Canadian Highlights

- Canada’s job market defied expectations again in November, pushing the unemployment rate down to a 16-month low.

- The labour market is demonstrating some resiliency, but slack still exists, and the short-term trajectory is marked by significant uncertainty.

- The Bank of Canada will make their final rate announcement of the year next week. We expect the Bank to hold rates steady at 2.25%.

U.S. Highlights

- Real consumer spending was flat in September, ending the third quarter on a soft note. Consumption for the third quarter was up 2.7% (q/q annualized).

- The Fed’s preferred inflation gauge – the core PCE deflator – rose by 0.2% month-on-month in September, as expected. That is still above the Fed’s target at 2.8% year-on-year, but down slightly from 2.9% in August.

- Combined with somewhat soft employment data in November’s ADP report, the Fed looks set to check off markets’ wish list for a rate cut next week.

Canada – Jobs Bringing on the Winter Heat

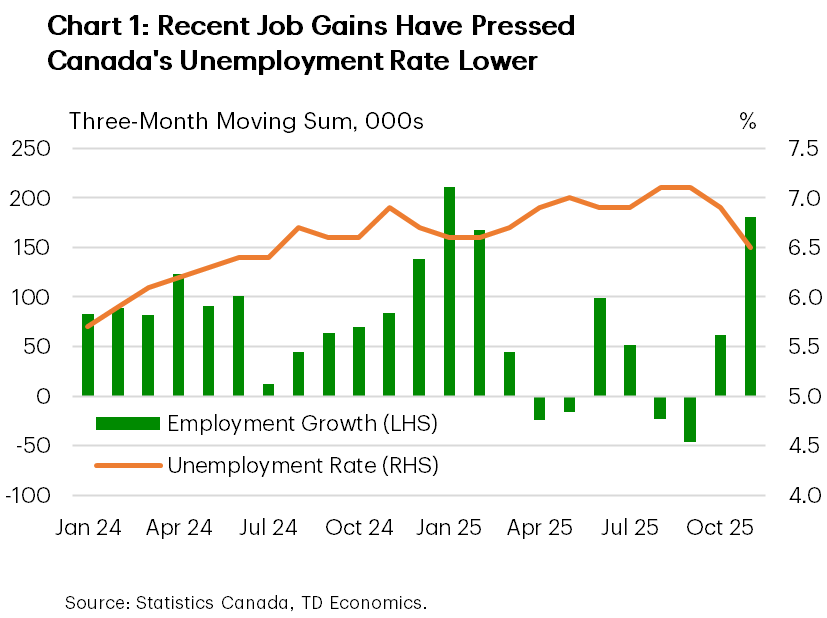

An update to Canada’s labour market was the sole event in an otherwise quiet start to December. And unlike the recent weather, the data brought some heat. Forecasters were caught flat-footed as Canada’s economy generated 54k jobs, against expectations for modest employment losses. Alongside a contraction in labour force growth, the national unemployment rate legged down to 6.5%, putting it back in line with mid-2024 levels. Other details were more mixed but upbeat on the margin. Part-time jobs drove the entirety of the gain, while job growth was concentrated in the private sector. To add, wage growth and hours worked both ticked higher on the month. In the wake of the news, the Loonie gained to 72 cents/USD, while yields are up a few basis points (bps), continuing their march higher on the week.

So, what do we make of all this, especially given the Labour Force Survey (LFS) has been particularly noisy in recent months? On one hand, Canada’s labour market is certainly displaying some resiliency. Job creation since tariffs took effect in March has averaged around 16k, roughly in line with historical average steady-state employment gains. That’s a great outcome considering the economy is facing one of the largest external trade shocks on record. What’s more, the Canadian economy gained a staggering 180k jobs over the last three months, which has helped put the unemployment rate on a downward trend (Chart 1).

