

- We expect the Federal Reserve to cut policy rates by 25bp at the September meeting. The market is pricing a slim 5-10% risk of a larger 50bp cut.

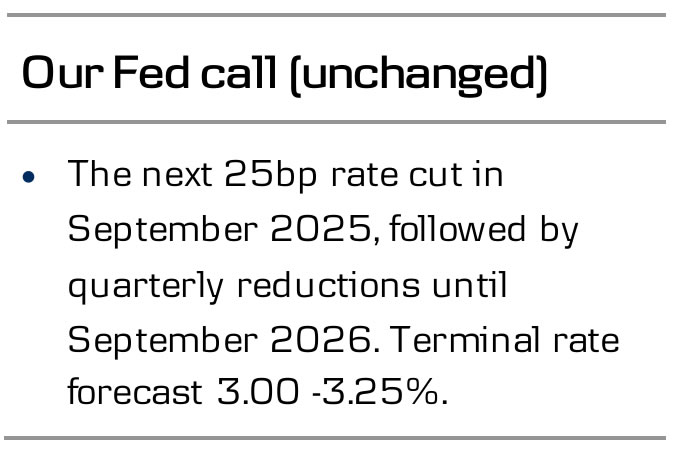

- Updated dots will provide key insight into whether the FOMC majority prefers quarterly or sequential cuts. We still call for only two cuts this year (Sep & Dec) and expect the median dot to signal a terminal rate of 3.00-3.25% by end-2026.

- We see upside risks to short-end USD rates and downside risks to EUR/USD if the majority of participants favour quarterly cuts over sequential reductions.

Markets have flirted with the idea of the Fed delivering a larger 50bp cut at the September meeting after disappointing jobs growth over the summer, but we still think a more gradual approach is better suited for the current environment.

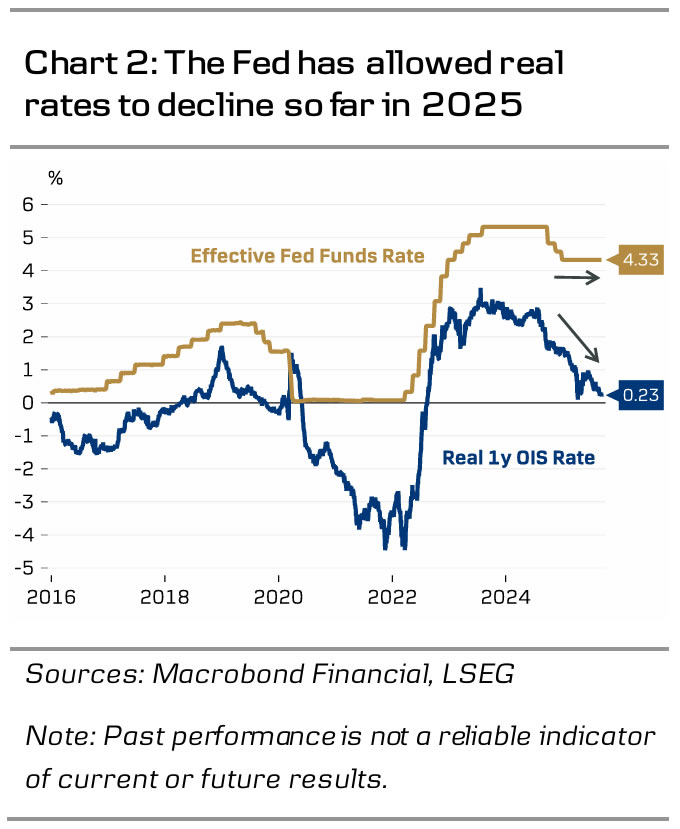

Many of the hawkish arguments that Powell presented in June and July still hold today. Monetary policy is not as restrictive as it was a year ago when the Fed kicked off the easing cycle with a 50bp move. The nominal policy rate is 100bp lower and 1Y real rate is 190bp lower than a year ago, while overall financial conditions have eased tremendously. There is simply less need for additional easing to reach neutral.

Furthermore, while Powell is likely to repeat his earlier view that tariff-driven inflation will remain temporary in nature, the still elevated level of inflation expectations increases the risk of more persistent price pressures. Recent CPI and PPI data showed that tariff costs are making their way through the economy, even if pass-through to consumer prices has so far been limited, see Global Inflation Watch – Tariff pass-through still in progress, 11 Sep.

The updated economic projections, and particularly the rate expectations (or ‘dots’), will provide important insight into participants’ preferences about the pace of future rate cuts. Those calling for only one additional cut this year likely prefer a more gradual pace in 2026 as well, while those calling for two more cuts would likely prefer continuing sequential cuts into early 2026. We think the median terminal rate forecast will remain at 3.00-3.25% – a level we think will be reached by September 2026.

Based on recent commentary, at least governors Waller and Bowman likely prefer more aggressive sequential cuts. Regional Fed presidents Williams, Kashkari and Bostic have favoured a more gradual approach in their recent remarks, though participants have generally refrained from laying out precise rate paths.

The FOMC’s September composition still remains somewhat unclear. Federal court blocked Trump from firing governor Cook based on alleged mortgage fraud. While this was not a ruling on whether Cook had committed wrongdoings or not, and even though Trump has already appealed the decision, it looks likely that Cook will be able to participate in next week’s meeting. The temporary nomination of Stephen Miran is currently being debated in Senate, and while it is likely that Senate will confirm Trump’s pick, it remains unclear whether Miran will be eligible to vote already next week. Confirmation vote has been scheduled for Monday (according to Reuters). In any case, we do not expect Cook’s and/or Miran’s participation to affect next week’s rate decision itself.