Canadian Highlights

- Industries that are highly exposed to the U.S. continue to suffer, with manufacturing and wholesale sales volumes down in August.

- Housing market developments were mixed in September, with home sales declining but housing starts improving. However, performances for Q3 overall were as expected.

- Next week’s CPI inflation and BoC surveys loom large for the upcoming Bank of Canada interest rate decision.

U.S. Highlights

- Alternative data helped fill the void of official releases due to the ongoing government shutdown. The Cleveland Fed’s Inflation Nowcasting model estimated core inflation remained around 3% (y/y) in September.

- The Chicago Fed’s Advance Retail Trade Summary indicated retail & food services sales excluding autos were healthy in September.

- Fed Chair Powell signaled that the central bank could soon reach a point where it may stop reducing the size of its balance sheet, also known as quantitative tightening.

Canada – Soft Data, Subdued Economy

If not for equities, one could easily make the case that caution dominated the minds of investors this week. Oil prices continued their slide, with WTI dropping about $2/bbl on concerns of a global supply glut and rising trade tensions between the U.S. and China. This is bad news for Canadian oil exporters, although the upside is that inflation will be pressured lower in October, freeing up Canadians to spend elsewhere. Canadian bond yields were also lower during the week (10-year yield was down about 8 bps as of writing), echoing the trend in their U.S. counterparts and reinforcing the theme of cautiousness. However, stock markets ran somewhat against the grain this week, after a brief trip into the red the week prior. This time, its was mining companies (benefitting from record highs in gold, which itself is a classic sign of cautiousness) that helped the TSX edge higher (as of writing).

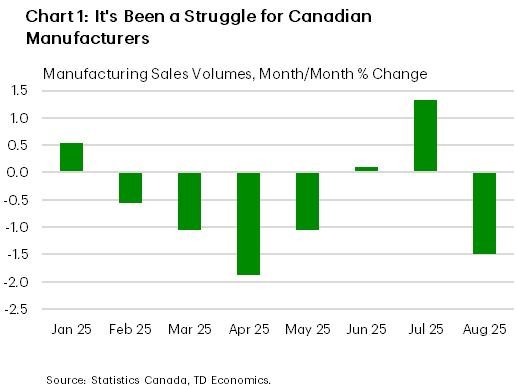

This week offered fresh evidence that industries tied to the U.S. continue to suffer. Canadian manufacturing sales volumes fell 1.5% month-on-month (m/m) in August, erasing gains made the prior two months (Chart 1). Sales were driven lower by tumbling shipments of transportation equipment (cars, aerospace products). Manufacturing was also dealt a fresh blow this week as Stellantis announced that it would be shifting production of the Jeep Compass originally planned for their currently idled plant in Brampton Ontario to the U.S. Meanwhile, wholesalers – also highly exposed to the U.S. market – had a rough August, with wholesale sales volumes down 2.7% m/m.