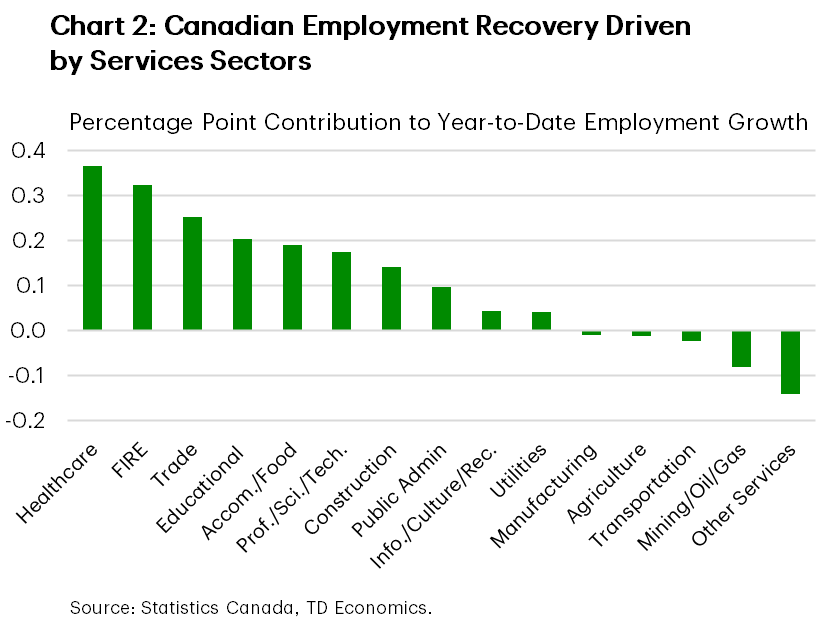

On the other hand, we are cautious to declare this a victory. Job conditions are showing signs of improvement, but the jobless rate is still elevated, and Canada’s payroll survey (SEPH) is painting a much weaker picture of labour conditions, albeit in data only up to September. The composition of employment gains this year has also been skewed, with almost 90% of job creation coming from the services sector (Chart 2). This result is unsurprising as the goods side of the economy is facing more of a disproportional hit from trade-related headwinds, but it still creates a wedge in the employment recovery narrative.

The Bank of Canada’s (BoC) will hold its final policy decision of the year next week. Prior to November’s employment report, it was already expected that interest rates would stay unchanged, and today’s update confirms this view. More important is how Governing Council guides the outlook. They are likely to recognize progress in employment while highlighting ongoing slack in the labour market and considerable uncertainty, especially as Canada and the U.S. enter complex USMCA renegotiation talks. We also expect the BoC will reaffirm that inflation will continue moderating. All told, we expect the Bank to maintain its current stance through 2026 and continue to look for signs that a sustained economic recovery is in the works.

We will finally get an update on how Canada’s exports are faring in the face of U.S. tariffs, as Statistics Canada will publish September’s international trade data on December 11th. Trade data was delayed due to the U.S. government shutdown, with October and November’s data to be released in January.

U.S. – Fed to Play Santa, Cut Policy Rate

Markets are convinced that the Fed will deliver an early holiday gift – a rate cut – next week. Odds of a December cut have hung near 90% ever since shifting up in late November, following support for more easing from Fed Presidents Williams (NY) and Daly (San Fran.). Economic data out this week, while mixed, did not perturb that balance. Equities managed to trek modestly higher, with S&P 500 up 1.1% from last week’s close.

September’s personal income and spending report provided a snapshot of spending and inflation trends before the government shutdown. Spending was flat in real terms in September, ending the third quarter on a soft note. Consumption for the quarter was up 2.7% (q/q annualized) – below expectations but still an improvement from 2.5% in the second quarter. September provides a soft handoff to the fourth quarter, which coupled with the government shutdown, slowing job growth, and weak consumer confidence, suggests spending will slow further at the end of the year. Early data from Thanksgiving weekend suggests holiday shopping was healthy but likely grew at a pace slightly below that of last year. Online sales continued to lead the way, with Cyber Week spending up nearly 8% year-over-year (y/y) according to Adobe. In-store gains were softer, with closely watched indicators pointing to growth in the low single-digits. AI tools helped boost retail site traffic, while a growing Buy-Now-Pay-Later (BNPL) trend also played an important role in propping up spending.

Core PCE inflation rose 0.2% month-over-month (m/m) in September, and 2.8% in y/y terms – a modest easing from 2.9% in the prior two months. The ISM services price index recorded a notable pullback in November – marking a modest positive post-shutdown signal with respect to inflationary pressures. Nonetheless, Cleveland Fed Inflation Nowcasting puts core PCE at 0.23% (m/m) for both October and November, 2.8% and 2.9% in y/y terms respectively – still well above target.

