concluded its final meeting of the year by keeping its key interest rate at zero, and it will continue to charge a small fee ($0.25$ percentage point) on bank deposits that exceed a certain limit.){kind=link}

Asia Market Wrap – Nikkei Struggles, Ends the Day Down 0.9%

The Nikkei finished lower on Thursday, primarily because of a large drop in SoftBank Group shares. SoftBank’s decline mirrored the steep fall of the US tech giant Oracle, which disappointed investors by predicting sales and profit below what Wall Street analysts expected.

Although the Nikkei briefly rose by 0.5% earlier in the day, it closed down 0.9% at 50148.82. The broader Topix index also fell by 0.94% after opening at a record high.

SoftBank Group was the biggest drag, plummeting 7.69%. Other Japanese technology companies also lost ground, including Tokyo Electron (down 1.57%), Shin-Etsu Chemical (down 3.94%), and the robot maker Fanuc (down 2.19%).

Even bank stocks, such as Mizuho Financial Group and Sumitomo Mitsui Financial Group, gave up their initial gains and finished lower.

Swiss National Bank Hold Rates at 0%

The Swiss National Bank (SNB) concluded its final meeting of the year by keeping its key interest rate at zero, and it will continue to charge a small fee ($0.25$ percentage point) on bank deposits that exceed a certain limit.

The bank also stated it is prepared to step into the foreign exchange markets if necessary. Inflation in Switzerland is currently very low, falling to 0.0% in November (from 0.2% in August), mainly because of cheaper hotel stays, rent, and clothing.

Looking ahead, the SNB predicts inflation will remain low, gradually increasing to 0.2% in 2025, 0.3% in 2026, and 0.6% in 2027. Globally, economic growth was better than expected in the third quarter of 2024 despite trade conflicts, though risks from US tariffs and uncertain trade policies remain.

Within Switzerland, the economy actually shrank in the third quarter, largely due to a decrease in pharmaceutical exports to the US after an earlier surge, but other sectors like manufacturing and services saw minor improvements.

The SNB expects the country’s economy to grow by just under 1.5% in 2025, slowing to about 1% in 2026, which may lead to a slight rise in unemployment as the economy cools down.

European Session – European Shares Edge Lower, Delivery Hero Down 5%

European stock markets were relatively quiet on Thursday, seeing a small dip overall. The main reason for the decline was the poor forecast from the American cloud company Oracle, which caused technology stocks to fall. This negative news overshadowed the relief felt after the US Federal Reserve made comments that were less aggressive about future interest rate hikes than investors had anticipated.

The general European STOXX 600 index, along with major markets like London and France, was down by about 0.1% to 0.3%. The technology sector specifically dropped about 0.9%, with the German software company SAP falling 2.5% because Oracle’s disappointing sales and profit predictions, combined with increased spending plans, brought back worries about the high valuations and returns on investments in artificial intelligence.

Although the Federal Reserve indicated that it might not cut interest rates immediately until the job market stabilizes, which was a positive signal for investors, it wasn’t enough to counteract the tech sector’s decline.

In other company news, Delivery Hero shares dropped 5% after a downgrade from Citigroup, while Drax in London rose 2.2% after predicting higher-than-expected yearly profits, and RS Group was the top performer on the STOXX 600, gaining 3% after an analyst upgrade.

On the FX front, the US dollar received some support on Thursday because there was a general avoidance of risk across the markets.

However, it couldn’t fully recover the ground it lost the previous day against other major currencies like the euro, yen, and sterling, mainly because the Federal Reserve’s recent announcement was not as aggressive as some investors had anticipated.

The euro remained stable at 1.1704 (a two-month high) after a significant gain on Wednesday, and the British pound held steady at 1.13374 following a similar rise. The dollar also continued to weaken against the Japanese yen, dipping 0.14% to 155.8 yen.

Meanwhile, the Swiss franc reached its strongest level against the dollar in nearly a month, trading at 0.7992 per dollar.

The Australian dollar suffered from the same risk-aversion trend, falling 0.5% to 0.6644. Reflecting the broad drop in risk appetite,

Bitcoin briefly fell below the 90,000 mark, and Ether dropped more than 4% to 3,200..

