- We expect the Bank of England (BoE) to cut the Bank Rate by 25bp to 3.75% but we recognise it is a close call.

- We see a clear, although narrow, path to a 5-4 decision for cut.

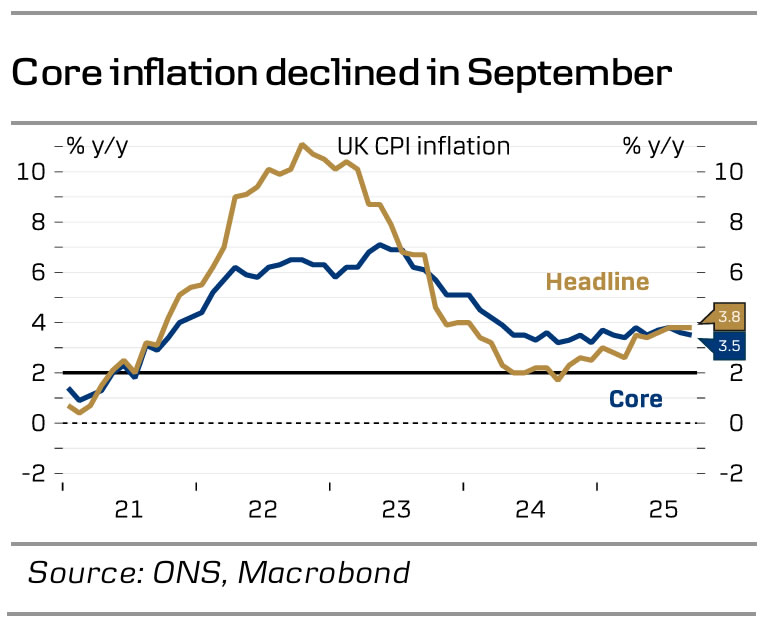

- Since the last meeting, the labour market has continued to cool but the steepness of job losses is not too worrying. Softer inflation data keeps the door open for further easing.

- If we are right, we expect GBP to weaken, and UK yields to drop on announcement.

We expect the BoE to cut the Bank Rate to 3.75% on Thursday 5 November. This is a non-consensus call, and markets are also pricing only about 30% for a cut. We see chances slightly above 50%. Recent data has confirmed that the cooling of the labour market continues but not at an alarming pace. Job loss accelerated although at a moderate pace of 10k in September and previous job losses were revised down. Consumer demand remains moderate with retail sales at 1.5% y/y in September. Both indicating no rush to cut rates.

On the other hand, CPI inflation came in lower than the 4.0% y/y consensus and BoE forecast in September at 3.8%. It was largely driven by lower-than-expected service inflation, which continues to be the main headache for the BoE. Following the CPI release, markets priced in close to 50-50 for a November cut but later retracted.

We see a clear, although narrow path, to pave the way for a cut at the November meeting. Four members of the MPC, Lombardelli, Pill, Mann and Greene will very likely be voting for an unchanged decision. Dhingra and Taylor voted for cut in September and will almost certainly repeat that. Deputy governor Ramsden has been in the dovish camp for long and he is likely to join Dhingra and Taylor. That leaves governor Bailey and deputy governor Breeden (until this date aligned at all meetings) with the deciding votes.

BoE call. With the economy holding up and inflation still quite sticky above target, we expect the BoE to cut rates for the last time in February leaving the Bank Rate at 3.50%. The Autumn Statement is a big joker in all of this. If the Labour government comes through with fiscal tightening as we expect, it will support our call for cutting rates quicker than what is priced in by markets, see also Research UK – Autumn Statement will be key for UK markets.

Market reaction. In our base case of a 25bp cut on Thursday, we expect GBP to weaken on announcement and UK yields to move lower. More broadly, we stay negative on GBP FX as we see the relative growth outlook between the UK and the euro area as GBP negatives. This is further amplified by divergence in the fiscal policy outlook with UK fiscal policy set to be tightened in the Autumn. Additionally, a global investment environment characterised by elevated uncertainty and a positive correlation to a USD negative environment, in our view, favours a weaker GBP. We expect EUR/GBP to trend higher the coming year, targeting the cross at 0.89 in 6-12 months.

{kind=link}