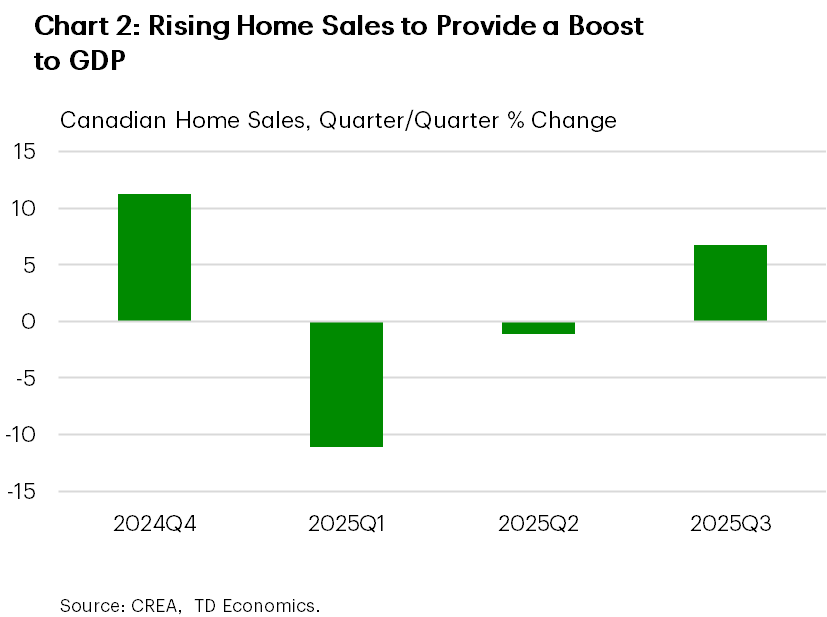

This week also painted a mixed picture of Canada’s housing markets in September. Home sales declined last month, marking the first drop since April, after the market had bounced back from very early 2025 lows. Housing starts, meanwhile, increased 14% m/m in September after August’s large drop. For the third quarter overall, home sales were up 7% while starts dropped 3%. Both results were generally in line with our latest forecast, where rising sales activity would enable residential investment to make a positive contribution to Q3 GDP growth (Chart 2). However, September’s weak sales performance suggests some softening in momentum heading into Q4. Our current view is for a modest, gradual rise in home sales unfolding through next year, although housing starts are expected to trend lower amid slow population growth.

All in, data this week reinforces that Canada’s economy continues to suffer under the weight of the trade war. It’s not all bad news, as last week’s employment report was solid, but the overall picture is one of an economy that is muddling along at a well-below trend pace. For the Bank of Canada, these data probably didn’t move the dial much in terms of their thinking on rates. But, next week’s BoC Business Outlook Survey and CPI inflation report will be the key final pieces of puzzle before the next interest rate decision on October 29th. The Bank of Canada will be looking for confirmation that the inflation backdrop is benign to support a rate cut, while businesses’ outlook in the face of tariffs will play a key role in their thinking on future demand.

U.S. – Reading the Tea Leaves Amidst the Data Fog

This week’s U.S. economic landscape remained shrouded in fog due to the lack of official data amidst the ongoing government shutdown. If it continues until Monday, it will be the third longest in history. In the official data drought, focus has shifted to alternative indicators, particularly from the Federal Reserve, which is still operating during the shutdown. US-China trade tensions ebbed and flowed, while concerns surrounding regional banks made a comeback, weighing on equity markets. Still, equities managed to eke out some gains, with the S&P 500 up 1% from last Friday’s low. Bond yields declined amid uncertainty and expectations of further monetary easing. Notably, the 10-Year Treasury yield fell below 4% and is now hovering near last year’s level.

