{kind=link}

- The RBNZ cut the OCR by 25bps to 2.25%. The decision was made following a 5 – 1 vote, with one MPC member voting to hold the OCR at 2.5%.

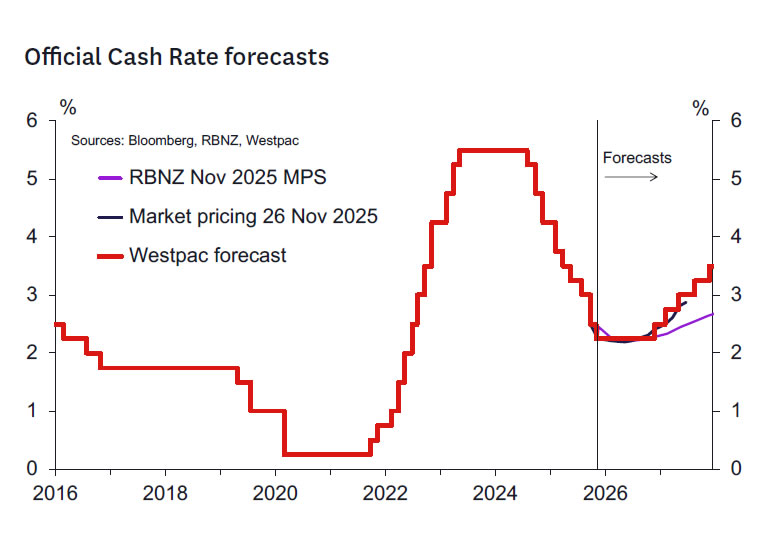

- The RBNZ’s OCR forecast profile was revised down as expected and now shows a terminal OCR of 2.20% (in Q2 2026), down from 2.55% previously.

- The RBNZ’s forecasts imply a first OCR hike around the middle of 2027, with the OCR to gradually move up towards 3% (the RBNZ’s estimated neutral rate) by the end of 2028.

- The RBNZ is presenting a neutral outlook for the OCR looking forward. The MPC retains flexibility to respond to incoming data, and is not drawing a firm line under the easing cycle just yet.

- Westpac expects no further cuts in the OCR. Our baseline forecast is that the OCR will begin a gradual move higher from late next year.

Key take out: OCR cut 25bps, RBNZ signals a neutral bias for February and perhaps beyond.

As widely expected, the RBNZ cut the OCR by 25bps to 2.25%. The decision was reached following a 5 – 1 vote, with one MPC member voting in favour of leaving the OCR at 2.5%.

The general tone of the Monetary Policy Statement seems more neutral than we expected. For example, there was no consideration of a 50bp cut, and one MPC member voted for no change in the OCR. The RBNZ’s assessment that the economy is picking up is perhaps a little more confident that we might have thought. Fixing the March 2026 OCR average at 2.25% sends a neutral bias for the February 2026 meeting. Glenn Turner was definitely opening the batting for the MPC in this innings!

As expected, the RBNZ’s projected track for the OCR was revised lower:

- The terminal OCR is 2.20% (in Q2 2026), down from 2.55% in the August MPS.

- The projected OCR for Q4 2026 was revised to 2.28% from 2.62% previously.

- The projected OCR for Q4 2027 was revised to 2.65% from 2.80% previously.

- The RBNZ assumes the OCR reaches 2.90% in Q4 2028 (the final quarter of the new forecast).

According to the RBNZ, the most important drivers of the reduction in the OCR track were a larger degree of spare capacity in the economy this year than assumed previously (reflecting the weak Q2 GDP outcome) and a lower outlook for export prices (due to recent falls in dairy product prices). The lower exchange rate supports exporter earnings and leans against disinflation in the short term.

The RBNZ is presenting a neutral, but data-dependent outlook. The Governor noted some slight downside risk to the OCR in the short term, but upside risk in the medium term. The Governor noted that the OCR is now at stimulatory levels and should support growth in time. Up to now, the RBNZ has been less clear about whether interest rates are at stimulatory levels.

The overall implication is that the MPC is now ready to send the nightwatchman in to see the innings through for the foreseeable future. The new Governor can reassess the situation next year in light of the data to come.

Notable quotes.

Some notable quotes from the press statement and Statement of Record were:

“Economic indicators are recovering, and economic activity is expected to strengthen through 2026.” “Risks to the inflation outlook are balanced.”

“Committee members discussed an improvement in near-term indicators of economic activity from their lows in the June quarter, suggesting a return to modest GDP growth in the September quarter. Feedback from recent business visits also suggests that, while activity remains weak, demand has stabilised.”

“Some members highlighted the risk that continued caution on the part of households and businesses could further slow the recovery in domestic demand, which could see inflation fall below the target midpoint. Conversely, other members highlighted the possibility of a faster recovery if house prices and household spending increase more quickly than assumed given lower mortgage rates, leading to more persistence in medium-term inflation pressures.”

“Members noted that tariffs have had less impact on the global economy than initially expected, reflecting the imposition of lower tariff rates than originally envisaged, inventory management, and adjustments in global supply chains… The Committee still expects trade barriers to weigh on global economic activity and to have a modest disinflationary effect on New Zealand.”