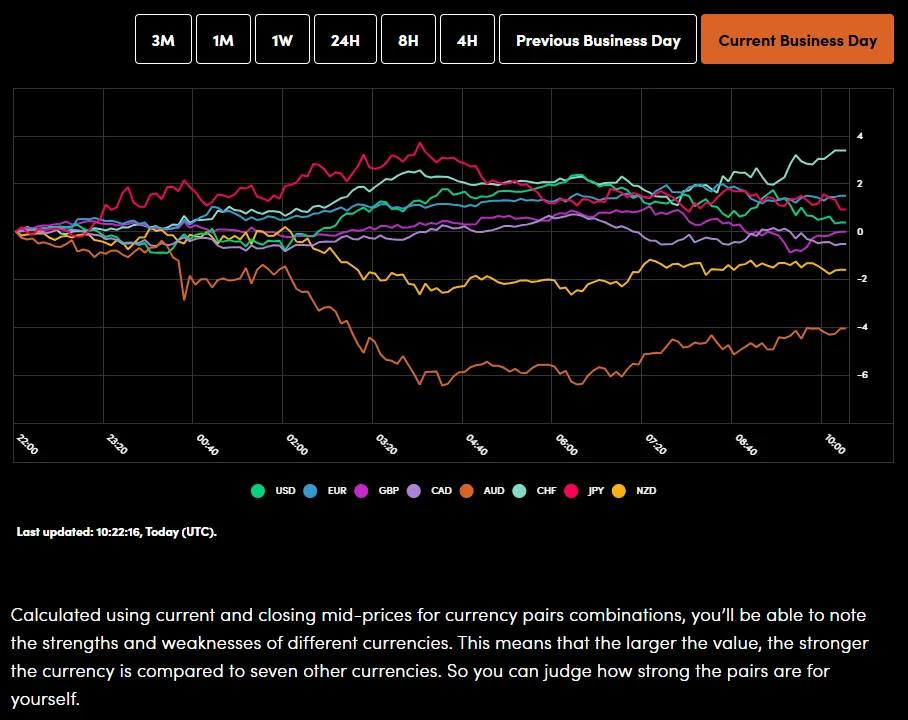

Currency Power Balance

Source: OANDA Labs

Oil prices declined on Thursday as investors redirected their attention toward two main events: the ongoing peace negotiations between Russia and Ukraine and the potential consequences of the US seizing an oil tanker that had been sanctioned off the Venezuelan coast.

These factors led to a decrease in prices. Specifically, Brent crude futures dropped by 81 cents, or 1.3%, settling at 61.40/barrel, and US West Texas Intermediate crude also fell by 78 cents, or 1.3%, to 57.68/barrel.

Gold prices dropped slightly on Thursday, moving away from a high point reached earlier in the week. This dip occurred because the US Federal Reserve’s recent interest rate cut was not unanimously supported, leaving investors uncertain about how quickly the central bank will continue to lower rates next year.

However, in contrast, silver hit a new record high. Specifically, spot gold fell 0.4% to 4,210.88/oz, though it had briefly reached its highest price since December 5th earlier in the trading session.

Meanwhile, US gold futures for February delivery saw a small increase of 0.3% to 4,238.10/oz.

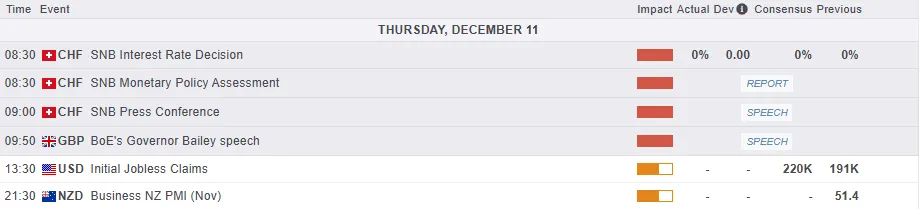

Economic Calendar and Final Thoughts

The European session will be quiet from a data perspective. There are Turkish interest rates and the OPEC monthly report which will be released and could stoke some volatility.

The US session will be busier though with Canadian and US trade balance data, Initial jobless claims and the NVIDIA senate bill coming into focus.

None of the above are expected to be massive market moving events and attention will now turn to inputs from the November jobs data next Tuesday.

The Federal Open Market Committee (FOMC) meeting yesterday was likely the most significant event that could positively impact the markets before the end of the year. Since that event has now passed, the US dollar might start to experience its typical seasonal weakness as the year concludes. This could cause the US Dollar Index (DXY) to gradually fall toward the 98.00 level.

For all market-moving economic releases and events, see the MarketPulse Economic

Chart of the Day – DAX Index

From a technical standpoint, the DAX Index has held above the key confluence level at 24000 for the last four trading days.

This could be seen as both positive and potentially slightly concerning. The failure to push higher means bulls are hesitant to push on and a lot of this is likely down to the FOMC meeting.

The post FOMC reaction has been rather tentative and not had a major impact on the DAX for now.

The period-14 RSI is eyeing a retest of the neutral 50 level. A bounce off this level could give bulls some optimism as it does hint that bullish momentum remains intact for now.

Immediate resistance rests at 24200 before the swing high just above the 24400 handle comes into focus.

Immediate support rests at 24000 before the swing high at 23880 and the 20-day MA at 23667 come into focus.

DAX Index Index Daily Chart, December 11, 2025

Source: TradingView.com (click to enlarge)