{kind=link}

We will now turn to a more technical look into the US curve, a 10-Year Bond chart to see what’s going on behind the pricing for tomorrow’s meeting, and provide a few more scenarios depending on the rate cut path.

More particularly, with the 25 bps cut being a quasi-certainty, we will provide potential scenarios on if the cut is hawkish or dovish and a few potential reactions.

A first move to signal in Markets, is the recent move higher in US treasuries across the curve.

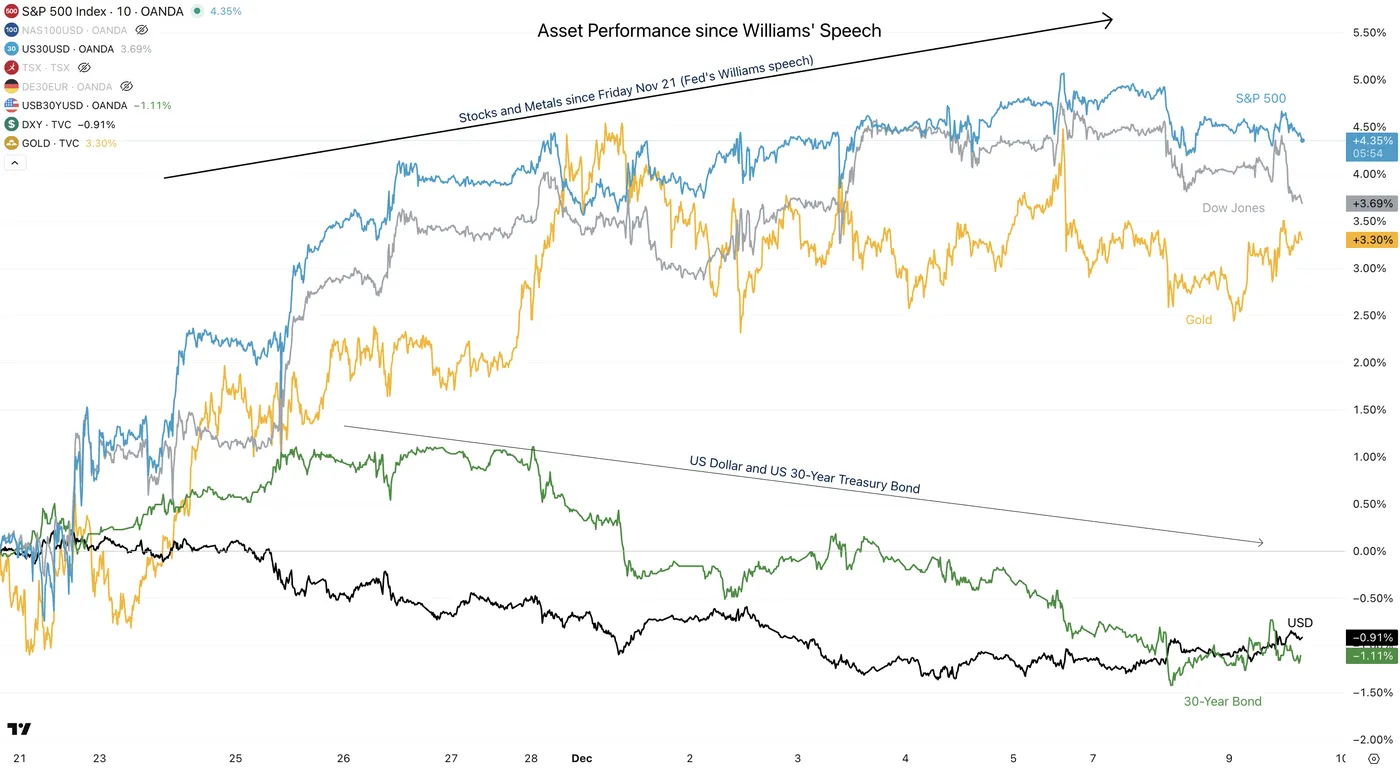

Mentioned many times across our analyses on MarketPulse, the speech from NY Fed’s Williams, a very influential speaker, affected Markets on a large scale:

Asset Performance since Williams’ Speech – Source: TradingView

Counter-intuitively, the speech that re-introduced possibilities of lower rates (which you can find right here) led a huge rebound in Stock Markets and Metals, but similarly preceded a move between +15 bps to +20 bps in US treasuries.

But why?

US 10-Year Bond with 10Y Yield underlay – December 9, 2025 – Source: TradingView

Never forget the sell-the-news effect – At least for the bonds!

The reasoning behind this move is a microcosm of the 2025 trend: A fear of an influenced Federal Reserve, which may fast-forward its rate-cut cycle at the cost of their data-dependency–or even their independence!

As explained in our recent pre-FOMC analysis, the 25-bps move could be one done with a blind eye – most of the data released throughout the past month is data dating back to September, such as the PPI and Retail Sales data (which corroborated a slowdown).

However, at the same time, more actual data also sent mixed signals, particularly regarding Labor – Weekly Jobless Claims came in at the lowest level since September 2022 just a week ago, while ADP Private Payrolls showed a regressing picture.

Until now, the Fed had been remarkably resilient about taking preemptive decisions without a clear consensus on why to hike or cut – and this shift in perspective also comes amid still uncertain tariff-led inflation outlooks.