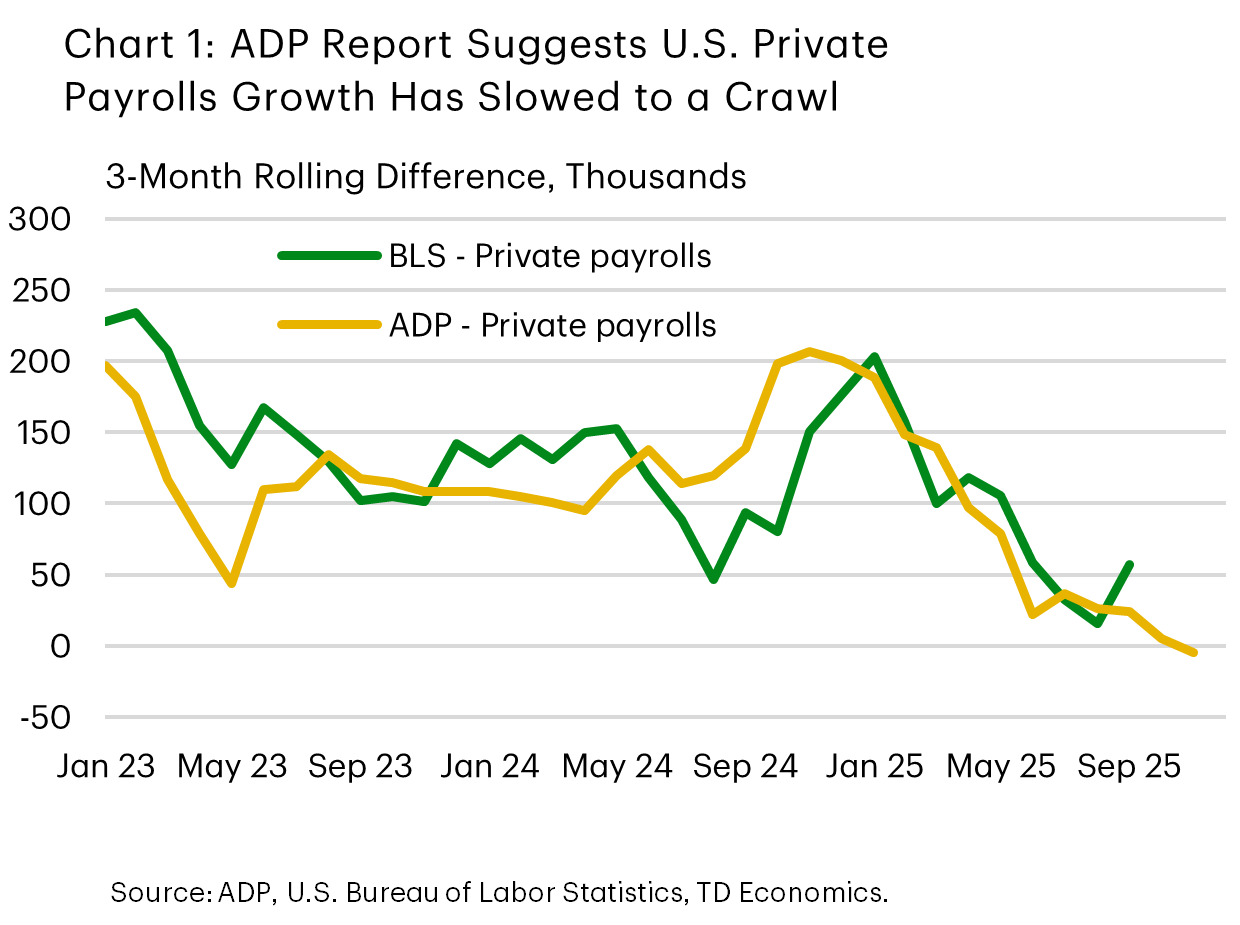

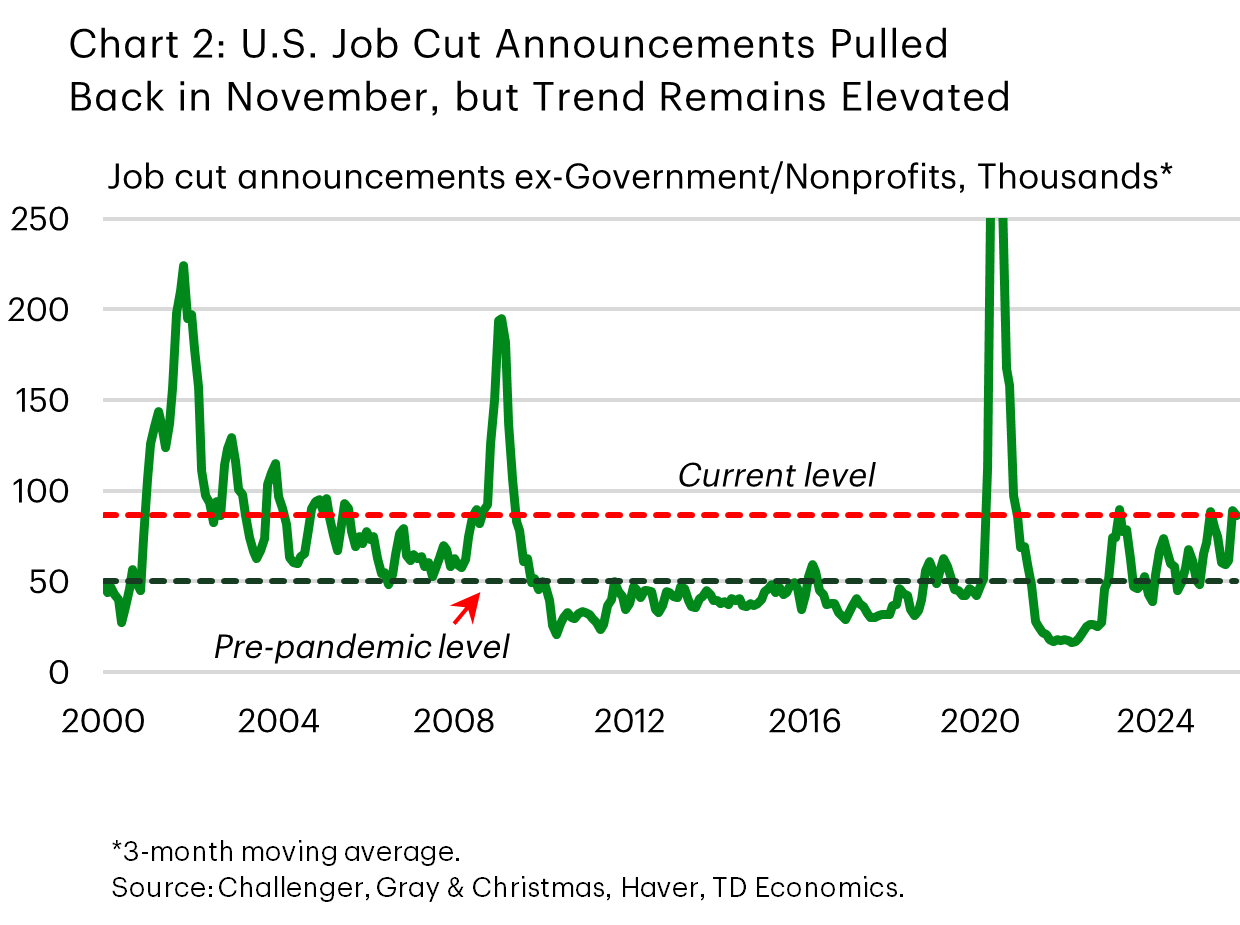

Employment data was mixed. Initial jobless claims dropped to a three-year low of 191k at November’s end. The Thanksgiving holiday may have distorted the data. But even prior to that last week, initial claims were still trending lower. Conversely, the ADP report showed private payrolls fell by 32k in November. Its three-month average, which is more closely aligned with the BLS equivalent, turned slightly negative too (Chart 1). Job cut announcements, meanwhile, also pointed to continued challenges. Layoff announcements in November were cut in half from their October tally, coming in at 71k. But even when looking past the weakness in the government sector, the trend in layoff announcements remains elevated (Chart 2). Overall, markets seemingly expect the Fed to focus on signs of labor market softness and maintain a cautious policy stance.

Our reading is that the Fed won’t disappoint market expectations next week. But in the New Year, the bar for additional cuts may be higher. Having delivered some insurance cuts, the Fed will likely take time to digest delayed economic reports and carefully assess post-shutdown data to form a clearer picture of the economy’s health.

and Daly (San Fran.). Economic data out this week, while mixed, did not perturb that balance. Equities managed to trek modestly higher, with S&P 500 up 1.1% from last week’s close.){kind=link}