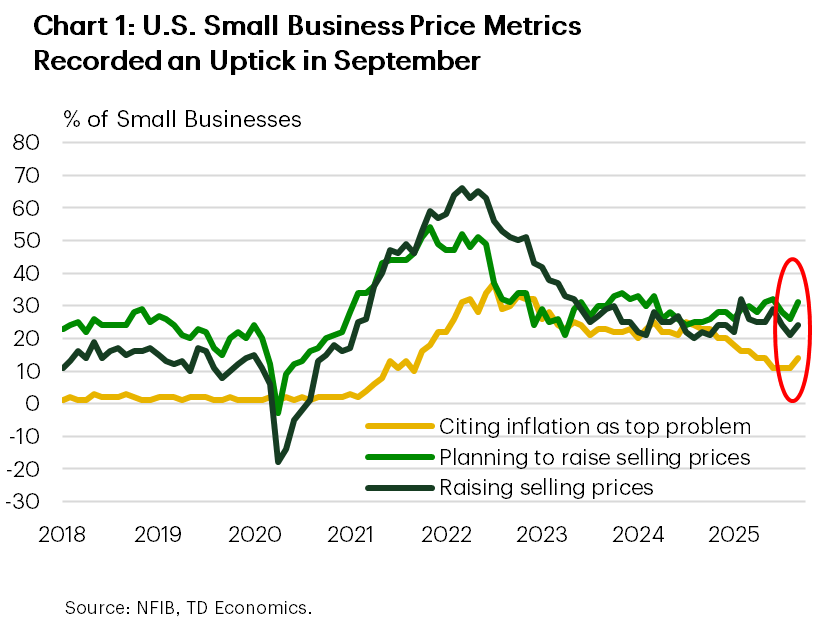

In the absence of the CPI report, alternative inflation indicators are sending conflicting signals. The Cleveland Fed’s Inflation Nowcasting model estimated core inflation at 0.26% month-over-month in September, suggesting year-on-year core inflation remained near 3%. The lack of acceleration would support another Fed rate cut amidst a deteriorating labor market. However, the Fed’s Beige Book reported further price increases, with several districts noting “faster input cost growth due to higher import prices and rising costs for services like insurance, health care, and technology”. The NFIB’s small business survey also showed moderate upticks in its price metrics (Chart 1). The CPI report is set to be released next week, which should help clear some of the fog.

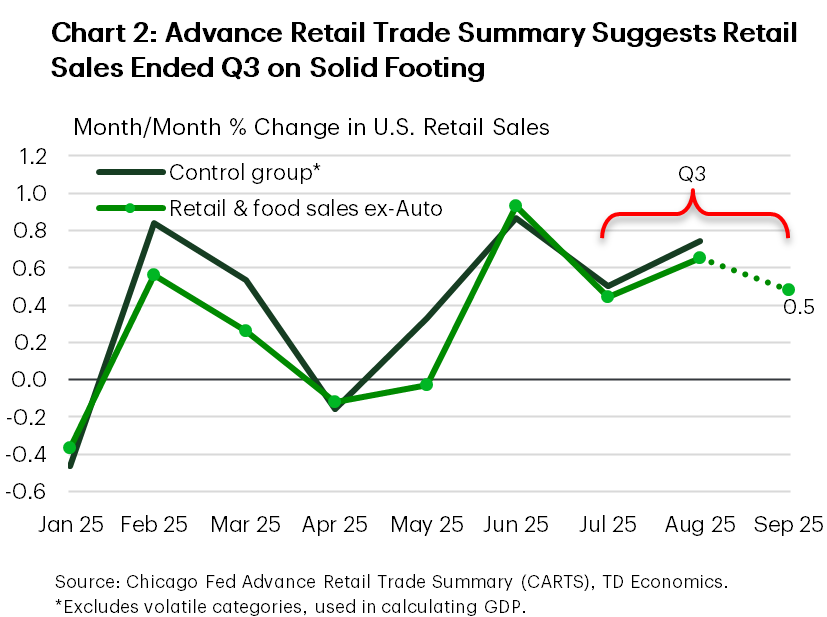

The September retail sales report is also delayed, but the Chicago Fed’s Advance Retail Trade Summary (CARTS), which tracks weekly sales, offers some insight. CARTS indicates that retail & food services sales excluding autos rose by 0.5% in September, suggesting a solid finish to the third quarter (Chart 2). However, given ongoing uncertainty and other consumer challenges, momentum is expected to ease in the fourth quarter. The Beige Book echoed this, noting that overall consumer spending, especially on retail goods, trended down in recent weeks, with auto sales being the main exception.

On the employment front, the Beige Book described labor demand as “subdued” and employment levels as “largely unchanged”. More employers reported lowering headcount through layoffs and attrition, citing weak demand, high uncertainty, and, in some cases, increased investment in AI. Layoffs were mentioned 14 times, up from 6 previously. NFIB employment metrics also pointed to a weak hiring trend among small businesses in September.

Fed Chair Powell reiterated recent messaging and placed more emphasis on labor market risks in a speech this week, supporting additional easing. Powell also signaled the central bank could soon stop reducing the size of its balance sheet. While he provided no set timeline for the end of quantitative tightening (QT), he stated “we may approach that point in the coming months,” noting early signs that liquidity conditions are gradually tightening.

Reading the tea leaves, labor market risks remain the key focus. As such, the Fed is likely to deliver another rate cut at the end of this month. The signal that QT may soon end further reinforces the Fed’s dovish stance.

{kind=link}