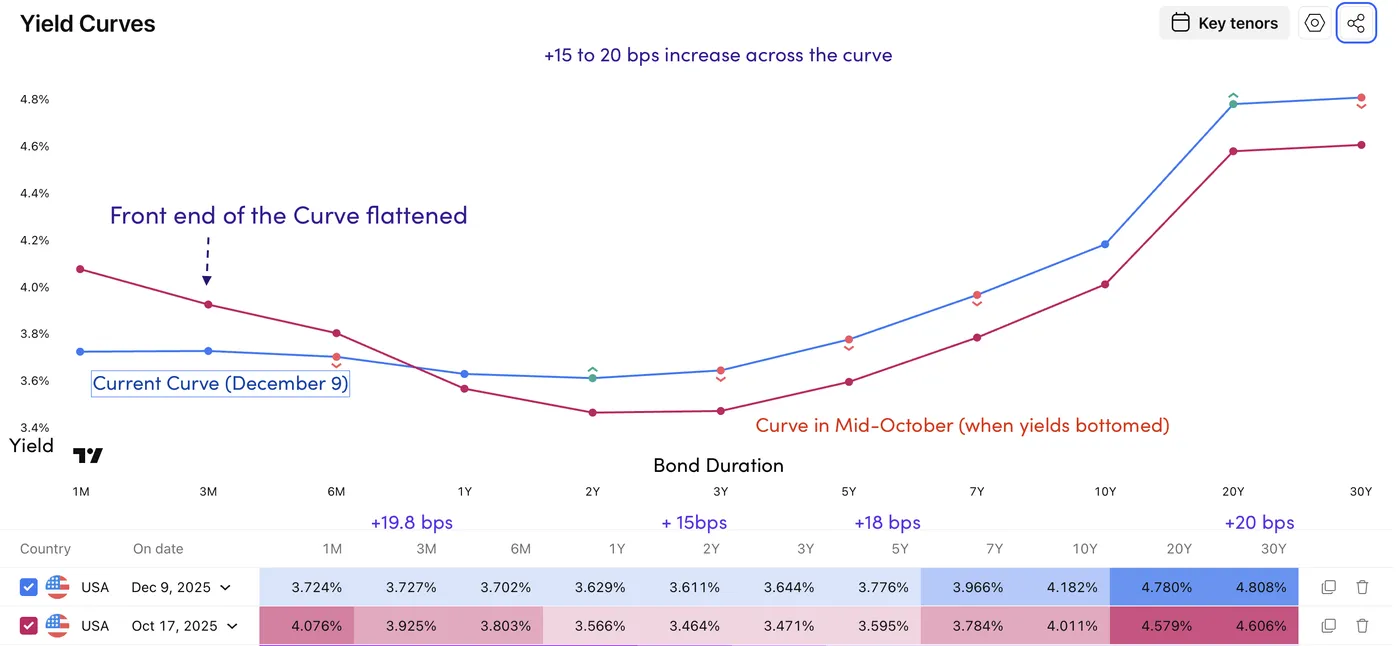

The US Curve: Mid-October vs Today – A 15 to 25 bps increase throughout all durations

The Greenback falling at the same time as yields rising indicates an increased premium for holding US debt.

Many words to describe the same phenomenon: The Debasement Trade.

If you haven’t heard about this term, you can find a stellar definition right here. To summarize, it’s a financial trend shifting away from fiat currencies and governmental assets to focus on finite assets, such as Stocks, Cryptocurrencies, and Metals.

Coming back to the curve picture from above, the front-end flattened quite aggressively, implying Rates staying put for a longer-while after this cut.

Mid-2026 Pricing: 50% odds of a 3% Neutral Rate – Source: TradingView

This takes us to our expectations for tomorrow:

Scenarios and probabilities:

A hawkish cut (70% chance)

This is the base case for tomorrow’s decision (in my opinion).

Powell should indicate a risk-management move after the streak of negative private payrolls data combined with a not-aggravating inflationary picture.

To balance out these words, expect the Fed Chair to point out to a blinded Fed due to the Bureau of Labor Statistics closure and delayed data, particularly for NFP.

Reactions in Major assets

- Upcoming rate cut probabilities decrease to price a pause in the waiting for more data

- The US dollar maintains its ongoing consolidation range (between 99.00 to 100.00 on the Dollar Index)

- Stock Indexes correct due to their ecstatic post-Williams repricing

- Short-end yields shoot higher while long-end yields stay put (Harsh bear flattening)

- Metals correct slightly

A dovish cut (10% chance)

Jerome Powell folds and makes extensive mentions on the private labor market while reducing mentions of inflation.

Reactions in Major assets

- Rate cuts get front-loaded (moved forward) aggressively but leaves VERY volatile future pricings

- The US Dollar falls off a cliff and goes to retest the yearly lows

- Stock Indexes flash to new all-time highs but may find struggles as Fed Independence doubts rage back

- Short-end yields shoot lower while long-end yields shoot higher (Strong steepening)

- Metals explode to new all-time highs and keep running higher

A dovish pause (20%)

The Fed decides to hold their breath due to a lack of data but keep a strong option on rate cuts in the short-term.

This one is the most tricky.

Most participants expect a cut, but this would quickly shift the current pricing:

Reactions in Major assets

- 2026 Rate cuts get front-loaded on a smaller extent

- The US Dollar rallies to hold above/close to the 100.00 level.

- Stock Indexes see VERY volatile swings and form a large range

- The curve stays put, long-term yields go lower (small Bull flattening)

Metals correct slightly

This article wasn’t the most common, but I hope it will be instructive.

Safe Trades!