“The Committee discussed the risk that unsustainable fiscal dynamics and increased politicisation of central banks globally could create the conditions for higher and more persistent inflation.”

“The case for a further reduction in the OCR emphasised significant excess capacity in the economy. This provides confidence that medium term inflation will return to, and remain around, the target mid-point. The economic recovery is at an early stage, and the inflation outlook provides scope to place more emphasis on avoiding unnecessary volatility in output and employment. With this context, retention of the easing in overall monetary conditions delivered to date would support an enduring recovery in economic activity.”

“Future moves in the OCR will depend on how the outlook for medium-term inflation and the economy evolve.”

Westpac’s OCR call.

We continue to expect 2.25% to mark the nadir of the easing cycle. The RBNZ looks like it has a neutral bias looking forward and is certainly not signalling any intention to cut the OCR in February. Of course, much could change between then and now. Hence, we continue to expect the RBNZ to maintain a flexible data-dependent approach. We agree that the current OCR, left long enough, should be sufficient to support the recovery in the economy.

The timing of the return of the OCR to higher, more neutral levels will depend on the pace of the eventual recovery. Hence while we continue to see the first hike as occurring in December 2026 (likely after the 2026 General Election), there are two-sided risks to that call. Should the economy pick up relatively quickly, the normalisation of the OCR could come before the election, closer to the middle of 2026. A disappointing recovery could mean the OCR on hold for longer.

The exchange rate has moved a touch higher as markets likely expected a more dovish outlook than seen today. More generally, we suspect that the New Zealand dollar will remain weak against most currencies until such time as markets turn away from the risks of a lower OCR and consider the timing of the tightening cycle. It will likely be some time before we get to that position.

RBNZ forecast detail.

The RBNZ’s updated forecasts align broadly with our own assessment.

The economy is starting from a weaker position than the RBNZ anticipated back in August. That’s due to the much weaker than expected June quarter GDP result. Like ourselves, the RBNZ thinks that result likely overstated the degree of weakness in activity. Even so, economic conditions were soft through the middle part of the year, and the economy has more spare capacity than the RBNZ anticipated (i.e., a lower output gap). And even with lower interest rates, that spare capacity is expected to dissipate only very gradually.

That lingering spare capacity has reinforced the downward pressure on the RBNZ’s forecasts for domestic inflation. This is an area where we think the RBNZ could be surprised on the upside. The RBNZ has acknowledged the strength in the prices for items like council rates, but expects this to ease. In contrast, we anticipate such pressure will be a bit more enduring.

Nevertheless, we agree with the RBNZ’s more general assessment that spare capacity in the economy will see inflation dropping back over the year ahead.

The RBNZ’s statement noted early signs that the economy is starting to turn. Consistent with such indicators and the large fall in interest rates over the past year, we think that domestic demand will pick up a bit faster than the RBNZ. However, much of that increase in demand will be met by increased imports.

Key things to watch ahead of the RBNZ’s 18 February 2026 Review.

The next RBNZ policy review will take place on 18 February 2026. Given the longer than usual break until the next meeting, there will be a significant number of key domestic economic data releases ahead of that meeting. Indeed, the RBNZ will receive a new round of all the top-tier quarterly indicators, and so there is plenty of scope for outcomes to drive a different outcome to that currently projected by the RBNZ. The most important releases are:

- The Q3 GDP report (18 December): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum. The RBNZ’s forecast of 0.4% growth is in line with our own view. The Q3 release will also include a range of revisions to the historical data, which could have a bearing on the RBNZ’s assessment of the economy’s spare capacity.

- The Q4 QSBO survey (13 January, TBC): The focus will be on indicators of spare capacity and cost/inflation pressures. It will also be interesting to see to what extent hiring and investment indicators are lifting as easy monetary conditions continue to transmit through the economy.

- The Q4 CPI (23 January) and January Selected Price Indexes (17 February): With headline inflation currently at the top of the RBNZ’s target range, the focus will be on whether the CPI is evolving in a manner consistent with the RBNZ’s forecast that it will quickly move back towards the target midpoint over the coming year.

- The Q4 labour market survey (4 February): Developments in both the unemployment rate and labour costs will be compared against the RBNZ’s updated estimates, while measures of labour input will provide some insight into how GDP might have fared during the quarter.

In addition to the above, key monthly activity indicators such as the BusinessNZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest, as will developments in retail spending and housing indicators (albeit the latter tend to be difficult to read given that the housing market typically goes somewhat quiet over the holiday period). The Government’s Half-Year Economic and Fiscal Update and Budget Policy Statement (16 December) might also contain information bearing on expectations regarding the future stance of fiscal policy (of particular interest given the seemingly tight General Election that looms later next year).

Finally, the other factor that will have a bearing on the next policy decision will be the arrival of the new Governor Anna Breman, who takes up her role next week. In addition, the departure of current Governor, Christian Hawkesby, will maintain a vacancy on the MPC. That vacancy may be filled by the time of the February MPS meeting, possibly by a temporary appointment pending the appointment of a new Deputy Governor.